PW Consulting Predicts Virus Filtration Market to Grow from USD 205.0 Million in 2025 to USD 338.3 Million by 2032 at a 7.5% CAGR

Virus Filtration Market: Strategic Imperatives for 2026 — PW Consulting Preview

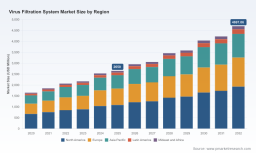

As 2026 unfolds, virus filtration sits at an inflection point where regulatory stringency, biologics pipeline expansion, and manufacturing modernization converge to reshape capital allocation and operational priorities. PW Consulting’s new market study — anchored on a 2025 base year and a layered forecast through 2032 — shows the sector expanding at a 7.5% CAGR, rising from USD 140.0 Million in 2020 to USD 205.0 Million in 2025, and projected to reach approximately USD 338.3 Million by 2032. This release highlights the strategic value of our full report for corporate decision-makers while deliberately withholding detailed segment breakdowns to encourage direct access to the comprehensive dataset and distribution maps.

Executive snapshot: Why 2026 matters

2026 is the year that early-stage regulatory expectations and capital-cost pressures translate into board-level decisions. The virus filtration market is no longer a niche risk-mitigation line item — it is an operationally critical, investment-sensitive component of biologics and plasma-derived product manufacturing. Our analysis identifies three immediate drivers shaping strategic choices this year:

- Regulatory tightening and orthogonality expectations that elevate virus filtration from best practice to governance requirement;

- Process intensification and the adoption of high-throughput biologics production that demand filters offering higher flux, robust small-virus clearance, and predictable scale-up behavior;

- Supply-chain concentration and capacity openings that create first-mover advantages for players securing validated supply lines and second-source strategies.

These dynamics create a compressed decision window for capital deployment in 2026: companies that move earlier to secure validated suppliers, process-compatible formats, and contingency stock positions materially reduce program timelines and regulatory friction.

Market snapshot: Growth trajectory and practical implications

PW Consulting’s topline trajectory is intentionally blunt: between 2020 and 2025, the market expands from USD 140.0 Million to USD 205.0 Million. Under our base-case scenario (2026–2032), the market grows at a 7.5% CAGR to roughly USD 338.3 Million by 2032. The practical implications are threefold for leadership teams:

- Budgeting. Maintenance of validated virus filtration steps becomes a multiyear capital and operating expense line requiring predictable, contractually secured supply and lifecycle plans.

- Portfolio prioritization. Given constrained internal capacity, firms must prioritize which programs adopt next-generation filters vs. incremental upgrades to existing assets, balancing time-to-clinic with long-term cost-per-dose.

- Procurement strategy. Spot-buying risk is rising as manufacturing capacity tightens for specific filter formats and membrane technologies; strategic sourcing and supplier development are now value-creation levers.

Readers seeking the full regional and application distribution charts, including our scenario matrices and sensitivity analysis, are invited to view the complete study: Access the full report .

Regulatory and technical context shaping 2026 decisions

Regulatory agencies (FDA, EMA) continue to emphasize robust viral safety demonstration, with virus filtration commonly forming a required orthogonal layer alongside virus inactivation and chromatography. Practical consequences for manufacturers include more rigorous demonstration of small-virus log reduction values (LRVs) in scaled processes and the need to manage post-approval change pathways carefully as filters evolve.

- Validation burden: New filter generations with different membrane chemistries can materially change fouling behavior and throughput; validation strategies must incorporate scale-down models and worst-case fouling scenarios.

- Compliance risk: Post-approval changes to filter specifications or suppliers require structured change control and regulatory dossiers; this increases program timelines if not planned proactively.

- Technology adoption: Recent product introductions and facility expansions are shifting the balance toward higher-flux, modified membranes that promise throughput gains but require updated process characterization data.

Notably, industry publications and product announcements in 2024–2025 have signaled a wave of second-generation filter technologies offering up to an order-of-magnitude improvements in specific throughput metrics. These innovations accelerate the urgency for firms to reassess both process design and supplier roadmaps in 2026.

Supply-chain and technology playbook: What the report provides

The PW Consulting report is designed as an operational blueprint for 2026 decision-makers. It includes pragmatic, implementable tools rather than theoretical overviews:

- Supply-chain maps that trace critical raw-material flows, single-source pinch points, and validated component suppliers to highlight where near-term capacity risk is concentrated;

- BOM (bill-of-materials) decomposition logic showing how filters’ downstream cost-per-dose evolves with membrane area, housing formats, and sterilization pathways;

- Yield-adjustment and fouling models that help project managers stress-test process throughput under realistic impurity loads and hold times;

- Technology roadmaps that juxtapose membrane-chemistry trade-offs, scale-up complexity, and anticipated regulatory touchpoints for post-approval change management.

