PW Consulting: Dialysis Water Treatment Systems Market to Expand at a 7.1% CAGR During 2026–2032

Dialysis Water Treatment System Market — Strategic Briefing for 2026 Capital Decisions

PW Consulting releases a forward-looking industry briefing built on our 2025 base-year market model and a forecast window covering 2026–2032. The global dialysis water treatment system market registers USD 964.6 Million in 2025 and is growing at a compound annual growth rate (CAGR) of 7.1% across the 2026–2032 forecast horizon, reaching an estimated USD 1556.5 Million by 2032. This briefing explains why 2026 is a pivotal year for capital allocation, how senior executives should interpret structural shifts, and what pragmatic tools in our full report materially reduce execution risk. The piece intentionally highlights analytical depth while reserving detailed segment-level distributions for the full report.

Market trajectory and the 2026 decision window

In 2026 the market dynamic is characterized by steady volumetric demand for hemodialysis infrastructure combined with accelerating operational and regulatory pressure on water quality, recovery, and lifecycle cost. Key observations that shape near-term capital choices:

- Regulatory tightening increases compliance costs: AAMI/ISO microbiological and endotoxin action levels are influencing procurement specifications and service regimes.

- Reimbursement headwinds: With no new capital-related TPNIES approvals under Medicare ESRD PPS for CY 2026, providers cannot rely on near-term incremental capital reimbursement to offset higher upfront costs.

- Technology migration: Buyers are showing clear preference for systems that combine high water-recovery RO architectures, validated thermal-disinfection modules, and remote monitoring for automated maintenance.

- Operational intensity: Hemodialysis patients can be exposed to hundreds of liters of treated water per week, so uptime, yield and microbiological control materially affect both patient safety and operating expense.

These forces raise the bar on procurement: buyers must now quantify lifecycle cost under stricter quality tolerances while vendors must demonstrate validated pathogen control, lower total water loss, and deterministic maintenance pathways.

Where value is migrating — a directional view

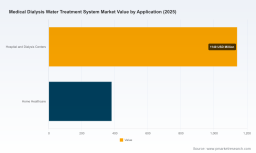

Value in 2026 is shifting along three vectors: product architecture (single vs. multi-stage and thermal vs. chemical disinfection), service models (capex sale vs. performance-based contracts and managed services), and supply-chain resilience (local spares, supplier diversification, and modular designs enabling faster site deployment). Geographies and application centers of gravity are also evolving, but exact regional and application distributions are intentionally omitted here — these are mapped in detail in our full dataset.

For readers wanting the complete geographic and application distribution maps, procurement sizing templates, and interactive scenario charts, see the full report at https://pmarketresearch.com/hc/medical-dialysis-water-treatment-system-market .

Operational toolset included in the full PW Consulting report

Our clients require executable instruments, not only high-level thesis. The report therefore embeds a suite of practical tools designed to convert insight into action for 2026 procurement and operations:

- Supply‑chain topology maps — identify single points of failure across membranes, pumps, control electronics and chemical consumables and the realistic lead-time mitigations for each.

- BOM decomposition logic — an engineered approach to reverse‑calculate cost drivers from vendor BOMs and to estimate substitution impact on yield and CAPEX.

- Yield adjustment and lifecycle cost models — parametric models that translate membrane recovery, disinfection frequency and labor rates into TCO bands usable in vendor scorecards.

- Technical roadmap and migration playbooks — decision trees for retrofits versus greenfield, including modular upgrade paths for thermal disinfection and double-pass RO adoption.

- Design‑win and service economics playbook — quantifies how installation cadence, design validation artifacts and training programs convert into sustainable service revenue.

Each tool is purpose-built to address 2026 pain points—cost containment under unreimbursed capex, compliance with updated microbiological thresholds, and minimizing downtime risk in high-throughput dialysis units—without prescriptive parameter disclosure in this briefing.

Competitive landscape — concentration and competitive dimensions

The market exhibits moderate concentration: the top three vendors account for approximately 45.0% of revenue and the top five for roughly 52.0%. That structure creates a competitive environment where incumbent installed base and service networks confer tangible advantages, but differentiated product and service offers still unlock share gains for agile entrants.

Across the competitive set, we analyze firms along repeatable competitive dimensions rather than publish proprietary growth forecasts. The principal dimensions PW Consulting tracks are:

- Regulatory and clinical validation moat — presence of FDA 510(k) clearances, documented validation in conjunction with AAMI/ISO standards, and published cleaning/disinfection protocols.

- Thermal-disinfection and high‑recover designs — patents and field-proven designs for heat-based disinfection and water-recovery optimizations reduce chemical exposure and ongoing consumable spend.

