PW Consulting: Advanced Packaging Market Set to Grow at 8.6% CAGR During 2026–2032

Advanced Packaging Market 2026: Strategic Imperatives for Capital Allocation and Risk Management

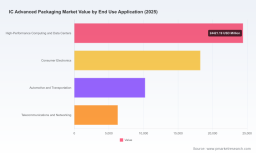

PW Consulting’s latest Advanced Packaging Market study (base year 2025) equips executives and investors with the actionable, scenario-based intelligence needed to make high-consequence decisions in 2026. The worldwide advanced packaging market has evolved rapidly from an estimated USD 22.2 Billion in 2020 to USD 45.1 Billion in 2025, and we project continued expansion to USD 49.6 Billion in 2026, supporting a compounded forecast trajectory (2026–2032) at a 8.6% CAGR that reaches an anticipated USD 80.4 Billion by 2032. This press briefing highlights the report’s strategic value for 2026 planning while preserving the detailed segment-level findings for subscribers who access the full study.

Advanced Packaging Market

Market Snapshot: A 2026 View

In 2026 the advanced packaging market is simultaneously maturing and replatforming. A structural demand surge since 2023—driven by AI/HPC, high-bandwidth memory integration and system-level performance requirements—has accelerated capacity additions and shifted capital intensity higher. Market concentration remains moderate: the top three firms account for 18.0% of market share, and the top five capture 38.0%, indicating continued competitive pressure from regional OSATs and emerging niche specialists.

Key Growth Drivers and Strategic Risks

Boardroom discussions in 2026 must weigh a clear set of drivers and asymmetric risks that determine where and how much to invest over the next 12–36 months.

- Demand drivers:

- AI and HPC workloads requiring heterogeneous integration and increased memory bandwidth.

- Proliferation of 2.5D/3D and fan-out architectures to meet form-factor and thermal constraints.

- Cross-industry adoption—automotive electrification, industrial edge compute, and healthcare devices—raising customization and reliability demands.

- OSAT and IDM capacity expansions aimed at proximity to hyperscale and OEM design centers.

- Systemic risks:

- Raw material bottlenecks and price volatility—recently demonstrated by supply concentration in certain critical minerals and multi-fold price moves for items used in advanced substrates and interconnects.

- Export control regimes and tariff scenarios that reconfigure where capital is deployed and how supply chains are re‑oriented.

- Yield and manufacturability risk as firms push hybrid bonding, finer-pitch interconnects and 3D stacking into volume production.

- Regulatory and ESG compliance pressures that create upstream traceability requirements for strategic buyers.

What the Report Contains — Practical, Execution-Focused Tools

PW Consulting’s report is engineered for implementation rather than abstract forecasting. Key deliverables include:

- Supply-chain topology maps that detail tiered supplier relationships, chokepoints and alternative sourcing pathways for critical materials and substrates.

- BOM decomposition and cost-build logic that translate package architectures into material, process and test spend drivers—designed for integration into procurement and sourcing models.

- Yield-adjustment and ramp models that provide scenario testing for different process maturity timelines and their P&L impact.

- Technology roadmaps that synchronize packaging nodes (e.g., fan-out, 2.5D/3D, hybrid bonding) with expected design windows by end-market cohort.

- Compliance and ESG modules that map traceability requirements and likely supplier remediation timelines under prevailing export-control and materials-policy regimes.

Each tool is delivered with a clear “how-to-use” playbook showing where it plugs into capital planning, vendor selection, and design-win strategies—enabling procurement, engineering and strategy teams to convert insights into executable programs in 2026.

Competitive Dimensions — What Determines Winners in 2026

Our competitive analysis focuses on capability vectors rather than prescriptive forecasts for individual firms. In 2026, success in advanced packaging depends on a small set of achievable but difficult-to-replicate competitive dimensions:

- Technology moats — proprietary process stacks, validated hybrid-bonding flows, and IP around interposer and TSV integration accelerate customer qualification cycles.

