PW Consulting: Rebar Coupler Market Poised to Surge — Forecasted 7.4% CAGR Through 2032

Rebar Coupler Market 2026: Strategic Intelligence for Capital Allocation and Operational Resilience

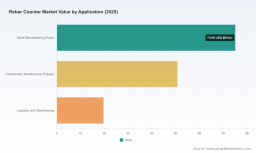

PW Consulting’s latest Rebar Coupler Market study (base year 2025) provides a forward-looking operational playbook for executives allocating capital in 2026. The market is on a sustained expansion path—growing from a 2025 baseline of USD 1,820.0 Million to an anticipated near-USD 3,000.0 Million by 2032 under a 7.4% CAGR—creating discrete windows for differentiated returns and operational defensibility. This release summarizes the report’s strategic value while reserving the full, actionable segmentation and scenario outputs for subscribers.

Rebar Coupler Market

Why 2026 Is a Pivotal Year for Rebar Coupler Decision‑making

2026 is characterized by three intersecting pressures that raise the bar on vendor selection, cost models, and compliance frameworks:

-

Raw material and input volatility — regional rebar price spikes and tight domestic supplies in several key markets are compressing margins and accelerating supplier consolidation.

-

Regulatory and ESG scrutiny — procurement specifications increasingly require traceability and standardized testing across the supply chain, elevating the cost of non-compliance.

-

Rapid automation adoption — OEMs and mill operators accelerate machine‑vision and AI integration to increase throughput and reduce downstream rework.

These forces mean that capital committed in 2026 needs to be backed by granular, scenario‑driven insights rather than broad market optimism.

Market Trajectory and Tactical Implications

Our forecast horizon (2026–2032) uses layered scenario modeling to translate a 7.4% compound annual growth rate into practical milestones for procurement, R&D pacing, and M&A timing. The market’s projected expansion to approximately USD 3,000.0 Million by 2032 signals both sustained demand and widening product differentiation opportunities—especially for players that convert technical superiority into repeatable design wins.

Notably, macro commodity signals are already influencing supply-side economics:

-

US ex‑works rebar prices reached approximately USD 1,058.2 per tonne in early 2026, showing abrupt monthly tightening that pressures replacement and inventory strategies.

-

A global steel benchmark stood at 3,103.0 CNY per tonne in April 2026, underscoring continuing base‑metal cost cyclicality that must be modeled into long‑term contracts.

These inputs translate into concrete operational imperatives: protect gross margins through BOM‑level redesigns, migrate cost volatility into hedgable or pass‑through contract structures, and accelerate yield-improvement programs within rolling-mill ecosystems.

Report Deliverables: Practical Tools, Not Just Projections

The PW Consulting report is intentionally operational and built for immediate deployment by procurement, operations, and corporate strategy teams. Key deliverables include:

-

End‑to‑end supply‑chain map showing supplier tiers, single‑point risks, and logistics choke points to prioritize contingency spend and supplier diversification.

-

BOM disaggregation logic that links coupler design choices to unit manufacturing cost and spare‑parts exposure—enabling procurement teams to run what‑if sourcing scenarios without bespoke engineering inputs.

-

Yield‑adjustment and tolerance models that quantify the downstream cost of counting errors, misjoins, and grout defects—useful for justifying automation investments and 5‑to‑7 figure CAPEX decisions.

-

Technical‑roadmap overlay that aligns emerging coupling technologies, machine‑vision inspection capabilities, and on‑line counting systems with likely OEM product cycles and standards evolution.

Each tool is accompanied by implementation checklists and decision matrices that translate analytic outputs into board‑level action items—without exposing the proprietary segmentation tables reserved for the full report.

Competitive Landscape: Dimensions of Advantage

The competitive topology in 2026 is defined less by simple scale and more by the composition of durable advantages. Our analysis covers established suppliers and challengers across multiple competitive dimensions:

-

Technology moat — companies that couple proprietary machine‑vision algorithms with hardware integration and on‑line diagnostics create switching costs that extend beyond price.

