PW Consulting: Tinplate Market Poised for Steady Growth with 3.3% CAGR, New Report Finds

Global Tinplate Market 2026: Strategic Imperatives from PW Consulting

PW Consulting’s latest Tinplate Market Research (base year 2025; historical window 2020–2025; forecast period 2026–2032) delivers a focused, actionable intelligence package for executive teams allocating capital, negotiating supplier agreements, and setting product roadmaps in 2026. The global tinplate market is now moving through a period of measured growth (CAGR 3.3%), with our model projecting a recovery and re‑rating window across the forecast horizon. This release summarizes the strategic takeaways from the report while reserving detailed segment matrices and precise design‑win level metrics for the full publication.

Executive Snapshot

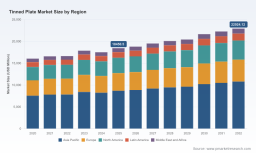

The market is sizable and resilient: PW Consulting estimates global tinplate industry revenue at USD 29,650.0 Million in 2025, progressing to an interim 2026 estimate of USD 30,070.7 Million under our base case. Growth is supported by stable demand in packaging end‑markets, selective automotive and industrial applications, and ongoing product innovation in lightweight and corrosion‑resistant grades. Industry concentration is meaningful: the top three suppliers account for roughly 55.0% of supply by capacity, and the top five for about 68.0% — a structure that privileges scale, integrated feedstock access, and regulatory compliance as competitive levers.

Why 2026 Is a Pivotal Year for Capital Allocation

Several converging forces make 2026 the inflection point for investment and sourcing decisions in tinplate:

- Raw material volatility: Tin price spikes (LME tin cash settlement peaked at USD 32,110.0/mt in October 2024) and elevated hot‑rolled coil (HRC) reference levels (approx. USD 650.0/mt CFR Asia in late 2024) compress margins and force supply‑side reconfiguration.

- Trade and compliance headwinds: The EU’s Carbon Border Adjustment Mechanism (CBAM) comes into direct effect in 2026 for steel imports, reshaping landed cost math for exporters and incentivizing low‑carbon feedstock strategies.

- Market concentration and regional policy: Persisting trade measures (US Section 232 duties) and national emissions targets (e.g., China’s dual carbon goals to reduce production emissions by 10.0% by 2025) are driving capacity relocations, brown‑to‑green retrofits, and selective vertical integration.

Taken together, these dynamics make precise supplier mapping, cost‑to‑serve modeling, and regulatory compliance scenarios essential for any C‑suite planning CAPEX or M&A in 2026.

What the PW Consulting Report Delivers — Practical Tools for 2026 Execution

This study is deliberately practical. Beyond market numbers and high‑level trends, the report includes a suite of operational tools designed to be plugged into 2026 decision workflows:

- Supply‑chain topology and heat maps that identify single‑point‑of‑failure mills, alternative sourcing corridors, and carbon‑intensity vectors for landed tinplate.

- BOM disassembly logic that translates tinplate composition and coating grades into cost buckets relevant to packaging converters and OEMs, enabling rapid scenario modeling for grade swaps or light‑gauge substitutions.

- Yield and loss adjustment modules that quantify conversion yield sensitivity across coating processes and forming operations — critical for near‑term margin recovery when raw material prices spike.

- Technology and decarbonization roadmap templates that map investment timing, expected throughput gains, and compliance milestones required to mitigate CBAM exposure.

Each tool is accompanied by implementation guidance (data inputs, level of internal effort, and quick‑win thresholds) so procurement and operations teams can apply the analytics without waiting months for bespoke consultancy work. For full model access and customizable spreadsheet versions, see the complete research package at https://pmarketresearch.com/worldwide-tinned-plate-market-research .

How These Tools Solve 2026 Pain Points

- Cost control under volatility: BOM and yield models allow teams to simulate alternative alloy and coating routes, quantify incremental forming losses, and set pass‑through thresholds for price negotiations.

- Trade and compliance readiness: Supply‑chain topology coupled with carbon‑intensity mapping highlights where CBAM or tariffs materially change supplier economics, enabling hedge or relocation decisions in 2026.

- Design‑win acceleration: Technology roadmaps and grade‑spec crosswalks identify immediate product modifications (e.g., lightweight grades or tin‑substitutes) that reduce material cost and increase conversion yield without triggering requalification delays.

