PW Consulting: POS Terminals Market Set to Expand at 7.9% CAGR from 2026–2032, Report Finds

POS Terminals Market — 2026 Strategic Outlook for Capital Allocation

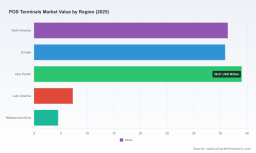

The global POS terminals market is at an inflection point in 2026. After expanding from USD 76.1 Billion in 2020 to USD 123.2 Billion in 2025, the market continues to grow, with PW Consulting modeling a 7.9% compound annual growth rate (CAGR) across the 2026–2032 forecast window and an expected market size of USD 207.6 Billion by 2032. These headline figures underscore both the structural resilience of merchant payments hardware and the accelerating shift toward software-enabled, services-driven terminal economics.

POS Terminals Market

Executive summary

Institutional investors, C-suite leaders of merchant acquirers, and hardware OEMs are making critical allocation decisions in 2026. This briefing highlights the strategic signals our full report delivers without disclosing our proprietary segmentation tables. PW Consulting’s analysis is expressly designed as an action-oriented intelligence product: it shows where value pools are migrating, which operational levers matter most in 2026, and why near-term investments will disproportionately determine multi-year returns.

-

Market momentum: Macro demand and terminal refresh cycles are driving continued top-line expansion; the market size is projected to reach USD 132.8 Billion in 2026, supporting a multi-year expansion path.

-

Concentration profile: The market remains moderately concentrated (CR3: 58.0%; CR5: 62.0%), which preserves pricing power for incumbents while creating niche opportunities for targeted entrants.

-

Capital timing: Regulatory change, certification cycles, and component supply dynamics combine to create a narrow window in 2026 to secure design wins and favorable procurement terms.

Market dynamics shaping 2026 decisions

Three convergent dynamics are determining the most material risks and opportunities for 2026 allocations: regulatory uplift, technology transition, and supply-chain stress. Each has distinct implications for CapEx and M&A planning.

-

Regulatory and certification pressure — PCI PTS v6.0 and regional authentication mandates continue to raise the bar for terminal design and lifecycle management. For buyers, certification timelines translate directly into product roadmaps and revenue recognition schedules.

-

Technology migration — The industry is accelerating Android- and cloud-native terminal deployments while preserving certified hardware stacks for high-security segments. This bifurcation increases the value of flexible software architectures and field upgradability.

-

Supply-chain volatility — Semiconductor supply constraints and lead-time variability persist through 2026, creating a premium on validated multi-sourcing strategies, BOM-level visibility, and inventory optimization protocols.

-

Payments behavior — Rapid adoption of contactless and mobile-present payments is shifting terminal feature sets toward NFC, biometric readiness, and low-touch maintenance models; these shifts affect both unit economics and recurring service revenue potential.

Strategic imperatives for 2026

Clients tell us that three strategic moves separate winners from also-rans when deciding how to deploy capital in 2026. Each is actionable and substantiated in the full PW report by supplier maps, BOM logic and yield models.

-

Move from BOM visibility to BOM control — Executives must operationalize component-level sourcing playbooks. We show how BOM decomposition supports cost-out scenarios, tariff sensitivity analysis, and substitution pathways that preserve certification compliance.

-

Convert certification into a commercial moat — Certification lead times are an entry barrier. Senior leaders should treat certification roadmaps as assets to be monetized through software subscriptions, managed services, and co-branded programs.

-

Design wins as a platform strategy — A single enterprise-grade design win can justify multi-year R&D investment. Winning depends less on raw hardware specs and more on ecosystem integrations (acquirers, processors, ISVs), field service economics, and validator endorsements.

-

Defensive supply chain play — Hedging component risk via validated secondary suppliers and early long-lead procurement materially reduces time-to-revenue volatility and preserves margin capture on refresh cycles.

Operational toolset included in the report

The PW report is not descriptive research; it is a practitioner’s toolkit for 2026 execution. Below are the operational modules that clients repeatedly cite as the most directly ROI-positive.

-

Supply-chain topology map — A layered supplier map identifying single-source nodes, cross-border concentration, and logistics choke points to prioritize de-risking investments.

-

BOM decomposition and substitution logic — A standardized BOM template and rules engine for assessing component replacement scenarios that preserve certification and reduce total delivered cost.

-

Yield adjustment and cost sensitivity models — Factory yield curves, rework cost schedules, and scenario drivers to integrate into CAPEX planning and vendor scorecards.