-

Operational speed to deployment — firms demonstrating rapid project commissioning and standardised testing regimes convert pilots into regionally scaled rollouts.

-

Service and software economics — players offering entitlement upgrades, remote diagnostics, and predictive maintenance capture aftermarket revenue and strengthen Design Wins.

-

Channel and project partnerships — access to large rolling‑mill projects and infrastructure contractors is often decisive for national rollouts, particularly where compliance and traceability are enforced.

Representative competitors we evaluated include firms known for advanced vision systems and rolling‑mill integrations. Our firm-level study assesses each player across the competitive dimensions above—demonstrating which combinations of IP, field performance, and commercial model are most likely to convert into sustainable share gains. For a deep dive into our comparative matrices and vendor scorecards, consult the full report.

Key example (not exhaustive): several vendors are already delivering AI‑enabled counting systems deployed in 2025–2026 projects, evidencing the link between algorithmic accuracy and 24/7 operational uptime—one of the most actionable predictors of future Design Wins.

To review PW Consulting’s vendor scorecards and procurement‑ready RFP templates, visit the full report: https://pmarketresearch.com/worldwide-rebar-counter-market-research .

Supply‑Chain and Cost Risk: What Boards Must Monitor Now

Several practical risk vectors require immediate board attention in 2026:

-

Concentration risk in raw‑material sourcing and logistics that can crystallize into price shocks.

-

Compliance and testing regimes that impose capitalized retrofit costs if not planned in procurement cycles.

-

Integration risk between coupler hardware, on‑line counters, and plant SCADA systems: technical incompatibilities add hidden TCO.

The report provides prioritized mitigation actions, including contractual templates for hedging exposure, supplier audit playbooks, and a roadmap for incremental automation investments that preserve optionality while improving unit economics.

Methodology: How PW Consulting Sources Confidential, High‑Integrity Intelligence

Our conclusions are grounded in a multi‑layered research approach designed to surface actionable, verifiable intelligence beyond public statements. Core elements include:

-

Layered triangulation — we cross‑validate supplier claims through patent citation analysis, procurement tender reviews, and anonymized customer interviews to isolate performance claims from marketing language.

-

Primary fieldwork — factory inspections and live commissioning observations where permitted, combined with sensor log extraction and quality‑assurance test reports, provide empirical performance baselines.

-

Proprietary economic modeling — BOM‑level costing algorithms and yield‑adjustment models convert technical differentials into P&L impacts under multiple commodity scenarios.

We explicitly supplement public sources with confidential inputs obtained under NDA from procurement offices, consenting OEMs, and tier‑1 infrastructure contractors—then apply rigorous statistical reconciliation to produce defensible forecasts. This approach enables us to surface the commercial implications of performance differentials without disclosing raw, contract‑sensitive data in the public summary.

Action Framework for 2026: Where Executives Should Focus

For leadership teams evaluating capital allocation in 2026, our analysis crystallizes three priority moves:

-

Prioritize technical proof‑points that map directly to yield and uptime. Shortlist vendors that can demonstrate repeatable, short‑cycle commissioning at scale.

-

Embed material‑price scenarios into multi‑year supplier contracts and BOM designs to preserve margin under commodity stress.

-

Invest in aftermarket and software capabilities that convert a one‑time sale into recurring revenue and defensible customer relationships.

Each recommendation is coupled in the report with tactical steps, estimated implementation timelines, and decision gates to convert strategic intent into executable programs within 6–18 months.

Next Steps and How to Access the Full Intelligence

PW Consulting’s Rebar Coupler Market report is structured to support both strategic deliberation and immediate operational implementation. The public summary you are reading is intentionally selective: it demonstrates our methodological depth and identifies high‑impact decision levers while directing you to the full dataset and playbooks that subscription clients receive.

For access to full segmentation maps, vendor scorecards, procurement templates, and the complete set of operational tools referenced here, visit the full report: https://pmarketresearch.com/worldwide-rebar-counter-market-research .

For detailed analysis of this topic, please visit the official page: Rebar Coupler Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.