PW Consulting: Solid Organ Transplant Immunosuppressant Market Set to Grow at 4.7% CAGR During 2026–2032

Solid Organ Transplant Immunosuppressant Market 2026: Strategic Priorities for Capital Allocation and Operational Resilience

PW Consulting’s new market study — base year 2025, historical review 2020–2025 and forecast 2026–2032 — reframes how executive teams should prioritize investment and operational choices in the organ transplant immunosuppressant space. The global market is measured at USD 5,350.0 Million in 2025 and is projected to reach USD 7,373.0 Million by 2032, expanding at a compound annual growth rate of 4.7%. This release is written from a 2026 vantage point and is designed to be a strategic “trailer”: it surfaces decisive, evidence-backed insights while directing decision-makers to the full report for the detailed segment maps, regional splits and actionable model parameters.

Solid Organ Transplant Immunosuppressant Market

Why 2026 Is a Pivotal Year for Resource Allocation

Three concurrent dynamics make 2026 a pivotal moment for capital allocation and portfolio reshaping:

-

Moderate, steady top-line growth driven by medical practice continuity and incremental adoption of formulation innovations — growth that rewards disciplined manufacturing and pricing strategies rather than volume-only plays.

-

Sustained pressure from generic entrants and patent expiries that shift margin dynamics; protecting or regaining design wins at major transplant centers is now a function of integrated clinical value and supply reliability.

-

Heightened regulatory and reimbursement scrutiny (notably Medicare/CMS policies on coverage and duration) that increases the value of evidence-based pharmacoeconomic positioning when negotiating formularies and pathways.

Core Market Dynamics (Summary)

Key dynamics that shape market outcomes in 2026 and beyond are:

-

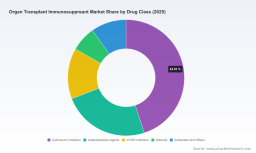

Established therapeutic classes (notably calcineurin inhibitors) continue to form the backbone of maintenance regimens, maintaining clinical preference and standard-of-care momentum.

-

Supply-side constraints — including the persistent limiting factor of donor organ availability — keep volume growth bounded even as per-patient therapy complexity rises.

-

Generic competition and multi-sourced manufacturing compress commodity pricing tails; differentiation increasingly depends on delivery format, adherence-enhancing formulations and patient support services.

-

Regulatory clarity and reimbursement policy (for example, CMS coverage parameters) have immediate impact on hospital procurement and payer negotiations; firms that proactively model these constraints capture outsized near-term design wins.

What PW Consulting’s Report Gives You — The Operational Toolbox

The value for boards and operating teams comes from the report’s actionable toolset, built to translate 2026 market realities into executable initiatives:

-

Supply-chain topology and vulnerability map — granular routes-to-market, single-supplier nodes and alternate sourcing options that matter when a vial shortage risks patient continuity.

-

Bill-of-materials (BOM) decomposition logic — an approach to disaggregate product economics across API sourcing, formulation, packaging and cold-chain requirements to isolate margin levers without exposing proprietary cost inputs.

-

Yield-adjustment models and sensitivity templates — calibrated to real-world manufacturing yields, these allow finance and manufacturing leads to stress-test EBITDA under alternate quality and yield scenarios.

-

Technology roadmaps and upgrade paths — sequencing for digitization and AI-driven process control that prioritize interventions delivering the fastest returns on compliance and yield improvements.

-

Regulatory and reimbursement playbook — a compliance-focused checklist that aligns dossier strategy, post-market evidence and local reimbursement engagement for faster formulary access.

These instruments are purpose-built to address the most pressing 2026 pain points — cost control under margin compression, supply continuity in the face of periodic shortages, and accelerated market access under tightened reimbursement rules — while preserving the exercise of commercial discretion that proprietary datasets require.

Competitive Landscape: Dimensions That Will Decide 2026 Outcomes

The competitive map is concentrated: the top three firms account for a dominant share and the top five an even larger portion of the commercial market. That concentration shapes the tactical frame for challengers and incumbents alike.

