PW Consulting Forecasts Dental Handpiece Market to Hit USD 1,228.0 Million by 2032

Dental Handpiece Market 2026: Strategic Imperatives for Capital Allocation

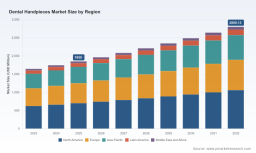

PW Consulting publishes a focused industry briefing derived from our forthcoming Dental Handpiece Market report (base year 2025). The market is sizing at USD 990.0 Million in 2025 and is modeled to grow at a 3.1% CAGR across the 2026–2032 forecast window to reach approximately USD 1,228.0 Million by 2032. Market concentration is meaningful: the top three suppliers account for roughly 47.0% of revenue and the top five for about 55.0%, creating both entry barriers and targeted M&A opportunities. This briefing explains why 2026 is a critical year for capital deployment and how our practical toolset converts research into executable decisions—without exposing the granular segmentation charts reserved for report subscribers.

Dental Handpiece Market

Market Dynamics Shaping 2026 Decisions

Several interlocking dynamics determine winners and losers in 2026. Buyers and investors must align product strategy, production footprint and aftermarket services to three structural shifts that accelerate capital reallocation:

- Regulatory and reprocessing pressure: CDC and FDA guidance calls for validated heat sterilization and performance-based pathways, which elevates compliance cost for non-validated designs and shortens commercial windows for legacy products.

- Clinical workflow and material trends: Rising use of high-strength restorative materials is increasing demand for higher-power electric handpieces and specialized coatings, changing BOM composition and service profiles.

- Commercial model evolution: Dental service organizations (DSOs) and large group practices increasingly favor subscription and managed-service arrangements, converting CapEx into recurring revenue but increasing supplier obligations around uptime and field service SLAs.

Why 2026 Is a Decision Point

2026 is not a passive year for portfolio managers. The convergence of updated regulatory expectations, several recent product launches and portfolio expansions, and evolving aftercare economics compresses time-to-action for manufacturers, distributors and investors.

- Compliance cliff: New sterilization and device performance guidance forces product requalification or phase-out; the cost of delayed compliance is material for mid-tier providers.

- Technology bifurcation: The market is polarizing toward premium, high-power electric systems with advanced coatings and smarter entry-level units optimized for subscription deployment.

- Service economics: With variable margins in aftermarket parts and repair, companies that secure design wins tied to long-term service contracts achieve disproportionate returns.

Practical Tools Inside Our Report—and How They Solve 2026 Pain Points

PW Consulting’s report is built as an operational playbook. Our deliverables are designed to move teams from insight to execution on cost control, compliance, and go-to-market alignment. Highlights include:

- Supply-chain topology map: Visualizes supplier tiers for critical components (turbine bearings, micro-motors, coatings, LEDs) and identifies second-source candidates to mitigate single-supplier concentration.

- BOM decomposition logic: A repeatable methodology to translate design choices into cost buckets (materials, precision machining, sterilization-validated assembly, aftermarket spares), enabling rapid scenario modeling for price and margin impact.

- Yield-adjustment and cost-to-serve models: Allow manufacturers to stress-test gross margins under different sterilization validation programs, warranty terms and subscription service levels—useful for CFOs reconciling CapEx vs. recurring revenue trade-offs.

- Technology roadmap with decision gates: Compares electric, air-driven and hybrid pathways against regulatory readiness, manufacturability and serviceability—helping R&D leaders prioritize investments that earn early design wins.

- Field-service and reprocessing playbooks: Cover best-practice service network design, spare-parts pooling and sterilization-validation protocols built to lower downtime and support subscription SLAs.

Each toolkit is accompanied by templates and a set of scenario outputs; these are purpose-built for 2026 operational constraints such as compressed validation cycles and tighter service-level expectations.

Competitive Dimensions: What We See Across Leading Providers

Our competitive analysis focuses on the dimensions that determine long-term commercial success rather than enumerating step-by-step 2026 plans for individual firms. Key competitive moats and design-win determinants include:

- Engineering and IP defensibility: Precision engineering, sensor feedback systems and proprietary bearing/drive designs drive product differentiation and aftersales margins.

