PW Consulting Forecasts Brass Faucets Market to Expand at a 4.8% CAGR Through 2032, Signaling Steady Momentum for Manufacturers

Brass Faucets Market 2026: Strategic Preview for Capital Allocation and Operational Resilience

Executive Summary

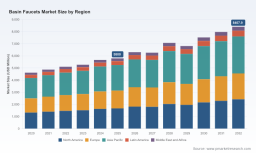

PW Consulting’s Brass Faucets Market report—anchored on a 2025 base year and projecting through 2032—presents an actionable vantage point for executives planning capital allocation, supplier strategy, and product roadmaps in 2026. The global market is currently operating from a 2025 baseline of USD 128.9 Million and is forecast to expand at a compound annual growth rate (CAGR) of 4.8% across the 2026–2032 horizon, reaching an estimated USD 179.0 Million by 2032. These macro trajectories reflect recovering end‑use demand, pockets of premiumization, and a re‑shuffling of cost and compliance pressures that materially affect near‑term investment returns.

Brass Faucets Market

Why 2026 Is a Pivotal Year

2026 is not “business as usual.” Several coincident forces raise the urgency for board‑level decisions this year:

Brass Faucets Market

- Raw material volatility: brass scrap prices and upstream alloy inputs are materially influencing unit margins for brass‑constructed fixtures.

- Regulatory tightening: lead‑free mandates and high‑efficiency lavatory specifications are shifting design and testing costs into product development cycles.

- Product migration: major brands are accelerating touchless, minimalist, and custom‑finish launches—forcing incumbents and suppliers to prioritize either scale efficiencies or specialized differentiation.

Market Trajectory: What the Numbers Conceal — and Reveal

The headline CAGR of 4.8% masks heterogenous drivers that vary by channel, product architecture, and compliance exposure. PW Consulting’s analysis shows a market that is simultaneously growing and polarizing: growth is concentrated in select premium and smart-enabled subsegments while legacy high-volume commodity nodes face margin compression from raw material cost swings and stringent water/lead regulations.

Market concentration remains relatively low: the combined share of the three largest firms is below 30.0% (CR3 ≈ 22.5%; CR5 ≈ 27.8%), which sustains competitive pressure on pricing and design innovation. For strategic planners, this means scale advantages are important but not sufficient—winning requires alignment of product specification, channel access, and regulatory readiness.

Strategic Priorities for 2026

Executives should consider four interlocking priorities when setting budgets and targets for 2026.

- Regulatory‑first product architecture: embed WaterSense and lead‑content constraints into the earliest design stages to avoid costly rework and to secure municipal and large‑scale commercial specs.

- Raw‑material hedging and supplier diversification: build flexible sourcing playbooks for brass and substitute alloys to mitigate price shocks and downstream yield variability.

- Smart and touchless ROI frameworks: quantify the incremental margin and specification stickiness of touchless features versus their additional BOM and compliance costs.

- Selective premiumization: prioritize finish and customization capabilities that translate into defensible design wins with architects and high‑end specifiers.

Competitive Landscape — Dimensions of Advantage

PW Consulting’s competitive review synthesizes corporate profiles, recent product activity, and observed supplier networks to map the competitive dimensions across established and niche players. Rather than forecasting detailed 2026 moves for each vendor, we highlight the structural levers that determine who wins in basin‑faucet procurement and specification.

- Brand and distribution moat: incumbents with deep trade relationships and specification teams still capture a disproportionate share of large commercial projects.

- Design and finish capability: bespoke finish options and artisan‑level customization function as a commercial hedge against commoditization for premium players.

- Manufacturing durability and specification compliance: firms engineered for heavy‑use commercial environments compete on durability testing and institutional approvals.

- Technology and integration: touchless and smart features are now table stakes in certain channels; integration quality and software/UX reliability are becoming decisive Design Win factors.

Recent product activity in early 2026 reinforces these dimensions. Several vendors introduced collections at KBIS and Spring launches that exemplify current market bets—touchless operation and curved, sculptural minimalism for mainstream premium lines, and handcrafted, made‑to‑order collections for the bespoke high end. These moves demonstrate how brands are layering product innovation on top of existing distribution and specification strengths.