Across the major players active in the market, PW Consulting’s analysis highlights a common set of competitive dimensions that determine near-term success:

-

Moat type — product efficacy/clinical legacy vs. manufacturing scale vs. integrated patient support. Incumbents with long-standing clinical data wield a modality-based clinical moat, while large manufacturers offset price erosion with scale-driven cost moats.

-

Design-win determinants — reliability of supply, hospital-level clinical familiarity, and the presence of adherence or monitoring programs. Procurement teams increasingly treat immunosuppressants as bundled services rather than line-item drugs.

-

Regulatory and payer sophistication — firms that couple robust pharmacoeconomic dossiers with proactive CMS and payer engagement reduce time-to-formulary and protect realized price.

-

Generic strategy — some established players defend with authorized generics or differentiated formulations; others pursue licensing/partnerships to protect share in cost-sensitive markets.

Representative players in this environment include innovators with long-established transplant portfolios and multiple generics manufacturers that exert pricing pressure. Recent 2025–2026 product activity (for example, a new tacrolimus injection vial introduced late in 2025) demonstrates that formulation-format competition is now a critical vector for procurement wins, especially in inpatient settings with rapid turnover.

For a deeper firm-by-firm competitive diagnostic and our proprietary “Design-Win Scoring” matrix that operational teams use to prioritize accounts, see the full company profiles and matrices in the complete report: Download the full report .

Regulatory and Reimbursement Context

Regulatory and payer signals are decisive in 2026. Public policies that maintain coverage for immunosuppressive therapies (including specific Medicare provisions) stabilize baseline demand profiles but also set the perimeter for acceptable pricing and duration of coverage. Manufacturers and investors must therefore model reimbursement shocks into near-term forecasts rather than treating them as tail risks.

Methodology — How PW Consulting Builds Confidence in Hidden Numbers

Our approach uses Layered Triangulation: we fuse patent and clinical-trial registers, anonymized claims and hospital procurement data, customs/tender flows, and structured interviews with transplant surgeons, hospital pharmacists and manufacturers. This multi-source triangulation reduces single-source bias and allows us to infer non-public commercial flows and manufacturing constraints with measured confidence intervals.

Specifics that increase the depth of our inference include: targeted supply-chain audits, reverse-BOM techniques on public filings, and reconciliation of prescription trends with aggregate manufacturer shipment data. All primary-source inputs are validated through multiple counterparty confirmations and internal plausibility checks before they inform the actionable models and scenario outputs included in the report.

Strategic Recommendations for 2026 (Executive Checklist)

Our findings translate into a short list of priority actions for 2026 decision-makers:

-

Prioritize manufacturing flexibility: invest selectively in process upgrades and secondary suppliers to lower single-point-of-failure risk and improve bargaining position with hospital systems.

-

Differentiate around format and adherence: extended-release formulations and alternative delivery formats are now legitimate sources of premium realization in clinical procurement dialogs.

-

Defend margins intelligently: employ authorized generics or licensing strategies where appropriate; reserve commercial discounts for regions where generics-induced price erosion is structural.

-

Align evidence and payer strategy: build economic models that translate clinical outcomes into payer value propositions, particularly for CMS-governed markets.

-

Use M&A and partnerships tactically: prioritize targets that add either manufacturing redundancy, formulation IP or hospital network access rather than only volume.

-

Implement AI-driven yield interventions: short-cycle projects in process control can deliver rapid ROI on yield and compliance, directly addressing 2026 margin pressure.

Next Steps and How to Access the Full Intelligence

PW Consulting’s full report provides the complete regional and application distribution charts, the firm-level scenario maps, and downloadable model templates that CFOs and heads of manufacturing use to stress-test budgets for 2026–2032. For the detailed breakdowns and the complete set of operative tools, access the full intelligence pack here: Download the full report .

PW Consulting’s Solid Organ Transplant Immunosuppressant Market study is designed to move executives from reactive defensiveness to proactive, data-backed portfolio and operational decisions in 2026. The full report contains the segment-level charts and operational models you will need to act with conviction.

For detailed analysis of this topic, please visit the official page: Solid Organ Transplant Immunosuppressant Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.