PW Consulting: Construction Site Dumper Market Set to Grow at a 5.85% CAGR Through 2032, Driving Major Regional and Product Shifts

PW Consulting Releases Strategic Brief: Construction Site Dumper Market Outlook and Tactical Playbook for 2026 Decision-Making

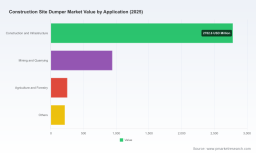

PW Consulting today publishes a forward-looking industry briefing tied to its comprehensive Construction Site Dumper Market Report (base year 2025, forecast 2026–2032). The analysis synthesizes macro sizing, competitive dynamics, supply‑chain stressors and commercial playbooks that senior executives, procurement leads and private‑equity investors must act on in 2026. Drawing on novel data modelling and primary interviews across OEMs, rental houses and fleet owners, the report shows the market moving from an estimated USD 4.185 billion in 2025 toward roughly USD 6.244 billion by 2032—a compound annual growth rate of 5.85% across the forecast period. This release highlights the strategic value of those insights while preserving the report’s proprietary segment-level data to encourage direct engagement with PW Consulting for deeper validation and execution support.

Construction Site Dumper Market

Why this matters for 2026 planning

-

Timing: 2026 sits at an inflection where demand recovery, product electrification and rising input-cost volatility converge—forcing capital allocation and sourcing decisions that will determine 2026–2028 margin trajectories.

Construction Site Dumper Market -

Resource allocation: Manufacturers and large fleet operators face trade-offs between capacity expansion, electrification investment and price competitiveness. The briefing translates market growth projections into prioritised actions to optimise ROI under different scenarios.

Construction Site Dumper Market -

Deal cadence: M&A and JV opportunities that look attractive under 2025 assumptions can change materially once raw‑material dynamics and tariff regimes are baked in. PW’s scenario modelling equips deal teams to set realistic valuation bands and earn‑out triggers.

Market trajectory at a glance

The dumper market is on a steady growth path driven by continued construction activity, infrastructure spend in select markets, and replacement cycles across private and rental fleets. PW’s top‑line forecast—from the 2025 baseline—projects consistent growth to 2032, with a mid‑single‑digit CAGR (5.85%) in the forecast window. Importantly, growth is not uniform: pockets of accelerated adoption exist (e.g., low‑emission zones, urban infill projects), while cost pressures and regulatory shifts create local demand distortions.

Key market dynamics shaping 2026 decisions

-

Input‑price volatility: Between 2024 and 2026, steel and aluminium price swings materially affected manufacturing margins; mid‑sized dumper pricing rose by roughly 4% in early 2026 as OEMs passed through part of the cost increase. At the same time, the US Producer Price Index for construction materials and services rose about 3.3% year‑on‑year, driven by steel, aluminium and copper—creating a persistent upward pressure on bill of materials.

-

Trade and tariff risk: Ongoing US tariffs on steel and aluminium imports (around 25% in many cases) add a structural cost burden for globally sourced assemblies and make near‑sourcing and material hedging viable strategic responses.

-

Electrification and product innovation: OEM roadmaps show parallel investments in electric drivetrains, rotator/dual‑view controls and operator safety systems. This bifurcation—higher‑margin, technology‑rich models vs. low‑cost utility units—will shape product roadmaps and dealer inventories in 2026.

-

Concentration and channel dynamics: The market exhibits moderate concentration at the top—our concentration metrics indicate the top three firms account for a significant share of industry revenue, and the top five increase that concentration further—creating both competitive pressures and partnership opportunities for mid‑tier players.

Competitive landscape: players to watch

Our competitive scan combines public disclosures, primary interviews and product mapping to profile the strategic postures of the leading OEMs. Below are the core incumbents whose moves will materially influence 2026 outcomes.

-

Thwaites Limited (Leamington Spa, UK) — a family‑owned specialist with a deep product line spanning small to large site dumpers. Thwaites has leaned into capacity and electrification: a late‑2025 factory expansion added production flexibility, and new product previews at Bauma 2025 signalled a push into both rotator and electric segments. Strategic implication: Thwaites is enhancing throughput while broadening its product mix—competitors should anticipate increased volume competition on mid‑tonnage units.

