PW Consulting: CIPP Market Poised to Hit USD 44,992.3 Million by 2032

PW Consulting Strategic Brief: Cured‑In‑Place Pipe (CIPP) Market — 2026 Preview

As of our base year 2025, the global CIPP market is valued at USD 3,349.8 Million. PW Consulting’s forecasting framework projects sustained expansion through 2032 at a compound annual growth rate (CAGR) of 6.38% (forecast period 2026–2032), taking the market into a markedly larger scale by the end of the decade. This brief synthesizes the operational intelligence and decision‑grade outputs contained in our full report and explains why 2026 is a pivotal year for capital allocation, technology adoption, and partner selection in CIPP.

Cured-In-Place Pipe (CIPP) Market

Market Dynamics: What Is Driving Urgency in 2026

Structural demand drivers

The CIPP sector is being driven by a confluence of long‑term infrastructure needs and shorter‑term regulatory and technology impulses. Key structural drivers include:

- Aging sewer and water networks in mature markets that prioritize trenchless renewal to minimize surface disruption and extend asset life.

- Tighter regulatory regimes around water quality and environmental protection that increase the threshold for acceptable rehabilitation methods and verification testing.

- Material and process innovation — notably UV‑cured liners and styrene‑free resin systems — that reduce curing time and installation footprint in congested urban environments.

Cost and supply‑side pressures

Raw material composition (vinyl ester, isophthalic, UV cure chemistries and styrene‑free resins) and global resin market volatility are creating input cost uncertainty. At the same time, lead times for specialty nonwoven and glass‑reinforced liners are tightening as demand patterns shift. These supply‑side pressures are material to 2026 procurement strategies and to decisions on vertical integration or long‑term offtake contracts.

Regulatory and ESG alignment

Municipal procurement now embeds stricter compliance checks — from cure verification to wall‑thickness validation — and public‑sector ESG mandates increasingly favor no‑dig solutions that lower carbon and social disruption. For investors and operators, the regulatory environment converts specification compliance into a competitive bar rather than a checkbox.

Where Growth Materials Are Concentrated — a high‑level view

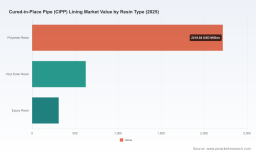

Our aggregate market sizing and time‑series analysis (2020–2025 historical, 2026–2032 forecast) reveals a market that is both growing and re‑balancing geographically and technologically. Rather than publish granular regional or application splits here, we quantify the overall opportunity and provide directionally what is changing:

- Geographic market centers are shifting in response to infrastructure investment cycles and retrofit priorities in mature economies, while adoption curves for UV technology accelerate where downtime costs are highest.

- Application mix is moving incrementally toward municipalities and utilities, with industrial and specialty segments adopting higher‑performance resin systems for corrosive environments.

- Market concentration remains relatively low: top three players account for a minority share of global revenue, reflecting fragmentation and local installer strength — an important factor for M&A and roll‑up strategies.

Strategic Imperatives for 2026

Executives deciding capital allocation this year face a narrow window where procurement, certification, and partner selection choices will materially affect EBIT margins and delivery risk. PW Consulting recommends three action levers that are central to 2026 execution plans:

- Lock supply through multi‑tier contract structures that cover specialty resins and liner fabrics while staggering price exposure.

- Accelerate validation programs for UV and styrene‑free systems to shorten time‑to‑revenue on high‑value urban contracts.

- Reassess M&A filters to prioritize installers with verifiable quality systems and local municipal relationships rather than purely volumetric metrics.

What Our Full Report Delivers — Practical Tools for 2026 Decisions

PW Consulting’s full CIPP market report is structured to move clients from insight to action. Key operative deliverables include:

- Supply‑chain map with upstream resin suppliers, liner fabricators, and logistics choke‑points — enabling targeted supplier risk mitigation and alternative sourcing scenarios.

- BOM (Bill of Materials) decomposition logic and cost‑build templates that let buyers stress‑test price scenarios and simulate margin impacts without divulging proprietary cost elements.

- Yield adjustment and installation‑loss models that translate field failure modes into unit‑cost and warranty reserve implications for 2026 contracts.

- Technology roadmap that overlays UV curing, glass‑reinforced liners, and styrene‑free chemistries with adoption timelines and operational implications for project scheduling and equipment capex.

