PW Consulting: Tamping Machine Market Poised to Grow at a 5.3% CAGR, Driving Global Rail Infrastructure Upgrades

Tamping Machine Market — Strategic Briefing for 2026: Positioning Capital, Compliance and Competitive Advantage

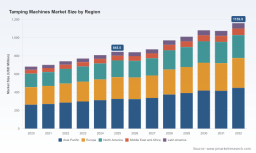

PW Consulting’s latest market intelligence on the worldwide tamping machine market synthesizes proprietary field-sourced evidence, engineering-level teardown analysis and multi-source triangulation to create an actionable playbook for executives allocating capital in 2026. The market continues its steady recovery and upgrade cycle: total industry revenue grows from 2,189.3 million USD in 2020 to 2,568.3 million USD in the base year 2025, with our model projecting a 5.3% compound annual growth rate across the 2026–2032 forecast window and an industry size near 3,670.0 million USD by 2032. This briefing highlights why these macro dynamics matter to boardrooms today, what levers materially reduce lifecycle cost and compliance risk, and where differentiation — not price — wins new platform orders.

Tamping Machine Market

Market Snapshot (2020–2032)

The historical series (2020–2025) shows consistent, investment-driven expansion in both new construction and maintenance demand, reflecting parallel waves of high-speed rail projects and freight network rehabilitation. Our 2026-onward forecast captures a market expanding at a 5.3% CAGR, driven by fleet renewals, rising specifications for energy efficiency and the steady adoption of automation and sensorization in track maintenance assets.

-

2020 revenue: 2,189.3 million USD.

-

2025 (base year) revenue: 2,568.3 million USD.

-

2026 forecast: 2,701.1 million USD; 2032 target: 3,670.0 million USD (forecast period 2026–2032).

Why 2026 Is a Turning Point for Capital Allocation

Several converging factors make 2026 a strategic inflection for tamping machine investment decisions:

-

Regulatory and procurement pressure for energy-efficient and low-emission equipment is increasing procurement total cost of ownership (TCO) thresholds and altering specification documents worldwide.

-

Rail operators are accelerating lifecycle replacement programs to reduce unplanned outages; aging fleets and rising maintenance backlogs are creating short windows to secure design wins for next-generation tampers.

-

Automation and sensor-based systems are moving from optional to expected: real-time geometry correction, predictive maintenance and telematics are now determinants of long-term contracting and service agreements.

-

Raw material volatility—especially high-strength steel—continues to pressure manufacturing margins and creates near-term procurement risk that must be hedged in 2026 budgets.

Recent industry actions underline this urgency: major OEM deliveries and fleet orders announced in late 2025 and early 2026 demonstrate active fleet upgrades and replacement cycles. These events are not isolated; they reflect a structural emphasis on universal tamping capabilities, energy efficiency variants and accelerated field deployment schedules.

Practical Tools in the Report — How They Address 2026 Pain Points

The report is designed as a decision-support toolkit for executives who must translate strategy into procurement and deployment outcomes in 2026. It contains operational artifacts and models that intersect directly with the pain points finance, operations and compliance teams face:

-

Supply‑chain topology and parts-mapping: visualized supplier tiers and critical-path components to de-risk single-source exposure without publishing vendor names that remain commercially sensitive.

-

BOM decomposition logic and manufacturing cost drivers: a methodology to decompose price into material, subassembly and labor buckets to inform negotiation and make-vs-buy decisions.

-

Yield adjustment and throughput models: scenario tools that show how incremental improvements in production yield and test yield translate to margin recovery across a fleet program.

-

Technology roadmaps and upgrade paths: a prioritized matrix for sensor, actuation and propulsion upgrades that balance capex, regulatory compliance and service revenue potential.

Each tool is packaged as an executable module — not as prescriptive parameter dumps. For example, our BOM logic tells you where margin is created and eroded and how to test alternative supplier and design choices against a client’s fiscal year 2026 budget envelope, but it does not disclose confidential unit-cost line items outside our client deliverables.

