PW Consulting Forecasts Game Engines Market to Expand at 6.8% CAGR Through 2032

Game Engines Market: Strategic Imperatives for 2026 — PW Consulting Market Brief

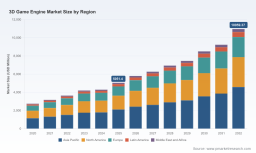

In 2026 the global game engines market is operating at an inflection point. After expanding from USD 999.8 Million in 2020 to USD 1,400.0 Million in 2025, the sector is projected to grow at a 6.8% CAGR across our 2026–2032 forecast horizon, reaching USD 2,225.0 Million by 2032. These headline numbers understate how quickly capital allocation windows are narrowing: improvements in rendering pipelines, cloud-native deployment patterns, and regulatory pressure on compute exports are collectively reshaping vendor economics and customer procurement cycles.

Game Engines Market

Why 2026 Is Pivotal

Strategic decisions made now determine platform share and partner economics for the next hardware and content cycle. Key structural shifts driving urgency include:

- Computational ceilings: High-fidelity 3D features increasingly demand high VRAM and dedicated ray-tracing cores, raising hardware baseline requirements for studio pipelines and cloud training environments.

- API standardization: Protocol-level improvements (notably recent Vulkan advances) lower cross-platform friction but raise the bar for engine maintainers to support multiple backends without ballooning TCO.

- Regulatory friction: Export controls on high-end GPUs and tightened procurement rules for dual-use technologies make cloud strategy and supplier diversification non-negotiable elements of risk management.

- Creative governance: Industry-level guidance on AI-generated assets is creating a compliance overhead for studios and engine providers that do not bake attribution and versioning into their toolchains.

Market Dynamics and Growth Drivers

Behind the headline CAGR, growth is being driven by several converging demand vectors. Our research identifies the following primary drivers shaping addressable opportunity and competitive dynamics in 2026:

- Enterprise adoption: Simulation, training, and virtual twin use cases continue to pull engine vendors into non-gaming revenue streams, creating new enterprise contract and licensing structures.

- Cloud & edge convergence: Real-time multiplayer and distributed rendering architectures are shifting value from single-platform runtimes to cloud orchestration and telemetry services.

- Web-native 3D: WebGPU and GPU-driven rendering advances expand reach into browser-based experiences, compressing time-to-market for lightweight 3D applications.

- Open-source momentum: Community engines lower entry barriers for indie developers, pressuring incumbents to differentiate via ecosystem services and commercial tooling.

- Hardware cycles: Adoption of hardware ray tracing and larger VRAM profiles changes the economics of fidelity versus cost, influencing platform support decisions.

What Our Report Delivers: Practical, Executable Tools

We designed the report to be a working playbook for 2026 procurement and engineering leaders. Key deliverables include:

- Supply chain maps that trace engine dependencies across middleware, cloud providers, and GPU vendors to reveal concentration risks and negotiation levers.

- BOM decomposition logic for typical engine deployments, enabling procurement teams to model marginal cost impacts of feature toggles and third-party plugins.

- Yield adjustment and TCO models focused on cloud GPU utilization, serving as a decision aid for hybrid on-premise vs cloud render strategies without prescribing a single “correct” configuration.

- Technical roadmaps that align engine capabilities (rendering, physics, networking) with hardware roadmaps and API standardization timelines, highlighting realistic upgrade windows for enterprise rollouts.

- Governance checklists that operationalize recent ethical and export-control updates for asset pipelines and cloud training workloads.

These assets are structured to resolve the immediate pain points we see in 2026—managing render-related cost inflation, maintaining compliance in cross-border deployments, and aligning engineering milestones with procurement cycles—without disclosing the confidential supplier-level numbers contained in the full dataset.

Competitive Dimensions That Decide 2026 Design Wins

Market concentration remains material: the top three firms together command approximately 68.4% of measurable share, indicating a competitive environment where ecosystem scale and partner reach are decisive. Our analysis highlights a consistent set of competitive dimensions that determine design wins and long-term defensibility:

- Ecosystem & tooling depth — a broad artist and engineering toolchain reduces friction for large studios and enterprise adopters.