These instruments are designed to solve 2026 pain points — from controlling resin cost exposure and securing installation quality to meeting tightened compliance checks — without presenting a single prescriptive parameter. Users can adapt the templates to their procurement cycles and regulatory environments.

Competitive Landscape: Dimensions of Advantage (Not Predictions)

Our industry mapping incorporates manufacturer profiles, installer networks and recent commercial moves. Rather than publish forward strategy for each firm, we analyze the competitive vectors that determine winners in CIPP engagements:

- Manufacturing scale and vertical integration — firms with integrated liner production and resin access reduce lead‑time risk and enjoy margin compression resilience.

- Technical differentiation — IP on UV curing processes, glass‑reinforced liner formulations, and validated styrene‑free systems create defensible performance gaps in urban and industrial projects.

- Installer network and local certification — design wins depend heavily on certified installation capacity, documented post‑installation verification, and municipal procurement relationships.

- Service and lifecycle support — warranty frameworks, long‑term monitoring packages, and rapid response crews convert single contracts into annuity revenue and lock‑in effects.

- M&A and consolidation strategies — recent acquisition activity underscores a move toward combining liner manufacturing scale with installer footprints to capture more upstream and downstream value.

PW Consulting has deep visibility into these dimensions across the competitive set — including legacy leaders with multi‑decade track records and smaller specialist innovators. The market’s low top‑three concentration means commercial outcomes are decided at the intersection of local execution and technical trust.

Notable industry developments (context for 2026)

Recent industry events and transactions are accelerating these dynamics:

- A high‑profile acquisition in 2026 expanded a liner producer’s global manufacturing footprint, highlighting consolidation momentum in UV liner supply.

- Major industry exhibitions in 2025 reinforced the diffusion of UV technologies and provided a forum for third‑party validation and specification harmonization.

For a consolidated list of recent developments and the implications for sourcing and partner selection, see our report briefing and interactive timeline.

Access the PW Consulting CIPP market report and interactive datasets for full regional and application breakdowns, supplier mappings, and scenario models referenced above.

Methodology and Data Rigor

PW Consulting’s CIPP research applies a layered triangulation methodology combining:

- Primary fieldwork: in‑market interviews with municipal procurement officers, leading installers, and manufacturing plant visits to observe curing workflows and production bottlenecks.

- Patent and citation analysis: mapping technology diffusion and proprietary claims around UV curing and reinforced liner chemistries to quantify technical defensibility.

- Proprietary cost modeling: BOM reverse engineering, supplier cost audits, and multi‑scenario sensitivity testing to derive margin impacts without exposing supplier‑level contracts.

- Third‑party verification: cross‑checking customs flows, ISO certifications, and independent lab cure‑test results to validate performance claims.

We emphasize how confidential, non‑public inputs (installation logs, audited supplier quotes, and instrumented cure data) are aggregated and anonymized into decision‑grade models. This process enables clients to trust modeled outputs while protecting commercially sensitive sources.

Action Plan for Executives — Practical Next Steps in 2026

Leaders preparing capital and procurement plans this year should prioritize three near‑term moves:

- Execute targeted supply agreements for specialty resins and reinforce alternate sourcing for liner fabrics to immunize margins against volatility.

- Run accelerated validation pilots for UV and low‑emission resin systems on at least two city projects to secure early mover advantages on municipal frameworks.

- Design integration playbooks that combine manufacturing scale, installer certification, and lifecycle service offers — these are the elements most likely to produce sustainable design wins.

PW Consulting’s full report provides the executable playbooks, contract templates, and scenario models necessary to implement these steps with measurable KPIs.

Closing

The CIPP market in 2026 is a technical, regulatory and procurement inflection point. The macro trajectory is positive — underpinned by long‑term infrastructure need and incremental technological improvement — but near‑term success depends on industrial sourcing discipline, validated performance claims, and municipal compliance readiness. PW Consulting’s full market study equips leaders with the tools to convert opportunity into predictable cash flows. For the complete dataset, regional distributions, and the templates that operationalize the insights summarized here, follow the link below.

Download the PW Consulting CIPP Market report — access the interactive models, regional maps and supplier scorecards referenced throughout this brief.

For detailed analysis of this topic, please visit the official page: Cured-In-Place Pipe (CIPP) Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.