Each tool is tied to actionable decision points—sourcing triggers, validation buffer sizing, and contingency stock thresholds—so that procurement, quality, and process teams can move from analysis to playbook execution within a single planning cycle.

Competitive landscape: Dimensions that matter (not predictions)

Our competitive mapping highlights the structural axes on which market advantage is created. PW Consulting’s interviews and proprietary analyses indicate that successful players exploit one or more of the following defensive and growth strategies:

- Proprietary membrane chemistries and validated retention performance (technical moat) that simplify downstream validation and reduce regulatory friction;

- Manufacturing scale and vertical integration (capacity moat) enabling contractual certainty for large-volume biologics and plasma producers;

- Integrated service capabilities—application support, single-vendor validated systems, and in-line sampling—to secure design wins through lower implementation risk;

- Strategic partnerships with CDMOs and vaccine manufacturers that convert early-adopter design wins into long-run revenue streams.

PW Consulting has assessed the competitive postures of leading suppliers—ranging from long-standing membrane specialists to integrated life-science system providers—and identifies Design Win determinants that consistently tilt selection decisions in favor of particular vendors. These determinants include demonstrable small-virus LRV under process-representative fouling, ease of scale-up from bench to process, validated sterilization and holding compatibility, and a supplier’s ability to deliver supply security under commercial timelines. For the specific company profiles, product positioning, and recent moves that inform these assessments, please consult the full report: Access the full report .

Recent industry movements: signals for 2026 strategies

Several 2024–2025 events crystallize the near-term operating environment:

- Product launches of next-generation filters have materially shifted throughput and validation expectations across pipelines; these launches accelerate consideration of post-approval change strategies.

- Capacity expansions at specialized membrane production sites create supply opportunities—but also demand a re-evaluation of qualified-supplier lists and contingency plans.

- Regulatory discussions and conference guidance emphasize multi-layer viral safety, reinforcing the centrality of virus filtration in product dossiers and manufacturing design packages.

These signals are not isolated product stories; they represent regime change in how procurement, validation, and program management teams evaluate vendor selection and lifecycle planning in 2026.

Methodology: Research rigor and how we source non-public signals

PW Consulting’s conclusions rest on a layered-triangulation methodology that combines quantitative market modeling with qualitative primary intelligence. Key methodological pillars include:

- Patent and technical literature analysis to track membrane chemistry innovation and performance claims across manufacturers;

- Supply-chain mapping and BOM teardown exercises, performed with anonymized procurement datasets and validated against plant-level interviews;

- Customer and supplier interviews, including CDMO process engineers and quality leads, conducted under confidentiality agreements to surface lead-time, qualification, and fouling experience;

- Benchmark validation against public company filings, regulatory guidance, and purchase-order aggregation to triangulate demand-side signals.

We emphasize that several of the most consequential insights in our report come from structured interviews and supplier-side disclosures not available in public filings. Our role is to synthesize those signals into decision-grade frameworks while preserving source confidentiality and commercial sensitivity.

Actionable strategic guidance for 2026

For executives and investment committees, PW Consulting recommends the following prioritization roadmap in 2026:

- Immediate risk triage: Identify critical programs where filter supply is on the critical path and establish multi-year purchase agreements or validated second sources;

- Validation optimization: Invest in scale-down models and worst-case fouling characterization now to reduce approval latency for adopting higher-flux filters;

- Capex alignment: Reassess short-term capital projects against the expected throughput and cost-per-dose improvements offered by next-generation membranes;

- Regulatory engagement: Pre-position regulatory submissions to address post-approval change pathways for new filter chemistry adoption, reducing time-to-market risk.

These are practical, prioritized steps designed to convert market growth and technological shifts into defensible commercial advantage.

Next steps and how to obtain the full intelligence

PW Consulting’s comprehensive Virus Filtration Market report contains the complete data tables, regional and application distributions, supplier scorecards, and actionable playbooks referenced in this release. For procurement directors, process leads, and corporate strategists planning 2026 capital allocation or M&A moves, the full dataset provides the evidence base required for board-level decisions.

To access the full report and interactive dashboards: View the full Virus Filtration Market report .

For detailed analysis of this topic, please visit the official page: Virus Filtration Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.