- Manufacturing scale and proximity — capacity located near hyperscalers and major IDM customers reduces logistics risk and shortens design‑to‑production lead times.

- Design‑win execution — integration between packaging engineers, system architects and OEM design teams that can co-optimize thermal, power and mechanical constraints.

- Supply continuity and materials security — companies that pre-empt raw‑material constraints with multi‑sourcing, strategic inventories, or captive refining positions gain negotiating leverage in 2026.

- Testing and yield engineering — advanced device testing capabilities and fast feedback loops that shorten yield ramp and mitigate early life failure modes.

Leading IDMs and OSATs are reinforcing different vectors: some are doubling down on proprietary packaging IP and ecosystem control, while others compete on cost, geographic footprint, and customer intimacy. Notable 2025–2026 developments—capacity expansions announced by several major players—underscore the urgency to secure design wins and material contracts now. To review the full competitive mappings and our firm‑by‑firm capability matrices, access the complete report: Access the PW Consulting Advanced Packaging Market Report .

Methodology — Why Our 2026 Intelligence Is Distinctive

PW Consulting’s findings stem from a layered triangulation methodology designed to reconcile public filings with primary, proprietary inputs. Core research methods include patent and citation mapping, confidential OEM and supplier interviews under NDA, on-site process audits, and controlled BOM teardowns validated against supplier quotes and customs data. We then stress-test scenarios using discrete-event yield and ramp models calibrated to observed line yields and contract test outcomes. This multi-source validation gives us confidence in our scenario envelopes while preserving discretion over the granular datapoints that clients require under subscription.

How These Tools Address 2026 Pain Points

Executives face three immediate operational priorities in 2026: cost control, compliance, and ramp risk. The report’s modules are aligned to each:

- Cost control: The BOM decomposition and supplier-cost-sensitivity tools identify the 10–20% of components and processes that drive most of the margin variance, enabling targeted negotiations and design substitutions without sacrificing performance.

- Compliance and sourcing: The supply-chain topology and ESG module identify regulatory exposure and upstream single‑points‑of‑failure, enabling procurement to design compliant sourcing lanes and traceability programs.

- Ramp and yield risk: Yield-adjustment models allow scenario testing of alternate ramp profiles, informing capital allocation to additional process engineering resources or second-source capacity in critical geographies.

Strategic Recommendations for 2026 Decision-Makers

Based on our 2026 market view, PW Consulting recommends a prioritized, risk-weighted approach to capital and commercial decisions:

- Prioritize investments that secure design wins with hyperscalers and strategic OEMs—early co-development of packaging can create multi‑year revenue streams and lock in system-level optimization.

- Hedge material and substrate exposures now—contract language, staged buy options, or co-investment in upstream supply can materially reduce surprise cost volatility.

- Balance scale with flexibility—build or secure capacity that supports both high-volume fan-out and specialized 2.5D/3D offerings to capture a broader set of design opportunities.

- Invest in yield engineering and test automation—reducing time‑to‑volume is frequently a higher-return use of capital than marginal capacity expansion in 2026.

- Embed compliance and ESG due diligence into supplier selection—noncompliant suppliers create not just reputational risk but tangible program delays under existing export-control and tariff dynamics.

Closing — Why Now Matters

Market momentum and policy-driven supply-chain shifts make 2026 a pivotal year for advanced packaging decision-makers. PW Consulting’s Advanced Packaging Market report provides the practical modeling, supplier intelligence and scenario playbooks required to convert market opportunity into durable commercial advantage. For teams that must align engineering, procurement and capital allocation in 2026, the full study contains the detailed segment maps, supplier matrices, and scenario models needed to act with conviction. Access the complete study here: Access the PW Consulting Advanced Packaging Market Report .

For detailed analysis of this topic, please visit the official page: Advanced Packaging Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.