PW Consulting Forecast: Unattended Ground Sensor Market to Expand at a 4.8% CAGR Through 2032

Unattended Ground Sensor Market Outlook 2026: Strategic Imperatives for Capital Allocation

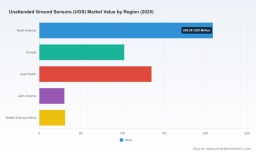

In 2026 the Unattended Ground Sensor (UGS) market is a mature but still-evolving segment of defense and security electronics, characterized by steady expansion and accelerating technology substitutions. PW Consulting’s new market study uses 2025 as the base year and traces the market through a six-year forecast horizon. The global UGS market grows at a compound annual growth rate (CAGR) of 4.8% from the 2025 baseline of USD 554.0 Million, projecting toward a market size of approximately USD 774.1 Million by 2032. For boards, private equity, and corporate strategy teams preparing capital allocation decisions in 2026, these topline dynamics frame both opportunity and near-term execution risk.

Unattended Ground Sensor Market

Executive snapshot: why 2026 is decision-critical

Investment and procurement windows are concentrated in 2026 as several defense programs transition from prototyping to low-rate production and as civilian security budgets prioritize persistent autonomous sensing. The market’s steady growth masks pockets of rapid change — including a shift toward multimodal sensing suites, tighter integration into ISR networks, and an industry-wide re-focus on lifecycle cost-of-ownership rather than unit price. PW Consulting’s report quantifies these transitions and models the downstream cost and operational impacts that will determine winners in upcoming award cycles.

Unattended Ground Sensor Market

Market forces shaping 2026 strategy

Multiple structural and tactical drivers converge in 2026 to create a narrow window for decisive action:

Unattended Ground Sensor Market

- Defense procurement momentum: sustained DoD and allied defense buys continue to be primary demand drivers, increasingly favoring systems that demonstrate networked interoperability and reduced logistical footprint.

- Technology substitution: advances in edge AI and sensor fusion are compressing the feature-to-price tradeoff, enabling smaller sensor packages to deliver more discriminative detection and classification.

- Supply-chain fragility: reliance on a small set of long-endurance battery chemistries and specialty components concentrates sourcing risk and elevates the value of secured upstream supplier relationships.

- Regulatory and export controls: ITAR and export-control regimes remain material constraints on program structuring and partner selection, prompting many buyers to evaluate non-ITAR pathways for allied sales.

- Operational economics: purchasers are prioritizing total lifecycle cost, including field-reliability and yield-adjusted replacement rates, over headline procurement cost.

What PW Consulting’s tools deliver — practical, executable intelligence

Our report is intentionally operational. Beyond market sizing, it equips commercial and engineering teams with repeatable tools and models designed for 2026 implementation planning:

- Supply-chain topology maps that identify single-source nodes, alternate qualified suppliers, and candidates for dual-sourcing to mitigate procurement risk.

- BOM teardown logic and cost-driver frameworks that translate component-level changes into program-level P&L impacts without exposing confidential supplier pricing.

- Yield-adjustment models and failure-mode sensitivity analyses that let production managers evaluate the cost-return of yield improvement investments at typical contract volumes.

- Technology roadmaps that align sensor modalities, edge compute capabilities, and communications stacks to likely program requirements over the forecast window.

- Compliance and export-control playbooks that map regulatory constraints to practical sourcing and partnership options.

These tools are designed to be plugged into 2026 capital planning cycles, enabling finance, procurement, and product teams to move from hypothesis to procurement-ready decisions faster and with quantifiable risk-reduction metrics.

Competitive dimensions: how established players are differentiated

The UGS vendor landscape is characterized by a mix of specialist sensor houses, large defense primes, and system integrators. Competition is not purely price-driven; it is multidimensional. PW Consulting’s analysis focuses on the defensive moats and winning conditions that determine design-wins and program longevity.

- Technology moat: Some vendors differentiate through proprietary signal-processing algorithms, miniaturized seismic/acoustic sensors, or hardened packaging that performs reliably across extreme environments. These capabilities control detection error rates and reduce support cost over time.

