PW Consulting: Creatine Market Poised to Reach USD 980.0 Million by 2032 on a 13.5% CAGR

PW Consulting: Creatine Market 2026 — Strategic Imperatives for Capital Allocation

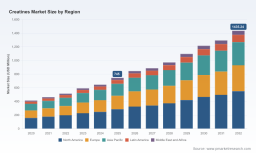

PW Consulting publishes a targeted industry briefing on the global creatine market at a pivotal moment in 2026. Our analysis uses 2025 as the calibration year and projects the market through 2032. The global creatine market is growing rapidly: from USD 490.0 Million in 2025 it expands to an estimated USD 565.1 Million in 2026 and follows a high-growth path to reach roughly USD 980.0 Million by 2032, reflecting a compound annual growth rate (CAGR) of 13.5% over the forecast horizon. For corporate decision-makers allocating capital in 2026, these macro dynamics create both opportunity and execution risk — and they demand a tightly prioritized response.

Creatine Market

Executive snapshot: Why 2026 is a decisive year

The market’s current trajectory is not incremental; it is structural. Demand-side drivers (premiumization of sports nutrition, next-generation delivery formats, and measured clinical use cases) intersect with supply-side reshaping (environmental regulation, factory consolidation, and cost inflation). At the same time, geopolitical trade measures and evolving certification regimes are changing effective sourcing economics for firms that rely on cross-border ingredient flows. Collectively, these forces compress the window for strategic moves — procurement agreements, capacity investments, certification programs, or M&A — into 2026 if companies want to secure defensible cost and supply positions before the next phase of price discovery.

Creatine Market

Key growth vectors (scannable)

- Product innovation: new delivery formats and formulation adjacencies (e.g., creatine plus electrolytes, soluble monohydrate) are unlocking incremental demand among mainstream fitness consumers and clinical channels.

- Premiumization and branding: trademarked, high‑purity credentials and third‑party certifications are widening value capture for branded suppliers and contract manufacturers.

- Regulatory and quality re-rating: environmental enforcement and factory exits are reducing low‑grade supply, tightening the market and elevating buyers that can demonstrate pharmaceutical‑grade controls.

- Channel expansion: retail and e‑commerce portfolio expansions by major supplement retailers and new product hubs are accelerating time‑to‑market for differentiated creatine SKUs.

Supply‑side pressures and cost drivers

Procurement and manufacturing officers must treat the supply chain as an active risk vector in 2026. Structural cost elements and policy shifts are reframing what constitutes a resilient sourcing strategy:

- Quality consolidation: enforcement of environmental and social regulations is accelerating the exit of smaller, low‑quality producers, reducing spot capacity and increasing volatility in the short term.

- Labor and input cost normalization: rising compliance costs (social insurance and workforce standards) are translating into higher base production costs for onshore manufacturing hubs.

- Trade friction: duties and tariff reclassifications materially change landed cost math, pushing some buyers to pay premiums for compliant, certified supply or to re‑engineer supply routes.

- Concentration dynamics: a moderate level of top‑tier concentration means design wins and channel access are increasingly decisive for suppliers seeking to scale premium offerings.

What the PW Consulting report delivers — practical tools for the 2026 playbook

Our report is deliberately operational. Rather than presenting only high‑level forecasts, we provide a toolkit designed to be used by procurement, R&D, regulatory, and corporate strategy teams as they execute in 2026. Key deliverables include:

- Supply‑chain topology and vulnerability map that traces material flows, single‑sourcing nodes, and regulatory pain points.

- BOM (bill‑of‑materials) disaggregation logic and scenario templates that show how formulation choices affect landed cost, margin and certification burden without prescribing prescriptive price points.

- Yield‑adjustment and throughput models that convert plant‑level performance assumptions into commercial availability scenarios under different compliance outcomes.

- Technology roadmap and comparative assessment of manufacturing routes, impurities control and downstream processing options to inform capex and partnership choices.

- Commercial playbooks for certification investments (e.g., sport‑certification, GMP alignment, pharma grading) and for negotiating design‑win clauses with major retail and contract manufacturing partners.

Each tool is accompanied by decision templates and sensitivity dashboards so teams can rapidly run "what‑if" scenarios relevant to 2026 capital and procurement cycles.