Competitive Landscape — Dimensions That Decide Design Wins

The tamping machine market shows moderate concentration (CR3 at 49.0% and CR5 at 55.0%), indicating a mix of global platform leaders and regional specialists. Rather than predicting specific 2026 initiatives for named vendors, PW Consulting evaluates competitive advantage through repeatable dimensions that shape who wins and who defends market share:

-

Technology moat: unique tamping mechanisms or control systems (e.g., high-frequency elliptical tamping or proprietary hydraulic architectures) that enable higher productivity or lower ballast wear.

-

Aftermarket and service network: the ability to deliver localized uptime guarantees, spare-part routing and training services that lock-in multi-year contracts.

-

Manufacturing scale and cost position: cost-competitive platforms are more likely to win volume orders where local content and price sensitivity dominate.

-

Integration capability: suppliers that bundle machine hardware with telematics, predictive maintenance and financing solutions win specification-led procurements.

-

Regulatory and sustainability alignment: vendors with validated low-emission variants or hybrid/electric offerings reduce procurement friction in regulated markets.

Applying these dimensions to the competitive set explains recent order patterns and delivery announcements without disclosing confidential program-level forecasts. Our analysis indicates that design wins in 2026 are increasingly decided by service economics and systems integration rather than point improvements in compaction performance alone.

For a full company-by-company capability matrix and our qualitative scoring of moat attributes, access the detailed competitive appendix here: https://pmarketresearch.com/worldwide-tamping-machines-market-research .

Methodology: Why Our Findings Are Actionable

PW Consulting’s conclusions rest on a layered triangulation methodology that blends public records, technical reverse-engineering and privileged sources. Core components include patent-citation mapping to identify technology ownership trajectories, engineering teardowns of representative platforms to validate BOM drivers, structured interviews with fleet maintainers and procurement officials, and anonymized transaction data from OEM order books and aftermarket contracts.

We emphasize how we obtain non-public inputs: targeted supplier surveys validated against customs and inland logistics manifests, site-level instrumented trials (with operator consent) to capture duty cycles, and cross-referencing of service records to infer failure-mode frequencies. This multi-vector approach reduces reliance on any single dataset and yields models that are resilient to noisy or incomplete public disclosures — precisely the capability executives need for 2026 decisions.

Strategic Actions for 2026 — High-Impact Recommendations

Translate insight into prioritized actions that preserve optionality and reduce downside in 2026:

-

Prioritize procurement specifications that shift evaluation from upfront capex to multiyear TCO, emphasizing energy consumption profiles, telematics readiness and availability SLAs.

-

Accelerate pilot deployments of sensorized units with predefined data contracts to validate predictive maintenance ROI before committing to fleet-wide retrofits.

-

Hedge critical material exposure in the next 12–18 months by securing strategic supplier agreements for high-strength steels and forged components that underpin tine and frame reliability.

-

Negotiate modular upgrade clauses in procurement contracts to allow staged adoption of hybrid/electric powertrains and advanced automation without asset stranding.

-

Assess partnership or local-assembly options in geographies with strict local-content rules to improve competitiveness in large tender processes.

For an executable checklist and procurement templates tailored to these recommendations, see the resources available in the full report: https://pmarketresearch.com/worldwide-tamping-machines-market-research .

Closing Perspective

In 2026, tamping machine markets are not just about moving ballast; they are a focal point where sustainability imperatives, digitalization and fleet economics intersect. Boards and executive teams that reframe procurement as a systems problem — combining machine specification, lifecycle service design and supply-chain resilience — will capture disproportionate value over the next funding cycle. PW Consulting’s tamping machine research delivers the analytical scaffolding to make those choices defensible, repeatable and auditable.

Contact PW Consulting to schedule a briefing of the full dataset, regional distribution maps and the executable modules described above.

For detailed analysis of this topic, please visit the official page: Tamping Machine Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.