PW Consulting: High-Speed Surgical Drill Market Poised to Rise from USD 215.0 Million in 2025 to USD 344.8 Million by 2032, Growing at a 7.0% CAGR

Worldwide High Speed Surgical Drill Market — Strategic Outlook for 2026

Executive summary

PW Consulting’s latest market research positions the worldwide high speed surgical drill market at a structural inflection point in 2026. The market is expanding from a 2025 base of USD 215.0 Million to an expected USD 344.8 Million by 2032, which equates to a sustained compound annual growth rate of 7.0% through our forecast window. This trajectory is driven by converging forces: procedure volume recovery, modular electrification of OR toolkits, and tightening regulatory and ESG requirements that re-price supplier risk across the value chain.

High Speed Surgical Drill Market

Our analysis is intentionally selective in this public summary: we expose the directional drivers and competitive dimensions that will shape capital allocation decisions in 2026, while retaining granular regional, application and customer-level splits inside the full report to preserve commercial integrity and encourage direct engagement.

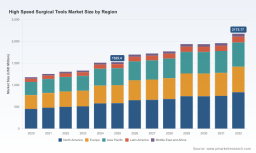

Market trajectory (2020–2032): headline view

The market demonstrates steady, double-digit recovery momentum following pandemic-related disruptions. Key annual checkpoints (rounded to one decimal) are: 2020 = USD 163.2M; 2021 = USD 168.0M; 2022 = USD 181.8M; 2023 = USD 187.6M; 2024 = USD 197.7M; 2025 = USD 215.0M; 2026 = USD 222.3M; 2027 = USD 247.9M; 2028 = USD 260.3M; 2029 = USD 279.1M; 2030 = USD 292.0M; 2031 = USD 314.0M; 2032 = USD 344.8M.

- Implication 1 — Scale and timing: The 2026 inflection represents a window where first-mover investments in modular electric and battery platforms can compound returns before technology parity compresses margins.

- Implication 2 — Concentration: The market remains moderately fragmented (CR3 = 24.6%, CR5 = 26.2%), implying that design wins and channel relationships — not mere scale — determine commercial leadership.

Growth drivers and structural shifts

Growth in 2026 is not mono-causal. PW Consulting identifies several high-conviction structural drivers that are actionable for investors and corporate strategy teams.

- Procedure mix evolution — a rising share of minimally invasive and image-guided procedures increases demand for high-torque, navigation-compatible drills.

- Electrification & portability — the premium on battery life, torque management, and sterilizable modular components accelerates retrofit and replacement cycles in hospital fleets.

- Supply-chain re-shoring and dual-sourcing — geopolitical risk and material price volatility push buyers toward vendors with transparent BOMs and verified second‑tier suppliers.

- Regulatory and sterilization constraints — new scrutiny on sterilization chemistries and polymer residuals forces design changes that materially affect unit costs and time‑to‑market.

- Service economics — remote diagnostics and outcome‑linked service contracts are shifting revenue models from transactional device sales to annuity-like service streams.

Competitive landscape — dimension-based analysis

Leading incumbents remain diverse in geographic reach, channel strength, and product design philosophies. Our report profiles major OEMs and highlights the defensive moats and design-win levers that determine success.

- Technology moat: Firms that own navigation integration, sterilization-validated materials libraries, and modular motor architectures win preference with hospital systems seeking lifecycle predictability.

- Channel moat: Companies with deep trauma and ortho field forces — and those embedded in bundled procurement agreements — capture disproportionate share of retrofit cycles.

- Service moat: Providers that monetize predictive maintenance and instrument-as-a-service models convert higher-priced capital into recurring revenue, improving lifetime margins.

- Regulatory moat: Firms with mature global QMS and demonstrated MDR/FDA audit readiness shorten approval timelines for incremental product variants.

Representative firms in the competitive set include long-established OEMs with market-leading pneumatic and electric platforms, navigation-integrated neurosurgical equipment vendors, and specialist manufacturers of ENT and microdebrider instruments. Recent discrete moves that validate these dimensions include a next‑generation battery/turbine platform launch, FDA 510(k) clearance for navigation-compatible enhancements, and expanded product lines targeting spinal and cranial access. These developments underscore how product architectures and regulatory timing map directly to near-term commercial outcomes.

For a complete competitive map and the companion scoring matrix that underpins our assessment of design‑win probabilities, consult the full report: Full report .

