PW Consulting Forecast: Battery Design & Manufacturing Software Market to Soar at 16.62% CAGR, Reaching USD 8.64 Billion by 2032

Battery Design And Manufacturing Software Market: A Strategic Playbook for 2026 Decision‑Makers

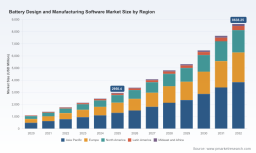

PW Consulting’s new market research briefing on the Battery Design And Manufacturing Software Market provides a practical, decision‑grade roadmap for executives planning technology, sourcing, and compliance strategies in 2026. Anchored on a 2025 base year and a rigorous historical series (2020–2025), the report shows the sector scaling rapidly — from a market of USD 1,102.5 Million in 2020 to USD 2,950.4 Million in 2025 — and projecting to USD 8,638.25 Million by 2032 at a compound annual growth rate (CAGR) of 16.62%. These headline dynamics are the backdrop against which near‑term strategic choices will determine competitive positioning, regulatory compliance, and margin capture.

Battery Design And Manufacturing Software Market

Why this briefing matters for 2026

-

Regulatory inflection points are happening now: major reporting and data‑registration requirements come into force in 2026 across critical markets, and buyer incentives are being conditioned by localization and origin rules. Software investments are no longer optional for manufacturers who need to demonstrate traceability, chemistry disclosure, and carbon accounting.

Battery Design And Manufacturing Software Market -

Technology consolidation and capability expansion among leading vendors are reshaping the vendor selection landscape. Recent M&A, product releases with AI enhancements, and a broadened scope of digital twin and MES offerings are changing how teams evaluate total cost of ownership and integration risk.

Battery Design And Manufacturing Software Market -

Fast‑moving engineering needs — from cell chemistries to pack assembly and BMS validation — mean that simulation, digital twin, and production execution tools are now central to time‑to‑market and safety outcomes, not peripheral R&D expenses.

What the PW Consulting report delivers (practical, execution‑focused)

-

Actionable market sizing and growth scenarios: a transparent methodology that reconciles historical vendor and end‑market signals into a 2026–2032 forecast, with sensitivity tiers for adoption velocity, regulatory tightening, and capital availability.

-

Vendor landscape and selection framework: a modular RFP checklist and scoring matrix that evaluates simulation, PLM, MES, quality & testing control, and BMS toolsets across integration, data model openness, AI readiness, validation toolchains, and field support.

-

Implementation playbooks: step‑by‑step roadmaps and KPI templates for pilot→scale deployments (6–24 month horizons), including data governance model, systems integration patterns, and change‑management milestones.

-

Compliance and reporting toolkit: an audit checklist aligned to emerging EU and US rules, ISO safety alignment requirements for BMS, and practical templates for traceability and chemical/performance reporting.

-

Commercial decision tools: TCO and ROI models, vendor lock‑in risk calculators, and scenario cost curves that translate software choices into cycle time, rework, scrap reduction, and compliance cost impacts.

-

Risk & scenario analyses: three distinct strategic scenarios that stress test product roadmaps, capital allocation, and supplier strategies under alternate regulatory and demand outcomes.

Market structure and competitive dynamics

The market is moving toward a concentrated but still contestable structure: the top three vendors capture a meaningful portion of commercial software revenues while the top five extend that reach materially. That concentration creates both opportunity and risk — enterprises can rely on established platforms for breadth of capability, but must manage vendor dependency, integration complexity, and upgrade roadmaps carefully.

-

Ansys — widely adopted for multiphysics battery modeling, thermal management, electrochemistry simulation, and BMS development; valued for speed in validation cycles and reducing physical testing burden.

-

Siemens — offers an integrated design‑to‑manufacturing portfolio including battery design and digital manufacturing tools; recent strategic expansion into complementary simulation and AI capabilities has broadened its proposition.

-

Altair Engineering — known for system and multiphysics simulation and advanced AI modeling; recent product advances and integration activity have improved automation and safety analysis workflows.

-

COMSOL — brings flexible multiscale electrochemical and thermal modeling modules that are frequently used in materials and early cell design stages.

