PW Consulting: Mica Paper Market Poised for Rapid Expansion with a 9.1% CAGR, New Insight Reveals

Mica Paper Market Outlook 2026 — Strategic Imperatives for Capital Allocation

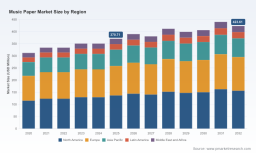

As PW Consulting releases its latest Mica Paper Market Mica Paper Market Mica Paper Market Mica Paper Market Mica Paper Market Mica Paper Market Mica Paper Market Mica Paper Market update for 2026, senior leaders must reconcile a simple fact: the industry is materially larger and more dynamic than conventional vendor briefings suggest. Our base-year benchmarking (2025) places the global mica paper market at USD 670.0 Million, with a projected trajectory to approximately USD 1,180.0 Million by 2032 at a 9.1% CAGR for 2026–2032. This growth profile creates both an investment window and a source of strategic risk for manufacturers, OEMs, and institutional buyers in the coming 18–36 months.

Mica Paper Market

Market Snapshot: Momentum, Not Mystery

The market has experienced steady expansion from 2020 to 2025, reflecting multi-vector demand drivers: electrification of equipment, higher-temperature insulation requirements, and an industrial pivot toward advanced synthetic substrates. These macro signals are not evenly distributed — the market’s center of gravity is shifting — and the winners will be those who translate that directional change into near-term design wins and supply security rather than relying on legacy channel strength.

- Historical scale: the market expanded from a modest base in 2020 to USD 670.0 Million in 2025, reflecting product requalification cycles across multiple industrial end markets.

- Forward momentum: a 9.1% CAGR for 2026–2032 implies accelerating capex and procurement activity through the end of the decade.

- Industry structure: the market exhibits moderate concentration (CR3: 35.2%; CR5: 48.0%), indicating meaningful room for mid-tier players to leverage specialization and for incumbents to consolidate value via downstream integration.

Why 2026 Is a Strategic Inflection Point

For boards and investment committees, 2026 is not “another year.” Three converging forces make it a make-or-break planning horizon:

- Trade and compliance tightening: new regional trade rules and more rigorous material traceability requirements increase the cost of non-compliance and lengthen supplier qualification timelines.

- ESG-driven procurement: end users and financiers are embedding material-level sustainability expectations into contracts, forcing suppliers to demonstrate supply-chain transparency and emissions control at the mica and processed-paper stages.

- Digital manufacturing uplift: AI-enabled process control and yield-management tools are moving from pilot to production, changing the calculus on who can consistently meet tight dielectric and dimensional tolerances at scale.

These trends elevate the value of actionable, operational intelligence over high-level market anecdotes — which is precisely where our Mica Paper Market report delivers immediate ROI for decision-makers.

What the Mica Paper Market Report Provides — Practical Tools, Not Plate Scraps

Our research package is designed as a strategic playbook for 2026 capital allocation and procurement cycles. We deliberately focus on operational instruments that translate into measurable margin and risk reduction while withholding segmented line-item tables in this summary to preserve the “trailer” nature of this release.

- Supply-chain map and tiered BOM decomposition — a visualized supplier topology down to sub-tier mineral feedstocks and critical processing nodes, enabling targeted supplier diversification and concentration risk scoring.

- Bill-of-Materials (BOM) logic and yield-adjustment models — pragmatic templates that show how small shifts in raw-material purity, calendering yield, or lamination throughput cascade to EBITDA under different demand scenarios.

- Technology roadmap and requalification playbook — side-by-side paths for muscovite, phlogopite, and synthetic mica paper adoption that outline requalification timelines, expected test protocols, and likely cost inflection points for 2026 buyers.

- Regulatory & compliance matrix — an actionable checklist to align supplier audits, test-cert chains, and traceability controls with near-term trade and ESG requirements.

Collectively, these modules are purpose-built to answer two executive questions: “How do I reduce cost volatility without jeopardizing reliability?” and “How do I certify compliance for complex, multi-source mica supply chains in time for 2026 product launches?” The report shows the methods and levers; it does not substitute for company-specific parameterization, which we help clients perform via bespoke engagements.

Competitive Landscape — Dimensions of Advantage, Not Scorecards

The market’s competitive topology is best understood through strategic dimensions rather than static rankings. Across the value chain — from raw mica miners to laminated-paper converters and distributor channels — firms compete on a mix of the following defensible attributes:

- Raw-material access and vertical integration: secure upstream feedstock can compress cost and expedite qualification, particularly in markets sensitive to supply disruption.