- Integration moat: Vendors who provide robust interoperability with broader ISR networks — including secure comms and standardized data formats — secure higher-value program roles beyond point sensors.

- Supply-chain moat: Firms that own or tightly control production of critical components (for example, custom ASICs or long-life power systems) can protect margins and sustain delivery through procurement cycles.

- Programmatic moat: Experience managing government contracting lifecycles, including field trials, logistics, and sustainment, creates a practical barrier to entry for pure-play newcomers.

Key industry participants display varied mixes of these moats. Specialist companies are strong on sensing performance and low-power operation; defense primes emphasize systems integration and network interoperability; mid-sized suppliers secure program positions through rapid fielding and flexible contract execution. Recent evidence of this dynamic includes contract awards and trade-show demonstrations that signal active program positioning and momentum among vendors.

For executives tracking competitive activity, PW Consulting profiles these firms qualitatively and maps competitive vectors rather than publishing prescriptive 2026 strategy forecasts. For readers seeking the detailed company-by-company scenario analysis and our confidential scoring of competitive factors, consult the full report at https://pmarketresearch.com/auto/unattended-ground-sensors-ugs-market.

Regulatory, material and operational headwinds — why timing matters

Three non-technical constraints materially affect near-term returns and should influence 2026 capital allocation:

- Export-control complexity (notably ITAR): program structure and partner selection must be planned with export regimes in mind; pursuing non-ITAR-capable solutions can accelerate allied sales but often requires product redesign.

- Battery and component sourcing: the sector’s dependence on long-life battery chemistries and specialized passive components creates concentration risk; securing upstream supply is often a multi-quarter negotiation with margin implications.

- ESG and lifecycle compliance: defense and civilian buyers increasingly require supply-chain transparency, end-of-life disposal plans, and conflict-minerals reporting as part of procurement evaluation criteria.

These headwinds amplify the value of early, informed engagement with suppliers and the adoption of product architectures that reduce single-point supply dependencies.

Methodology: how PW Consulting constructs actionable truth

Our findings are underpinned by a layered triangulation methodology designed for contested and partially opaque markets. Primary inputs include structured interviews with procurement officials, integrator engineering teams, and tier‑1 suppliers; proprietary BOM tear-downs of representative sensor units; and contract-window analysis that maps public awards to likely production profiles.

We augment primary research with patent-citation analysis to reveal technology adoption pathways and with cross-referenced supply‑chain datasets to identify single‑source risks. Wherever possible, we validate model outputs against program delivery records and field-test reports. This approach allows us to surface non-public commercial cues — such as supplier substitution patterns and engineering trade-offs — while preserving client confidentiality and avoiding disclosure of sensitive transactional data.

Practical strategic recommendations for 2026

For executive teams deciding on investment, procurement, or divestiture in 2026, PW Consulting prioritizes a set of near-term actions that materially improve optionality and reduce downside risk:

- Prioritize modular, multi-modal sensor architectures to preserve upgrade paths for edge-AI and communications improvements without full product redesign.

- Secure alternate supply for high-risk components (notably power sources and RF front-end parts) via qualified second-source agreements or captive inventory programs.

- Shift procurement evaluation criteria from unit price to lifecycle cost metrics that incorporate expected field replacement rates and yield-related sustainment costs.

- Build compliance-by-design into procurement and supplier selection processes to accelerate exportable product configurations for allied sales.

- Invest selectively in edge-processing capabilities that reduce bandwidth and increase classification accuracy, thereby enabling higher-value system roles within ISR architectures.

These steps reduce program risk and enhance competitiveness in a market where modest performance differentials translate into sustained program positions.

Closing: how to use this intelligence now

PW Consulting’s Unattended Ground Sensor market study is structured to move decision-makers from strategic intent to executable plans during 2026. Its mix of macro forecasting, operational tools, and competitive intelligence is tailored to the practical needs of program managers, procurement leads, and investors. For a full breakdown of the segmentation maps, regional distribution, detailed supplier scorecards, and our scenario-based contract forecasts, access the complete report: https://pmarketresearch.com/auto/unattended-ground-sensors-ugs-market.

For detailed analysis of this topic, please visit the official page: Unattended Ground Sensor Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.