- Installed-service network and design-win track record — training programs, technician deployment density, and long-term service contracts drive retention and recurring revenue.

- Integration capability — the ability to bundle water systems with dialysis chairs/centrals, bicarbonate dosing, and IT-enabled remote monitoring for predictable operational outcomes.

- Customization and speed-to-site — hybrid engineering capabilities to deliver site-specific wall-boxes and skid-mounted solutions in constrained timelines.

Reading these dimensions across the example companies in our universe yields the following directional observations (high-level):

- Mar Cor Purification (Xylem) leverages turnkey central and portable offerings and extensive technician training to strengthen service moats.

- Fresenius Medical Care benefits from integration with dialysis delivery platforms and an emphasis on resource optimization that appeals to large in‑center operators.

- DWA and Herco concentrate on technical depth—exclusive focus on dialysis water and double‑pass/thermal architectures—creating a product‑technology moat for ultrapure requirements.

- AmeriWater, Specialty Water, Total Water and similar firms offer FDA-cleared products and customization that serve acute-care and retrofit markets where regulatory documentation and speed matter.

- B. Braun and Nipro focus on water recovery and “green” generation systems, aligning with ESG and utility-cost reduction priorities that are increasingly procurement filters.

Recent in-market developments—new product launches and FDA 510(k) clearances—confirm the near-term emphasis on validated thermal/disinfection capabilities and higher-yield RO architectures. For granular company profiles and our scoring across the competitive dimensions, consult the full dataset at https://pmarketresearch.com/hc/medical-dialysis-water-treatment-system-market .

Regulatory and reimbursement context shaping procurement

Regulatory standards and reimbursement structure materially influence vendor selection and lifecycle economics in 2026: AAMI/ISO microbiological and endotoxin action levels are being enforced in purchasing specifications; CMS Conditions for Coverage require compliance with AAMI RD52 or equivalent ISO standards for dialysis facility water quality; and the FDA continues to classify dialysis water systems as medical devices under 21 CFR 876.5665 (Class II, 510(k) pathway). At the same time, the absence of new capital-related reimbursement mechanisms in CY 2026 places greater emphasis on lifecycle ROI modeling and on sourcing approaches that can preserve margin without shifting unacceptable clinical risk to providers.

2026 strategic implications — recommended executive moves

For hospital system procurement leaders, OEMs and private equity investors, PW Consulting recommends a prioritized set of actions for 2026:

- Reweight procurement scorecards toward validated disinfection performance, demonstrable water recovery and vendor service density rather than pure upfront CAPEX beats.

- Insist on BOM-level transparency during negotiations or use our BOM decomposition templates to stress-test supplier bids.

- Negotiate hybrid procurement constructs—capex discount + performance-based service fees—when reimbursement cannot fully cover replacement cycles.

- Invest in predictive maintenance and remote-monitoring retrofits to reduce emergency interventions and extend membrane life.

- Accelerate supplier diversification and local spare-part stocking to mitigate supply-chain lead-time spikes for membranes, pumps and controllers.

- Embed ESG metrics (water recovery, chemical usage, energy demand per treated liter) into vendor selection to capture long-run operating cost reductions and meet institutional sustainability goals.

Methodology and data integrity

PW Consulting’s conclusions rest on a structured, multi-layered research approach we describe as Layered Triangulation. Core elements include: primary interviews with hospital biomedical engineers, dialysis-center operators, and service technicians; structured site audits and time-motion observations of disinfection cycles; procurement invoice sampling and controlled BOM reverse engineering; patent and regulatory-filings analysis (including FDA 510(k) dossiers); and automated analysis of service logs and warranty claims. We integrate these primary inputs with secondary market data and supplier financials, then validate by cross-checking independent data streams to reduce bias and reconcile outliers.

Where public disclosure is limited, we supplement with anonymized vendor contract excerpts and calibrated engineering models to estimate membrane yields and maintenance cadence. This process enables us to produce scenario-grade TCO bands and supplier scorecards that are robust for board-level capital allocation decisions while protecting confidential sources.

Next steps — how to use this briefing

PW Consulting positions this briefing as a strategic prelude: it articulates the market trajectory, competitive dimensions, regulatory inflection points, and practical tools buyers and investors need to act in 2026. To access the full segmentation maps, company scorecards, downloadable BOM templates, and interactive scenario models that underpin the analyses above, please consult the full report at https://pmarketresearch.com/hc/medical-dialysis-water-treatment-system-market .

For detailed analysis of this topic, please visit the official page: Dialysis Water Treatment System Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.