- Rendering leadership — photorealism, Nanite-style geometry handling, and efficient global illumination create visible differentiation for AAA and simulation workloads.

- Cloud & service integration — seamless ties to cloud compute, multiplayer back-ends, and telemetry services accelerate time-to-value for multiplayer and enterprise customers.

- License & commercial model flexibility — predictable licensing that aligns with studio revenue models is often a gating factor in procurement.

- Community & extensibility — open-source projects and strong third-party marketplaces can erode incumbents’ pricing power unless countered by superior managed services.

Applied to the competitive set—major commercial engines, cloud-integrated offerings, and open-source projects—these dimensions explain why certain vendors win long-term platform roles while others succeed in niche or complementary positions. Recent engine releases and updates in 2025 demonstrate how vendors are doubling down on these dimensions: improved geometry handling for larger worlds, GPU-driven pipelines for web deployment, and Vulkan/backend optimizations that reduce cross-platform maintenance cost.

To explore our vendor-by-dimension matrix and see how each provider maps to these criteria, download the full report here: https://pmarketresearch.com/worldwide-3d-game-engine-market-research .

Regulation, Ethics, and Supply Risk — Strategic Considerations

Trade controls on high-end accelerators and updated industry ethical guidelines are no longer theoretical risks; they are active constraints that influence platform selection and capital allocation. In 2026, companies must simultaneously:

- Design multi-backend support to avoid single-vendor GPU lock-in.

- Incorporate provenance and attribution metadata into asset pipelines to meet evolving ethical expectations.

- Reassess cloud residency and data locality strategies to stay ahead of export-control and procurement compliance obligations.

These are not one-off checklist items: they materially affect TCO, time-to-market, and legal exposure. Firms that treat compliance as an engineering requirement, not a checkbox, gain measurable negotiating leverage with platform vendors and customers.

Methodology: Layered Triangulation and Source Rigor

PW Consulting’s conclusions rest on a multi-layered research protocol designed to produce reproducible, decision-ready intelligence. Key methodological pillars include:

- Patent and SDK citation analysis — mapping technology diffusion and identifying latent IP ownership that constrains feature swaps and licensing negotiations.

- Layered triangulation — combining confidential interviews with platform engineers, anonymized supplier procurement datasets, public financials, job-posting telemetry, and SDK usage metrics to reconcile headline claims with operational reality.

- Supplier BOM reconstruction — reverse-engineering common deployment stacks from contract templates and partner disclosures to model marginal cost and yield sensitivity.

We obtain non-public inputs through standard consulting channels: vetted executive interviews, NDAs with supply-chain partners, and collaboration with procurement practitioners. These sources allow us to quantify concentration and risk vectors without exposing proprietary transactional data in this public brief.

Actionable Strategic Guidance for 2026

For capital allocators, platform owners, and enterprise adopters the immediate implications are clear:

- Prioritize investments that reduce coupling to single GPU vendors and favor engines with multi-backend performance roadmaps.

- Allocate budget toward tooling that embeds compliance and provenance controls early in the asset lifecycle to avoid retrofitting costs.

- Negotiate design-win clauses that tie commercial terms to measurable ecosystem KPIs—SDK uptake, plug-in marketplace health, and cloud telemetry SLAs—rather than simple seat counts.

- Use BOM and yield models to stress-test vendor proposals under realistic hardware-constrained scenarios, treating GPU availability as a first-order cost driver.

These are high-conviction moves that change bargaining power in 2026 and reduce downside under both supply shocks and regulatory shifts.

Next Steps

PW Consulting’s full report includes the complete segmentation maps, vendor scoring matrices, scenario-modeled TCO templates, and step-by-step execution playbooks that senior teams need to convert insight into action. To access the detailed charts and confidential appendices, see: https://pmarketresearch.com/worldwide-3d-game-engine-market-research .

For detailed analysis of this topic, please visit the official page: Game Engines Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.