- Materials and surface technologies: Proprietary coatings and high-power motor packaging are decisive where zirconia and other hard materials dominate restorative workflows.

- Regulatory and validation leadership: Firms with established sterilization validation processes and FDA-ready documentation shorten customer procurement cycles—particularly with institutional buyers and DSOs.

- Integration and systems play: Suppliers that bundle handpieces with integrated motors, control electronics and connectivity gain traction in practices seeking turnkey maintenance and predictive service.

- Distribution and aftermarket scale: Deep direct sales networks and authorized-service footprints reduce downtime and are frequently the tiebreaker in enterprise procurement.

Applying these dimensions to leading names in the market, PW Consulting observes the following patterns (high-level):

- Legacy precision OEMs maintain strong engineering moats and deep OEM relationships; their design wins are often secured on performance predictability and clinical reputation.

- Premium European suppliers trade on material science and finishing processes that enable demanding restorative tasks.

- Large integrated dental companies leverage system integration and infection-control credentials to win multi-product contracts with DSOs and hospital networks.

- Regional manufacturers and aftermarket specialists compete on cost, warranty offerings and service speed—areas that become attractive acquisition targets for firms seeking to broaden distribution or enter subscription economics.

For a full competitive matrix, product-by-product capability scoring and our proprietary design-win heatmap, access the full dataset here: https://pmarketresearch.com/hc/dental-handpieces-market .

Methodology: Why Our Forecasts and Operational Tools Are Actionable

Our analysis uses a layered-triangulation approach combining patent-citation mapping, controlled tear-downs, supplier interviews conducted under NDA, DSO procurement-panel surveys, warranty and field-service telemetry, and public regulatory filings. This multi-source approach allows us to reconcile declared claims with in-market performance and true cost structures.

We adhere to rigorous cross-validation protocols: patent activity is cross-referenced against BOM-level teardowns, supplier revenue run-rates are reconciled with shipment proxies and service-visit logs, and design-win trends are validated through anonymized procurement panels. When we reference "non-public" evidence in the report, it reflects data obtained through contractual partnerships, manufacturer disclosures under confidentiality, and field instrumentation aggregated into anonymized, statistical formats to preserve commercial sensitivity.

2026 Strategic Recommendations for Capital Allocation

Based on our operational toolset and market dynamics, PW Consulting recommends that investment committees and executive teams take the following priorities into 2026:

- Prioritize compliance-ready portfolios: De-risk product lines that require sterilization revalidation or FDA pathway workstreams. The timetable for validation should be integrated into capital planning and SKU rationalization exercises.

- Shift from unit-sales to service economics selectively: Evaluate pilot subscription offerings in regions or customer segments where uptime and predictable spend are highly valued; model trade-offs with our cost-to-serve templates before scaling.

- Build aftermarket scale or partner strategically: Given concentration among top suppliers, acquiring or partnering with regional service networks accelerates market access and supports design wins that rely on fast field support.

- Invest in targeted technology bets: Focus R&D on motor-packaging, sensor feedback and validated surface treatments that materially shorten clinical cycle times for hard-material restorations.

- Use M&A to close capability gaps—fast: With the top-five concentration in place, tuck-in acquisitions that add coating chemistry, sterilization validation capabilities or field-service channels can be value-accretive within 18–24 months.

Final Note: Immediate Actions

2026 is a year in which regulatory timing, product cycles and commercial model shifts converge into a compressed window for capital allocation. PW Consulting’s report translates these forces into executable programs—supply chain plays, portfolio pruning templates and M&A scorecards—so that leaders can convert insight to defensible advantage. For the full regional distributions, segmentation charts and the operational annexes that support board-level decisions, please review the comprehensive report: https://pmarketresearch.com/hc/dental-handpieces-market .

For detailed analysis of this topic, please visit the official page: Dental Handpiece Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.