PW Consulting: Disk Stack Centrifuge Market Poised to Reach USD 2,670.0 Million by 2032, Growing at a 5.0% CAGR

Disk Stack Centrifuge Market — Strategic Outlook for 2026 Decision-Makers

The Disk Stack Centrifuge Market report from PW Consulting provides an operationally focused intelligence package designed to inform capital allocation, sourcing, and product roadmap decisions in 2026. Anchored on a 2025 base year and a 2026–2032 forecast window, the study combines time-series market sizing with proprietary supply‑chain forensics and executable playbooks. This article summarizes the high‑level implications and strategic levers for executives while preserving the full, granular datasets and regional/application splits for subscribers.

Market Snapshot (2020–2032)

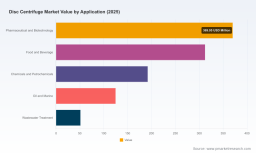

The global market for disk stack centrifuges grows from a measured 1,400.0 Million USD in 2020 to 1,900.0 Million USD in 2025, and the report projects a continuation of that trajectory through 2032, reaching 2,670.0 Million USD under a compound annual growth rate of 5.0% across the forecast period. These headline figures reflect steady demand driven by industrial water reuse programs, pharmaceutical and biotechnology scale‑up, and ongoing modernization in food & beverage processing.

- Demand momentum: accelerated by public programs for wastewater reuse and tightening process‑water standards.

- Cost pressure: material and component inflation — notably stainless‑steel supply constraints — are compressing supplier margins and shifting sourcing strategies.

- Regulatory overlay: new safety and energy mandates in major markets are creating both retrofit opportunities and compliance timelines that will dictate near‑term capex schedules.

Why 2026 Is a Pivotal Year

2026 is a junction of regulation, cost normalization, and technology adoption. Several contemporaneous forces make decisions this year disproportionately impactful for outcomes across the forecast horizon:

- Regulatory deadlines effective within the next 12–24 months change retrofit economics and create waves of compliance demand in regions where machinery safety and energy efficiencies are being updated.

- Trade and tariff dynamics are re‑shaping procurement choices for OEM buyers that source at scale; supply‑side cost shifts (raw materials and freight) increase the value of diversified sourcing and local assembly strategies.

- Energy efficiency benchmarks and unit‑level OPEX are now a first‑order procurement criterion in large industrial accounts; buyers are pricing lifecycle energy performance into RFPs rather than treating it as an optional add‑on.

Report Toolbox — What Practitioners Get

The core strength of the PW Consulting report is its toolbox orientation: each module is designed to be operationally executable by procurement, engineering, and BD teams. Key deliverables include:

- Supply‑chain map: tiered supplier network visualization with component criticality scoring and single‑source risk indicators.

- BOM decomposition logic: method to rebuild a supplier bill‑of‑materials from observable features, inspection data, and component cross‑references for negotiation and cost engineering.

- Yield adjustment models: factory‑level yield and throughput models that translate design choices into expected throughput, spare‑parts needs and service intervals.

- Technology roadmap: scenario‑based trajectories for materials, sealing systems, motor/drives and digital controls that align to 2026 compliance and efficiency targets.

- Total‑cost of‑ownership (TCO) playbook: procurement templates that fold in energy, downtime, spare parts and service models for accurate lifecycle comparisons.

- Compliance & certification matrix: cross‑jurisdictional mapping of the standards that matter for high‑speed centrifuges and the implementation timelines buyers must meet.

Each tool is accompanied by executable next steps — for example, a prioritized list of inspection checkpoints for incoming equipment or a supplier re‑qualification checklist for regulated pharma accounts — but the detailed parameter sets and model inputs are reserved for the full report and interactive deliverables.

Competitive Landscape — Dimensions That Drive Wins

The market is concentrated but not immobile. The leading OEMs and regional specialists demonstrate distinct competitive moats and route‑to‑win behaviors. Our competitive analysis emphasizes the dimensions that determine procurement outcomes rather than publishing prescriptive forecasts for each firm.

- Brand and installed base: incumbents with large installed fleets create lock‑in via spare‑parts depth, training programs and long‑term service contracts.

- Hygienic and certification competencies: firms that consistently achieve GMP and pharmaceutical‑grade hygienic designs convert a larger share of high‑margin bio/pharma RFPs.

- Engineering‑for‑throughput: suppliers that demonstrate higher clarified yields and lower product loss secure design wins in food, beverage and biotech segments.