Operational Playbook: Tools Included in the Report

The report is intentionally practical. PW Consulting provides applied tools that procurement, product, and operations teams can use to convert strategy into measurable actions—without disclosing client‑level or proprietary parameter sets in this preview.

- Supply‑chain topology maps that show supplier tiers, typical lead times, and risk nodes for brass and secondary components.

- BOM deconstruction templates that guide targeted cost‑out initiatives and substitution scenarios without prescribing a one‑size‑fits‑all solution.

- Yield‑adjustment and rework models to stress‑test margins under different scrap‑price and regulatory compliance scenarios.

- Technology roadmaps that align product features, certification timelines, and development cost buckets to prioritize investment sequencing.

Each tool is geared toward resolving specific 2026 pain points: controlling material‑driven cost escalation, accelerating compliance certification, and setting procurement contracts that reflect realistic yield and finish variability.

Technology & Design Trends Shaping R&D Budgets

Design and technical direction in 2026 centers on three converging trends:

- Contactless interaction: the market is seeing a step change in demand for touchless operation that requires cross‑disciplinary investment in sensors, power management, and sealing technologies.

- Materials engineering under compliance constraints: alloy optimization to meet lead‑content limits while preserving machinability and finish adherence.

- Customization at scale: modular manufacturing approaches that allow a configurable finish and performance matrix without linearly increasing inventory complexity.

R&D planners should staff cross‑functional squads combining design, compliance, and supply‑chain expertise to compress time‑to‑market while avoiding late‑stage certification failures.

Regulatory & Raw‑Material Dynamics — Immediate Implications

Regulatory constraints such as lead‑content ceilings and high‑efficiency lavatory flow requirements are not future threats; they are current design constraints that increase time and cost to market for new SKUs. Raw‑material dynamics, including mid‑2026 brass scrap pricing, are elevating unit cost risk and shortening planning horizons for price‑sensitive channels.

Decision makers must therefore adopt a two‑track response: design and certify compliant SKUs for regulated markets while implementing flexible procurement and cost pass‑through mechanisms for commodity lines.

Methodology Corner

PW Consulting’s findings combine quantitative and qualitative evidence through a Layered Triangulation framework. Key methodological pillars include:

- Patent‑citation and standards‑compliance scanning to identify emerging technical boundaries and likely future certification costs.

- Primary interviews with OEM procurement, Tier‑1 die casters, and finishing specialists, conducted under NDA to surface non‑public input cost drivers and yield behavior.

- Physical teardown and BOM reconstruction of representative basin faucets, validated against customs flows and commercial shipment data to reconcile theory with trade reality.

These approaches yield a validated decision‑support dataset that informs the tools and scenarios in the full report while protecting sensitive source material obtained through confidential agreements and secure fieldwork.

How Executives Should Use This Report in 2026

The value of this research is practical, not just predictive. Use it to:

- Stress‑test your 2026 CAPEX and NPD plans under alternate raw‑material and regulatory scenarios.

- Prioritize supplier investments and dual‑sourcing strategies to defend margin against brass volatility.

- Quantify the ROI of compliance‑first design versus retrofit strategies for major product families.

- Create procurement contracts with embedded yield and finish allowances informed by teardown‑validated BOM templates.

Next Steps & Access

For executives preparing capital plans or reassessing product portfolios in 2026, the full PW Consulting Brass Faucets Market report contains the complete suite of models, regional distributions, and scenario matrices necessary to act. Access the full Brass Faucets Market report here: https://pmarketresearch.com/hc/basin-faucets-market .

Final Observations

2026 requires a balanced posture: protect against cost and compliance risk while selectively funding product differentiation that secures specification lock‑ins. PW Consulting’s market sizing, scenario toolset, and competitive analysis are designed to help leaders convert uncertainty into defensible, time‑sensitive decisions—without compromising on operational detail or strategic ambition.

For detailed analysis of this topic, please visit the official page: Brass Faucets Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.