PW Consulting: Automotive Battery Thermal Management System Market Poised to Reach USD 9.8 Billion by 2032 with a 12.5% CAGR

Automotive Battery Thermal Management System Market — 2026 Strategic Brief

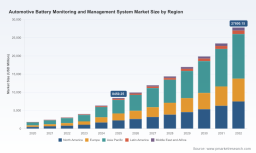

As of 2026, the Automotive Battery Thermal Management System (BTMS) market is operating at an inflection point. After expanding from USD 2.5 billion in 2020 to USD 4.3 billion in 2025, the market is now tracking a 12.5% compound annual growth rate (CAGR) into our forecast horizon and is projected to approach roughly USD 9.8 billion by 2032. That trajectory reflects both structural demand from vehicle electrification and an acceleration of regulatory, materials and software-driven forces that are reshaping supplier economics and OEM program decisions.

Automotive Battery Thermal Management System Market

Key market dynamics shaping 2026 decision-making

The drivers that matter this year are less about single-vehicle features and more about systems-level choices that determine capital efficiency and program risk. Clients we advise are prioritizing several converging trends:

-

Regulatory pressure and data traceability: New battery lifecycle rules and passport requirements are forcing OEMs to re-evaluate BTMS architectures to support lifecycle documentation and second-life use cases.

-

Safety and functional compliance: Faster adoption of higher ASIL requirements and international transport restrictions are increasing the technical bar for thermal and monitoring subsystems.

-

Cost and materials shifts: Battery pack price deflation and chemistry shifts (notably LFP penetration) are changing the relative value of thermal performance versus per-kWh pack cost — creating trade-offs between up-front spend and lifecycle risk.

-

Software and intelligence: AI-enabled diagnostics, prognosis and thermal controls are migrating performance value from pure hardware to hardware-software co-design, favoring suppliers with combined semiconductor, software and systems capabilities.

-

Supply-chain concentration and supplier differentiation: Design wins increasingly depend on supply-chain transparency, proven manufacturing yields and integration into OEM validation cycles rather than only component performance on paper.

Why 2026 is a decisive year for capital allocation

With market size already at USD 5.0 billion in 2026 and a sustained double-digit CAGR, capital committed this year will disproportionately influence total addressable share through 2032. The urgency arises from three linked pressures:

-

First-mover cost advantage: Early bets on scalable thermal platforms and validated BOM roadmaps allow volume suppliers to compress per-unit cost before competitors replicate architectures.

-

Regulatory timing: Compliance requirements and transport limitations that take effect in 2026–2027 create hard deadlines for qualifying modules in global vehicle programs.

-

Design-win windows: OEM program timelines—shortened through platformization and zonal electrical architectures—mean suppliers that can demonstrate integrated BMS/BTMS proof-points secure longer-term production volume.

What PW Consulting's BTMS report delivers (practical, execution-focused tools)

Our new market study is deliberately operational. It packages strategic insight into a set of executable instruments for 2026 program and portfolio decisions:

-

End-to-end supply-chain map: A verified tiered supplier network that identifies single-source risks, capacity choke-points and alternative sourcing routes.

-

BOM teardown and cost-to-produce logic: A guided decomposition approach that maps component cost drivers and assembly labor sensitives to help finance and sourcing model supplier-side negotiations.

-

Yield-adjustment and scenario cost models: Parametric models that convert yield improvements, chemistry choices and localization steps into per-vehicle cost outcomes under multiple OEM ramp scenarios.

-

Technology roadmap and migration pathways: Comparative matrices that position liquid cooling, air-cooling, phase-change options and hybrid concepts against program-specific constraints (pack density, duty cycle, thermal runaway mitigation).

-

Compliance and qualification playbook: Checklists and gate criteria aligned to international safety standards, battery passport needs and upcoming transport restrictions to shorten qualification cycles.

-

Partner-selection scoring and negotiation templates: Decision frameworks that weight technical fit, manufacturing footprint, IP position and software/cloud capabilities to prioritize strategic suppliers for design-win pursuit.

Each tool is crafted for translation into board-level decisions — not as theoretical analysis but as templates and processes teams can deploy to compress time-to-qualification and reduce program-level financial uncertainty.

