PW Consulting: Diaper Bags Market at USD 820.0 Million in 2025, Poised to Reach USD 1,064.6 Million by 2032 at a 3.8% CAGR

Diaper Bags Market 2026: Strategic Imperatives for Growth and Resilience

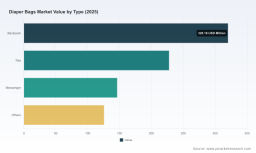

As PW Consulting’s senior industry analyst, I am pleased to present a strategic preview of our latest Diaper Bags Market report — a timely intelligence package designed to inform executive decisions in 2026. The global market has shown steady expansion, rising from approximately USD 700 million in 2020 to an estimated USD 820 million in our 2025 base year, and is projected to grow at a compound annual growth rate (CAGR) of 3.8% through the 2026–2032 forecast horizon. By 2032, our topline projection points to a market approaching the mid‑billion dollar range, underscoring continuous opportunity for incumbents and newcomers alike.

Diaper Bags Market

Why this report matters for 2026 decision-makers

- Timing and context: Companies entering 2026 face a mature but evolving product landscape. Growth is steady rather than explosive, making disciplined allocation of capital and focused product differentiation essential.

- Actionable strategy, not theory: Our analysis unpacks where value is being created today — from product ergonomics to channel execution and manufacturing footprint — and translates that into prioritized, executable initiatives for 2026 planning cycles.

- Risk‑adjusted roadmaps: With raw material volatility and packaging EPR regulation rising on the agenda, the report offers scenario-based investment playbooks that balance margin protection with market share ambitions.

Core takeaways executives need to act on

- Optimize product portfolios for clarity and margin: Given incremental growth, brands that sharpen their core SKUs (backpacks, totes and hybrid formats) and eliminate low‑velocity variants will improve working capital and SKU economics.

- Channel and experience differentiation: Digital D2C, strategic partnerships with specialty baby retailers, and experiential touchpoints remain the most effective levers to convert new parents into repeat buyers. Pricing and promotion cadence must be tailored by channel to avoid margin erosion.

- Sustainability as competitive hygiene: Extended Producer Responsibility (EPR) laws and high‑visibility regulation in several U.S. states require immediate attention. Companies that proactively reengineer packaging and takeback pathways will unlock both compliance and brand equity benefits.

- Supply chain resiliency is a bottom‑line imperative: Recent commodity movements and regional manufacturing dynamics demand a reassessment of sourcing strategies and contingency inventories.

What’s in the full report — practical, field‑tested intelligence

- Concise market sizing and trend maps across 2020–2025 with a transparent forecast methodology for 2026–2032, enabling scenario stress tests for planning and M&A diligence.

- Channel and go‑to‑market playbooks that translate consumer microsegments into merchandising rules, promotional calendars, and retail partnerships.

- SKU and portfolio optimization templates: guided frameworks for SKU rationalization, launch sequencing, and margin uplift through material and design choices.

- Supply chain playbook: supplier scorecards, cost‑to‑serve benchmarks, and alternate sourcing pathways aligned with tariff and freight volatility scenarios.

- Regulatory readiness checklists for EPR and state packaging mandates, including cost modeling templates and supplier engagement scripts.

- Competitive benchmarking and M&A screening tools: a confidential database of leading brands, OEMs and factories, with practical acquisition prioritization criteria.

Note: this release highlights high‑level findings. The full report contains granular regional and application breakdowns, SKU‑level pricing matrices, and detailed company profiles useful for due diligence and GTM planning — data intentionally reserved for subscribers to preserve competitive advantage.

Diaper Bags Market

Competitive landscape: who is shaping the market and why it matters

The diaper bags market is marked by a mix of branded consumer players and large OEMs. Market concentration is moderate; the top three and top five firms control meaningful shares of industry revenue, which reflects an environment where national brands coexist with specialized niche designers and sizable contract manufacturers in Asia.