- Process IP and quality gates: thickness control, dielectric uniformity, and thermal-stability process recipes act as effective technical moats once embedded in OEM qualification lists.

- Customer intimacy and design wins: pre-certification at the component engineering stage accelerates adoption; design-win velocity is often more valuable than short-term price concessions.

- Distribution reach and niche channel strength: some legacy distributors and specialty paper manufacturers retain strong institutional relationships that can be repurposed for mica-based substrates.

For example, a set of small-to-mid-sized suppliers — well-known in adjacent specialty paper markets and select distribution channels — leverages deep customer service, customization capacity, and localized inventory models to capture design wins in educational and instrument-level applications. These players differ materially from converter-integrators who compete primarily on scale, capital intensity, and validated high-voltage performance.

PW Consulting’s field work has observed that design wins in 2026 increasingly favor players who can simultaneously demonstrate technical reproducibility, traceable supply, and low requalification friction. This triad is the dominant axis for near-term market share shifts.

On Adjacent Channels and Retail/Distribution Influence

Certain retailers and specialty-paper distributors retain disproportionate influence in institutional buying cycles and educational channels. While these actors are not typically primary suppliers for high-voltage industrial mica paper, their distribution intelligence and SKU-level customer data are valuable signals for forecasting demand and seasonal inventory needs. PW Consulting integrates such third-party channel intelligence into our demand overlays to refine procurement lead-time assumptions.

To review our full competitive matrices and the company-level strategic dimension maps, access the full report: access the full Mica Paper Market report .

Technology Pathways and Supply Resilience — Tactical Priorities for 2026

Technical and procurement leaders must prioritize three tactical domains this year to convert market growth into resilient margin:

- Qualification velocity: shortening supplier qualification cycles by pre-validating suppliers against modular test suites reduces time-to-market for product launches.

- Yield uplift via AI: adopting proven AI process-control modules for lamination and calendaring can deliver asymmetric upside on yield and scrap reduction within a single six-to-nine-month initiative.

- Sustainable sourcing proofs: establishing verifiable emissions and chain-of-custody proofs for mica feedstocks is no longer optional for capital-backed OEMs and system integrators.

Implementing these priorities requires disciplined experiments and pilot budgets in 1H–2H 2026. The cost of delayed action is not merely lost revenue but increased exposure to supplier rationalization and rising compliance costs.

Methodology — How PW Consulting Sees What Others Miss

Our Mica Paper Market analysis is built on layered triangulation and traceable, replicable evidence collection. Methodological pillars include:

- Patent and standards-citation analysis — mapping process- and material-related patents to active production footprints to detect near-term capacity and capability shifts.

- Layered triangulation — integrating customs trade flows, confidential supplier interviews, third-party lab test logs, and on-site OEM qualification schedules to reconcile demand and supply at a granular level.

- BOM and yield reverse engineering — reconstructing representative Bills of Materials from disassembled samples and production-acceptance criteria to populate our yield-adjustment models.

We obtain non-public inputs through structured NDAs, targeted supplier workshops, and cooperation with independent test labs. These sources enable us to produce forward-looking operational tools rather than static forecasts — a key differentiator when clients must make supply decisions with 12–24 month consequences.

Implications and Recommended Next Steps for Executives

For CFOs, procurement heads, and CTOs, the tactical implication of our 2026 assessment is straightforward: prioritize supplier qualification velocity and invest in targeted yield-improvement pilots now. Specific starting actions include:

- Initiate a 90–120 day supplier assurance sprint to map tier-1 and tier-2 risks, focusing on traceability and requalification windows.

- Allocate a pilot budget for AI-enabled yield-control modules at a single converter site to validate scrap-reduction assumptions before scaling.

- Mature procurement clauses to include verifiable sustainability and traceability deliverables tied to milestone-based payments.

These moves protect near-term deliveries while positioning organizations to capture the upside of a market that PW Consulting expects to be materially larger and more consolidated by 2032.

Access the Full Intelligence

This executive brief is a strategic preview that demonstrates the depth of PW Consulting’s operational insight while preserving the granular segmentation, supplier-level matrices, and scenario parameterizations for the full report. To review the complete dataset, interactive supply-chain maps, and the requalification playbook, visit: access the full Mica Paper Market report .

For detailed analysis of this topic, please visit the official page: Mica Paper Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.