Technology, BOM and supply‑chain levers — what the report delivers

PW Consulting’s deliverables are built for operational execution. The report contains actionable tools that translate market dynamics into procurement, R&D and M&A decision support — without exposing client-sensitive model parameters in this summary.

- Supply‑chain map — end-to-end tiering of critical subcomponents (motors, bearings, polymer housings, precision-turned titanium bits) and supplier risk scoring that highlights single-source exposure.

- BOM teardown logic — normalized cost-builds for electric, pneumatic and battery architectures with sensitivity vectors for key inputs (e.g., medical-grade alloys, motor controllers, sterilizable polymers).

- Yield and cost-to-serve models — configurable levers for process yield, sterilization rework rates, and freight/HS code impacts to estimate landed unit economics under different sourcing scenarios.

- Technology roadmaps — a timeline of plausible platform transitions (hybrid electric-battery, navigation-native interfaces, integrated shaver/debrider modules) and their implied R&D gating milestones.

These tools are purpose-designed to address 2026 pain points such as cost containment under sterilization restrictions, achieving compliance for EU MDR and ISO regimes, and sizing inventory buffers for volatile alloy prices. They are delivered as Excel‑based models and interactive decision trees in the full report.

Regulatory, reimbursement and materials context

Compliance and reimbursement are central to capital planning in 2026. Key operational constraints that shape near-term product architecture and supplier selection include:

- Quality systems and sterilization standards — ISO 13485 and steam sterilization validation requirements materially affect material selection and sterilization-process engineering.

- Regional device regulation — EU MDR surveillance and FDA 510(k) pathways introduce timing and documentation costs that should be built into go‑to‑market timetables.

- Sterilization chemistry risk — growing scrutiny around EtO residuals constrains polymer choices and favors designers with validated low‑residual sterilization protocols.

- Reimbursement dynamics — inpatient coding conventions require alignment of capital and service bundles to capture full procedure economics in hospital contracting.

- Raw material volatility — medical‑grade titanium alloy pricing and availability require procurement hedges and supplier qualification strategies to avoid production interruptions.

Methodology — layered triangulation and proprietary inputs

PW Consulting’s conclusions rest on a multi‑layered evidence base. We combine primary interviews with hospital procurement leaders, OEM engineering and procurement teams, and Tier‑1 supplier executives with direct observation from BOM teardowns conducted in accredited labs.

We then apply a layered triangulation methodology: patent citation network analysis to map technology trajectories; regulatory filing mining to validate clearance timing; hospital procedure-volume datasets to anchor market consumption; and confidential supplier pricing panels to estimate cost structures. Proprietary adjustment routines reconcile divergent inputs and quantify model uncertainty; the result is a set of scenario-ready outputs that clients can operationalize for 2026 capital planning.

Strategic implications for 2026 decision-makers

For corporate and financial leaders allocating capital in 2026, PW Consulting recommends a prioritized playbook that balances optionality with execution discipline:

- Prioritize platform modularity — invest in motor and control modules that can be reused across electric and battery variants to shorten validation cycles and spread R&D amortization.

- Trade regulatory speed for service depth — where approval timelines constrain market entry, compensate with enhanced service contracts and predictive maintenance offerings to protect margins.

- Hedge critical materials — secure multi‑tier supply and explore long‑term purchase agreements for medical‑grade alloys and specialty polymers to tame input cost volatility.

- Accelerate sterilization‑aware design — redesign polymer interfaces and seals for validated low-residual processes to avoid costly post-market actions and sterile processing bottlenecks.

- Embed ESG and trade compliance — build traceability into supplier contracts to pass audit and procurement screens increasingly used by hospital systems and government payers.

These moves are not mutually exclusive; the report provides a prioritized roadmap and ROI sensitivities to help teams choose the optimal sequencing based on balance-sheet strength and go‑to‑market capabilities.

How to use this research in 2026

Use PW Consulting’s models to stress-test acquisition targets, inform pricing under service-based commercial models, and select the supplier networks that reduce go‑to‑market friction. Our interactive dashboards allow scenario toggling for sterilization rules, regional regulatory timing, and battery‑lifecycle economics so that investors and management teams can quantify outcomes before committing capital.

Access the detailed distribution maps, competitive scoring, and executable cost models here: Full report .

For detailed analysis of this topic, please visit the official page: High Speed Surgical Drill Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.