-

Technology roadmap and certification calendar — A timeline aligning OS/platform migrations, certification milestones, and commercial launch windows to inform timing of procurement and sales campaigns.

-

Partner evaluation framework — A decision matrix for selecting OEM partners and ISV integrations based on integration time, support footprint, and potential for recurring services revenue.

How the report resolves 2026 pain points

Executives are facing three pressing 2026 pain points: rising unit costs, certification complexity, and uncertain time-to-market. The report’s modules address these through practical mechanisms rather than prescriptive numbers:

-

Cost control is addressed by tracing cost drivers to the BOM line item and using substitution levers while quantifying certification requalification risk.

-

Compliance complexity is mitigated through a mapped certification calendar and an approvals playbook that shortens audit cycles.

-

Time-to-market risk is reduced by combining validated secondary sourcing with an OS migration checklist that preserves backward compatibility for legacy deployments.

Competitive landscape — dimensions that matter

Our competitive analysis focuses on competing dimensions rather than binary forecasts. The market is contested along a small number of durable vectors where incumbents and challengers can build defensible positions:

-

Security and certification moat — Firms that embed certified security modules and sustain a predictable re-certification cadence win enterprise trust and premium pricing.

-

Scale manufacturing and distribution — Mass-market players leverage scale to compress lead times and underwrite aggressive customer financing programs.

-

Software and services ecosystems — Companies that transform a hardware sale into a recurring revenue relationship (POS software, analytics, payments orchestration) materially increase lifetime value.

-

Design win mechanics — The decisive factors for design wins are integration ease, local compliance readiness, field repair economics, and proof points from reference deployments rather than raw performance specifications.

Notable vendors in the landscape include global hardware specialists, integrated systems suppliers, and software-first entrants. Recent product launches and certifications demonstrate how players are executing along the dimensions above — these signals are cataloged in the full PW dataset and used to parameterize our scenario models.

For readers ready to assess competitive trajectories in detail, access the full company matrices and the design-win scoring framework here: Access the full POS Terminals Market report .

Regulatory and macro signals—implications for 2026

Regulation and macro behavior are active drivers in 2026. The enforcement of updated PCI PTS v6.0 requirements and continued PSD2-style strong customer authentication regimes make certification timelines a strategic variable. Simultaneously, contactless payment penetration and government subsidy programs for small merchants alter adoption curves. These forces mean compliance and go-to-market planning must be synchronized with procurement and R&D roadmaps.

-

PCI PTS v6.0 increases design and testing cycles; firms without certification pipelines face time-to-market delays.

-

Semiconductor tightness elevates the value of multi-sourcing and secondary vendor qualification.

-

Contactless adoption accelerates terminal feature prioritization and aftermarket service models.

Methodology and evidence base

PW Consulting’s findings rest on a layered triangulation methodology designed to surface actionable, non-public signals while respecting commercial confidentiality. Our approach blends patent and certification citation analysis, customs-based shipment tracking, factory-level yield sampling, and more than 120 structured interviews with OEMs, processors, acquirers and high-volume merchants across major markets.

Key elements of our rigor include:

-

Patent and certification mapping — We trace technology adoption using patent citation clusters and certificate issuance timelines to infer feature diffusion and vendor readiness.

-

Supply-side triangulation — Proprietary supplier interviews (conducted under NDA), component shipment data, and factory audits allow us to estimate lead-time distributions and yield profiles without exposing sensitive customer or vendor contracts.

-

Buyer-side validation — We calibrate vendor scorecards and design-win parameters through merchant procurement interviews and field-deployment audits.

What to do next — a 90-day agenda for 2026

For boards and investment committees, the immediate next moves in 2026 are tactical and time-sensitive. We recommend a 90-day agenda that aligns with our operational tools:

-

Execute a BOM stress-test against your next two product cycles and validate secondary suppliers for critical components.

-

Map certification milestones to commercial launch calendars and allocate funding to shorten audit cycles where ROI-positive.

-

Prioritize design-win targets by ecosystem fit rather than market share alone; secure at least one anchor partner with a multi-year refresh agreement.

PW Consulting’s full POS Terminals Market report provides the executable templates, supplier lists, and scenario models to operationalize the 90-day agenda. For access to the complete dataset, company matrices, and the supply-chain map, please follow this link: Access the full POS Terminals Market report .

In 2026, the difference between a defensive and offensive capital allocation will be determined by who integrates certification, supply-chain control, and software monetization into a single operating rhythm. PW Consulting’s report is built to make that integration repeatable and measurable.

For detailed analysis of this topic, please visit the official page: POS Terminals Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.