Competitive landscape — dimensions that determine design wins

Our competitive analysis focuses on the capabilities and moats that actually produce production programs. Across the supplier universe, we see five decisive dimensions:

-

System-level integration: Suppliers that combine sensors, power electronics, and control firmware reduce OEM validation burden and shorten integration cycles.

-

Functional-safety and standards credentials: Proven ASIL-rated platforms, pre-validated firmware and documented qualification processes materially improve selection odds.

-

IP and semiconductor leverage: Access to advanced power semiconductors, precision monitoring ICs and sensor IP is a differentiator as thermal control shifts to software-driven, fine-grained management.

-

Manufacturing and supply resilience: Near-term capacity, multi-sourcing strategies and logistics control are becoming competitive filters — not just cost factors.

-

Software and cloud services: Predictive diagnostics, lifecycle telemetry and integration with battery passports are now bid components in many OEM RFQs.

We map these dimensions against representative players to highlight where each firm has structural strengths without attempting to publish proprietary program forecasts. Examples of directional signals that reinforce these dimensions include strategic partnerships and platform launches: a recent exclusive low-voltage battery systems partnership announced by a European systems supplier highlights trend towards integrated low-voltage solutions; extensions of semiconductor-to-software collaborations illustrate the push to AI-enabled BMS capabilities; and launch of pre-validated R-BMS platforms confirms the market premium on reducing OEM validation time. These developments are discussed in-depth in the report alongside comparative supplier archetypes.

Access the full competitive maps and company profiles to validate supplier fit for your 2026 programs.

Methodology — how PW Consulting generates proprietary, actionable insight

Our findings are founded on layered triangulation and reproducible methods designed to surface non-public program indicators while meeting client confidentiality constraints. Core elements include:

-

Patent and citation analysis to track where engineering effort is concentrated and to identify emerging protective IP positions.

-

Physical BOM teardowns and validation runs performed across representative pack architectures to quantify component mixes and assembly flows.

-

Supplier audit data and an expert panel of OEM validation engineers to corroborate manufacturing capability claims and yield assumptions.

-

Proprietary procurement and freight datasets, anonymized contract sampling, and customs flows to detect sourcing shifts and capacity constraints.

-

Machine-learning–augmented models that reconcile price signals, production yields and ramp schedules into probabilistic scenario outputs.

Combining these layers enables us to surface leading indicators — for example, supplier tool orders or firmware release cadences — that are seldom visible in public filings yet materially influence design-win probabilities. The report documents our calibration steps so that clients can reproduce sensitivity analyses under their specific program assumptions.

Actionable recommendations for 2026 (executive checklist)

For executives allocating capital this year, our advisory experience and scenario testing point to a compact set of high-leverage actions:

-

CFOs and strategy teams: Prioritize funding for platforms that demonstrably lower time-to-qualification and contain validated yield-improvement roadmaps rather than modular feature add-ons that defer manufacturing risk.

-

Product leaders: Adopt co-design contracts that bind thermal hardware and BMS software providers to shared performance and diagnostic SLAs, reducing integration rework.

-

Sourcing and procurement: Execute dual-sourcing strategies for critical thermal components and secure early supplier process audits to protect ramp timelines.

-

Compliance and legal teams: Integrate passport and transportation constraints into early-stage design gates to avoid retrofit costs and shipment delays.

-

R&D and operations: Invest selectively in AI-enabled thermal control capabilities that can shift value from costly hardware improvements to closed-loop control and predictive maintenance.

Next steps — how to use this analysis

PW Consulting’s BTMS report is designed as an operational guide for teams that must convert strategy into executable program plans in 2026. If your objective is to optimize program economics, accelerate qualification cycles, or evaluate supplier trade-offs under regulatory constraint, the full dataset and playbooks enable rapid scenario testing tailored to your fleet, chemistry and geographic footprint assumptions.

For immediate access to the full suite of competitive profiles, supply-chain maps, BOM templates and scenario models, visit our detailed report page: https://pmarketresearch.com/auto/automotive-battery-monitoring-and-management-system-market .

For detailed analysis of this topic, please visit the official page: Automotive Battery Thermal Management System Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.