Competitive Landscape — Dimensions of Advantage, Not Predictions

Our coverage includes detailed, source‑verified profiles of the sector’s largest players. Rather than offering prescriptive 2026 strategies for each firm, the report analyzes the structural dimensions that determine winners and losers over the near term. These dimensions include:

- Feedstock integration: Players with upstream access to low‑carbon steelmaking routes or captive refinery arrangements preserve margin resilience when tin or coil prices spike.

- Scale and footprint flexibility: Multi‑regional mill networks enable rapid reallocation of volumes to avoid tariffs or local emissions penalties; footprint matters more than ever under differentiated regulatory regimes.

- Product and processing moats: Proprietary electrolytic coating technologies, tin‑free surface chemistries, and high‑yield grade formulations act as barriers to entry for converters requiring tight tolerance and long qualification cycles.

- Design‑win mechanics: For packaging OEMs, the decisive factors for supplier selection are consistent coating performance, certification pedigree (food safety, recyclability), and demonstrated short‑lead responsiveness in peak demand windows.

Companies we profile (including global integrated steel producers, specialized tinplate mills, and vertically integrated packaging suppliers) are assessed against these dimensions. Recent market moves — such as announced capacity expansions for low‑carbon output, premium grade launches, and selective price adjustments — validate the importance of each competitive axis without disclosing proprietary projections.

To review the supplier scorecards and the underlying sourcing decision framework, visit our detailed analysis at https://pmarketresearch.com/worldwide-tinned-plate-market-research .

Methodology — Why Our Findings Are Actionable and Verifiable

PW Consulting applies a Layered Triangulation methodology to ensure rigor and traceability:

- Primary supply‑side verification: plant tours, technical interviews with mill operations and quality leads, and anonymous buyer interviews with packaging converters.

- Patent and standards analysis: review of recent electrolytic coating patents, technical certifications, and coating chemistry filings to map technological differentiation and time‑to‑market for new grades.

- Transactional triangulation: synthesis of trade flows, customs mirror data, and commercial tender outcomes to validate capacity utilization and effective market shares.

Where public data is sparse, we employ calibrated proxying and non‑attributable supplier benchmarking — methods that allow us to surface reliable insights about yield curves, downtime risk, and supplier compliance posture without publishing commercially sensitive numbers. Our approach explains how we access non‑public signals (confidential interviews, reverse‑engineered BOMs, and plant performance diaries) while preserving source anonymity and commercial confidentiality.

2026 Strategy Playbook — Practical Moves for Executives

For leadership teams planning capital deployment or supply re‑negotiation in 2026, the report organizes recommended moves into four tactical buckets:

- Short horizon (0–12 months): lock conditional supply agreements with carbon‑verified volumes, deploy BOM swaps for immediate cost relief, and stress‑test contracts with yield‑sensitivity clauses.

- Medium horizon (12–36 months): prioritize partnerships with mills investing in low‑carbon capacity, co‑fund pilot lines for lightweight grades, and restructure logistics to minimize tariff exposure.

- Operational playbook: implement yield tracking KPIs, escalate quality gates around electrolytic coatings, and standardize requalification tests to cut time‑to‑market for grade changes.

- Portfolio resilience: evaluate options for partial vertical integration where scale economics and regulatory arbitrage make captive sourcing superior to spot procurement.

Each recommendation is accompanied in the full report by an implementation checklist and a decision matrix that maps investment size to expected P&L sensitivity under alternative tin and HRC price scenarios.

The Bottom Line for 2026

2026 is not a year for passive observation. With volatile raw materials, new trade‑compliance regimes, and measurable concentration in supply, companies that adopt a data‑first procurement posture and integrate technical yield analytics into commercial negotiations will preserve margin and protect market share. PW Consulting’s Tinplate Market Research provides the calibrated scenarios, operational templates, and supplier intelligence to do exactly that — while the full set of segment tables, supplier scorecards, and downloadable models remain available in the complete report.

Access the full research bundle, including customizable Excel models and supplier scorecards, at https://pmarketresearch.com/worldwide-tinned-plate-market-research .

For detailed analysis of this topic, please visit the official page: Tinplate Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.