- Cost and manufacturing footprint: low‑cost manufacturers leverage verticalized supply chains to win on price in commoditized applications, but face tariff and compliance exposure in certain end markets.

- After‑sales and digital services: remote monitoring, predictive maintenance, and onsite overhaul capability are increasingly making the difference in procurement decisions for industrial accounts.

Representative firms we profile include Alfa Laval, GEA Group, Flottweg SE, Pieralisi Group, Huading Separator, Zhangjiagang Peony Machinery and TEMA Separation. For each, the report synthesizes where their structural advantages align to specific applications, what risks are latent in their supply chains, and which commercial behaviors (warranty terms, spare parts policies, retrofit offers) most influence customer selection.

Access the full competitive radar and company matrices to see how each supplier maps to buyer personas and procurement levers in 2026.

Technology Pathways and Investment Priorities

Technology evolution is not a single axis: buyers must balance energy performance, uptime, and regulatory readiness. Practical investment priorities for 2026 are:

- Energy reduction retrofits and motor/drive modernization to meet near‑term efficiency mandates.

- Modularization of core separation assemblies to reduce time‑to‑service and spare parts complexity.

- Hygienic design upgrades that simplify CIP (clean‑in‑place) cycles and reduce product loss — a direct revenue saver for food and pharma clients.

- Digital enablement of predictive maintenance and remote diagnostics to reduce unplanned downtime and optimize service intervals.

- Material substitution strategies and redesigns that lower exposure to stainless‑steel price volatility while maintaining corrosion resistance and cleanliness standards.

Our technology workstream pairs scenario modeling with validated supplier cost curves to show which upgrades pay back within typical corporate planning horizons; the detailed ROI matrices and retrofit case studies are available in the report. For a guided walkthrough of which pathways are relevant to particular operating profiles, consult the interactive roadmap here: Disk Stack Centrifuge Market — Full Report .

Regulatory, Raw Material and Trade Dynamics

Three non‑market forces materially influence near‑term choices:

- Regulations: updated machinery directives and local safety requirements impose retrofit schedules that create deterministic demand waves for compliant equipment and documented safety validation.

- Raw materials: stainless‑steel price spikes and supply constraints are increasing the value of engineering alternatives and secondary sourcing strategies.

- Trade policy: elevated tariffs and import restrictions in certain jurisdictions are reconfiguring sourcing and local content decisions for large projects.

These constraints are already influencing lead times, capital budgets and procurement tender language in 2026; firms that proactively restructure supply lines and prioritize energy‑efficient retrofits will capture outsized near‑term value.

Methodology — Why Our Findings Are Actionable

PW Consulting applies a layered triangulation methodology combining: patent and standards citation analysis, customs and trade flow records, anonymized interviews across OEMs and tier‑1 customers, physical BOM deconstruction from sampled equipment, and factory visits with calibration against public tender outcomes. We quantify uncertainty through scenario ranges rather than single‑point estimates and validate model outputs against multiple independent data channels.

Critically, much of the insight in this report arises from reconciled non‑public sources: supplier quotes, anonymized service histories, and proprietary component price indices. These inputs are weighted and reconciled through cross‑validation so that negotiated procurement levers and retrofit ROIs reflect realistic in‑market behaviors rather than theoretical constructs. The full methodology appendix documents weighting schemes and validation checkpoints for governance purposes.

Actionable Guidance for 2026 Executives

For capital allocators, procurement leads, and plant engineering heads, the actionable implications are clear:

- Prioritize retrofit projects that deliver both compliance and a path to reduced lifetime energy consumption; these provide defensible near‑term returns under tightened regulatory regimes.

- Diversify sourcing to mitigate tariff and raw‑material shocks, but preserve a service‑led relationship with incumbents that hold installed‑base advantages.

- Use BOM and yield models to instrument supplier negotiations; margin extraction opportunities are largest where buyers can credibly replicate a supplier’s cost drivers.

- Accelerate pilot deployments of digital monitoring at scale to convert anecdotal uptime gains into contractually certified SLA improvements.

Next Steps — How to Engage PW Consulting

PW Consulting provides tailored briefings, supplier negotiation playbooks, and retrofit prioritization workshops based on the full dataset and models in the report. For a complete breakdown of regional and application distributions, granular TCO models, and the company‑level scorecards referenced above, please visit the report page and request access: https://pmarketresearch.com/worldwide-disc-centrifuge-market-research .

For detailed analysis of this topic, please visit the official page: Disk Stack Centrifuge Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.