Diaper Bags Market

- Established consumer brands: U.S.-based legacy and specialty brands are driving much of the product innovation and brand loyalty dynamics. These players excel at retail distribution, seasonal collaborations, and lifestyle positioning that resonates with new parents seeking both function and style.

- Design‑led challengers: A cohort of upmarket and design-forward entrants has expanded consumer expectations on materials, modularity, and cross‑use styling. Their ability to command premium pricing hinges on demonstrable utility and aspirational branding.

- OEM and contract manufacturers: China‑based factories and global wholesalers enable rapid scaling and competitive pricing for private label and high‑volume SKUs. Their role is central to margin management, lead time control and product customization capability.

- Retail and channel partners: Big‑box retailers and specialist baby stores remain important distribution anchors, while direct-to-consumer channels continue to accelerate customer insights, repeatability, and margin expansion.

Recent industry activity — such as the product showcases at the ABC Kids Expo in May 2026 — demonstrates active innovation pipelines across both heritage and emerging brands. Trade events continue to be an important bellwether for new materials, multifunction designs, and accessory ecosystems that extend lifetime customer value.

Supply‑side dynamics: raw materials and manufacturing risks

- Commodities pressure: In 1Q 2026, HDPE and LDPE prices saw notable increases driven by demand and supply tightness. Conversely, certain paperboard inputs displayed relative stability. These disparate movements favor product designs that can substitute materials without compromising perceived quality.

- Pulp and fiber indices: Broader pulp price indicators have risen versus historical baselines, raising out‑of‑shelf costs for paper‑based packaging and some composite materials used in accessories and inserts.

- Manufacturing concentration: High‑volume OEM capacity remains concentrated in parts of Asia, which supports cost competitiveness but leaves buyers exposed to lead‑time and freight variability. Diversifying supplier tiers and near‑shoring selective SKUs are practical hedges.

Regulatory and sustainability drivers to watch

- Extended Producer Responsibility (EPR): Several U.S. states have implemented comprehensive EPR packaging laws with staggered effective dates through 2025 and beyond. California’s packaging EPR framework achieved a regulatory milestone in mid‑2026, signaling enforcement readiness. Brands should model compliance costs and explore producer consortium participation.

- Materials innovation: Consumer and regulatory pressure is accelerating adoption of recyclable and lower‑impact materials. Firms that integrate circularity into product design — for example, easy‑to‑separate components and recyclable outer shells — can reduce long‑term compliance exposure and appeal to sustainability‑oriented consumers.

Recommended 90‑day and 12‑month priorities for 2026 planning cycles

- 90‑day sprint: Conduct SKU economics triage (identify lowest contributors to revenue and margin), lock in raw material contracts for near‑term stability, and establish an EPR impact model for current packaging formats.

- 6–12 month initiatives: Roll out a prioritized SKU rationalization plan, pilot near‑shore production for key premium SKUs, and operationalize a packaging redesign roadmap aligned with upcoming EPR compliance windows.

- M&A and partnerships: Use the report’s target screening framework to prioritize acquisitions that add differentiated product technology, design IP, or in‑region manufacturing capacity. Consider strategic alliances with material innovators to secure early access to recyclable composites.

How PW Consulting’s intelligence accelerates your 2026 outcomes

Our Diaper Bags Market report combines market rigor with operational pragmatism: robust topline projections (base year 2025), a transparent 2026–2032 forecast, concentration analysis, supplier mapping, and trade‑show surveillance. The result is a decision‑ready playbook that reduces the time between insight and action — from strategic planning sessions to board‑level investment decisions.

For procurement, product, channel and M&A teams preparing 2026 budgets, the report delivers the quantifiable context and executable guidance required to prioritize initiatives, defend margin, and capture growth in a measured, risk‑adjusted way. To access the full datasets, regional and application detail, and company benchmarking tools referenced above, please consult the report landing page where subscribers can download the complete analysis and supporting appendices.

For detailed analysis of this topic, please visit the official page: Diaper Bags Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.