-

MathWorks — favors model‑based system development and virtual testing, embedding battery system simulation into broader vehicle/industrial controls workflows.

-

Dassault Systèmes — leverages platform strengths in materials science, virtual twin, and lifecycle management for end‑to‑end battery cell and pack optimization.

-

GE Vernova — focuses on MES for production traceability and yield optimization in battery manufacturing lines.

-

AVL — provides simulation and lab management solutions supporting test automation, BMS development, and virtual twin validation at cell, module and pack levels.

Recent market developments underscore the pace of change: notable product releases that embed AI workflows, major strategic acquisitions that combine simulation and high‑performance computing assets, and industry summits that signal an accelerating practitioner community around battery manufacturing and simulation best practices.

Key regulatory and technology forces shaping vendor and buyer strategies

-

Regulatory reporting mandates and data‑format standards are now binding in key jurisdictions, forcing engineering and IT teams to embed reporting workflows into design and production systems rather than treat them as an afterthought.

-

Content thresholds tied to incentive programs introduce supply chain compliance as a software problem: systems must track material provenance and support verifiable reporting across suppliers.

-

Functional safety standards require BMS development and validation approaches that are tightly integrated with simulation and virtual testing platforms — pushing organizations toward toolchains that can demonstrate traceable verification artifacts.

-

AI and digital twin adoption is accelerating — not as a speculative capability, but as a pragmatic way to automate parameterization, speed up virtual test coverage, and compute lifecycle carbon footprints at scale.

Strategic recommendations for 2026

-

Prioritize integration‑first selections: prefer vendors and partners that expose open data models and provide proven connectors into PLM, ERP, and MES to ensure compliance reporting and traceability needs are met without costly bespoke work.

-

Invest in a phased digital twin program: begin with cell and thermal models to de‑risk designs, then extend to module, pack, and factory twins to capture production quality and yield gains.

-

Embed compliance and provenance workflows into procurement and production systems now — delayed remediation is far costlier than acquiring the right data model and governance around supplier material declarations.

-

Use TCO and scenario tools to stress test vendor lock‑in and upgrade paths against market concentration; ensure contractual flexibility for key algorithmic components (e.g., IP for cell models) where possible.

-

Build internal AI and modeling capability alongside vendor partnerships to retain control over the highest‑value IP (chemistry models, safety cases) while outsourcing commodity simulation and execution services.

Scenario planning: three practical paths to 2028

-

Measured scaling — steady EV and storage deployment with predictable regulation: phased investments in simulation and MES yield steady ROI and limited vendor churn.

-

Regulatory acceleration — rapid tightening of reporting and origin rules: prioritize traceability systems and in‑house data capabilities; accelerate digital twin rollout to meet compliance and reduce certification cycles.

-

Geopolitical fragmentation — localized incentives and trade barriers: emphasize flexible, interoperable architectures and multisource vendor strategies to avoid single‑country or single‑supplier exposure.

How PW Consulting supports execution

Our advisory offering converts this report’s insights into operational outcomes. Services include vendor selection and procurement support, systems integration oversight, regulatory compliance audits, ROI and TCO modeling customized to your product and supply chain, and M&A due diligence around software and digital twin capabilities. We also deliver bespoke training programs for engineering, manufacturing, and compliance teams to operationalize digital twin and AI workflows.

PW Consulting’s Battery Design And Manufacturing Software Market report is structured to be immediately usable by CIOs, heads of engineering, supply chain leads, and corporate strategists weighing software investments in 2026. The full report contains the underlying data tables, vendor scorecards, technical integration patterns, and downloadable TCO/ROI models that executive teams use to align investment, procurement, and compliance timelines.

Next steps

For companies preparing capital and technology plans in 2026, this report provides the evidence base and pragmatic playbooks to prioritize investments and de‑risk execution. To access the complete dataset, vendor scorecards, and the downloadable implementation toolkits referenced here, please visit the PW Consulting report landing page and request the full report package and executive briefing session.

For detailed analysis of this topic, please visit the official page: Battery Design And Manufacturing Software Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.