Competitive dimensions to monitor (not a roster of predictions)

Competitive advantage in the creatine ecosystem is multi‑dimensional. Our analysis focuses on the structural attributes that determine whether a supplier or player wins at scale, rather than attempting to publicize internal strategy playbooks.

- Branded purity and provenance: premium trademarks and a verifiable "made‑in" provenance create a pricing moat in premium segments. Branding and digital relaunches amplify this advantage by improving downstream buyer preference and traceability signalling.

- Regulatory and certification certainty: suppliers with audited GMP, pharma certifications, and third‑party sport certifications effectively lower buyer risk and shorten procurement cycles.

- Scale and supply integration: vertical integration across precursor chemicals, intermediate processing, and formulation can compress cost curves and improve control, especially when tariffs or logistics premiumize local production.

- Channel and formulation design wins: distribution partnerships and co‑development with major retailers and manufacturers create repeatable revenue streams. Design wins are won through a combination of product purity, commercial reliability, and regulatory transparency.

- Operational excellence and yield resilience: plant yield, impurity control, and rapid conversion of capacity changes into reliable supply determine which suppliers can sustain share during cyclical shocks.

Examples of observable market moves in 2026 that illustrate these dimensions include premium brand relaunches at major Western suppliers, new soluble and delivery‑format product announcements from innovators, and retail portfolio extensions that prioritize science‑backed creatine propositions. These developments validate the competitive dimensions above without substituting for the full, vendor‑level diagnostics in our report.

Company archetypes we track

Across our vendor coverage, three archetypes emerge — premium branded Western suppliers with traceability and marketing moats; high‑volume, cost‑efficient manufacturers focused on quality certifications; and specialist distributors and co‑manufacturers that bridge technical and commercial gaps for brands. Monitoring how individual firms reinforce one or more of these archetypes is critical to forecasting access, price, and design‑win probability.

Methodology — how PW Consulting builds a defensible intelligence set

Our approach blends quantitative triangulation with on‑the‑record and confidential qualitative inputs. Core elements include customs and trade flow analysis cross‑referenced with plant‑level capacity mapping, patent and regulatory filing reviews, targeted interviews with procurement and quality leads across ingredient buyers and sellers, and on‑site validation at production facilities and trade shows. We apply a layered triangulation process that weights independently verifiable datapoints against proprietary supplier interviews and third‑party certification records to reduce bias and surface actionable signals.

Where public data is thin, we use supply‑chain forensics — component shipment tracking, input pricing proxies, and formulation reverse engineering — to identify near‑term bottlenecks and margin pressure points. All proprietary insights are surfaced in anonymized, decision‑ready dashboards that support negotiation, sourcing, and M&A diligence workflows.

Practical recommendations for corporate leaders in 2026

Based on our analysis, boards and executive teams should prioritize three near‑term actions:

- Stress‑test sourcing economics against tariff and compliance outcomes. Run live procurement auctions that include compliance‑adjusted landed cost scenarios and evaluate multi‑sourcing as an insurance instrument.

- Invest selectively in certification and traceability where premium positioning is core to your business model; treat certification spend as a capacity creation lever rather than a marketing expense.

- Align R&D roadmaps with channel partners’ needs for novel delivery formats and bundled formulations, and use contingent commercial commitments (design‑win clauses) to de‑risk scale‑up capex.

Where to get the full intelligence

PW Consulting’s full report contains the detailed regional distribution maps, supplier‑level scorecards, BOM templates, and capex trackers that boards and deal teams need to act in 2026. For the comprehensive dataset, proprietary supplier analyses and the actionable scenario models referenced above, explore the full report here: Explore the full PW Consulting Creatine Market report .

Final thought — the timing window for capital allocation

2026 is not a year to defer decisions. Market expansion is substantial and rapid, but it is accompanied by supply consolidation and regulatory recalibration that increase the payoff to well‑timed investments and the penalty for indecision. Corporates that combine rigorous supplier due diligence with targeted investments in certification, formulation innovation, or secured capacity will convert systemic growth into durable competitive advantage. PW Consulting’s report is designed to make those choices measurable and executable.

For detailed analysis of this topic, please visit the official page: Creatine Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.