-

Wacker Neuson (Munich, Germany) — positions itself on visibility, operator ergonomics and performance across wheel, track and dual‑view platforms. The February 2025 launch of a 12.5‑tonne Dual View model underscores a move up‑market in payload while doubling down on site productivity features. Strategic implication: expect margin pressure for feature‑rich rental specifications and an intensifying competition for larger on‑site units.

-

JCB (Rocester, UK) — leverages strong brand and dealer networks, with early electrification efforts in small‑tonnage site dumpers and a focus on safety systems. JCB’s integrated sales and service model makes it a formidable partner for rental fleets seeking lifecycle cost certainty. Strategic implication: partnerships with global rental players are a key battleground.

-

Mecalac (Annecy‑le‑Vieux, France) — concentrates on compact, urban‑optimised offerings with swivel and front‑tip configurations. Its portfolio aligns well with the growing need for machines in confined and inner‑city jobsites. Strategic implication: urbanisation trends favor compact product specialists for municipal and dense construction projects.

-

Bergmann Maschinenbau (Meppen, Germany) — focuses on tracked and wheeled compact dumpers with electric variants, often addressing niche site needs such as tunnels and mines. Strategic implication: niche manufacturers can capture premium pricing in specialised applications where regulatory or access constraints limit options.

-

Caterpillar Inc. (Irving, Texas, USA) — brings scale in articulated dump trucks and higher‑payload site solutions. Caterpillar’s systems approach emphasizes productivity and telematics for larger projects. Strategic implication: large contractors and mining operators will continue to favour consolidated suppliers that integrate machines with fleet analytics and financing.

Recent industry moves and what they signal

-

Factory expansions and product launches in 2025–2026 reflect a defensive capacity build plus targeted up‑skilling toward electric and rotator variants. Expect near‑term increases in production flexibility rather than capacity for volume growth alone.

-

OEMs are selectively premiumising offerings—adding operator safety, visibility and telematics—to protect margins. Rental‑led spec demands will accelerate the uptake of telematics and maintenance contracts.

-

Material cost pass‑throughs and tariff exposure are driving procurement teams to diversify suppliers, consider near‑sourcing and invest in forward material contracts; these are practical levers for margin protection in 2026.

Strategic imperatives for 2026 (actions by capability)

-

For OEM executives: Prioritise modular platforms that allow quick product swaps between electric, diesel and hybrid drivetrains. Use capacity flexibility—rather than blanket expansions—to respond to regional demand swings and raw‑material shocks.

-

For supply‑chain leaders: Implement a two‑track sourcing strategy: secure long‑term agreements for critical alloys and fast‑cycle suppliers for commoditised components. Deploy dynamic hedging for metal inputs and build tariff‑aware BOMs to quantify landed cost impacts.

-

For sales and channel heads: Reconfigure dealer economics to favour service and telematics subscriptions; rental houses will increasingly value TCO clarity over purchase price. Design bundled offerings with maintenance and uptime guarantees to capture recurring revenue.

-

For investors and M&A teams: Focus on targets that bring complementary technology (electric drivetrains, telematics), regional dealer access, or niche product portfolios that command premium pricing in constrained environments.

-

For fleet owners and contractors: Reassess replacement cycles to balance immediate cost pressures against long‑term fuel savings and regulatory compliance advantages from electrified units. Negotiate lifecycle contracts that shift operational risk back to OEMs or lessors.

What PW Consulting’s full report delivers (practical, executable items)

-

Top‑down market sizing with transparent modelling assumptions, and bottom‑up checks to validate the forecast trajectory to 2032.

-

Scenario analyses that quantify P&L and free‑cash‑flow impacts under alternative raw‑material price paths, tariff regimes and electrification adoption rates.

-

Competitive scorecards, capability maps and dealer network heatmaps to prioritise markets and channels for expansion (proprietary segment‑level data is reserved for report subscribers).

-

Supplier risk matrices and recommended contractual language for material hedging, duty mitigation and dual‑sourcing playbooks.

-

An M&A playbook including valuation frameworks, synergy checklists, and integration risks specific to dumper platforms and after‑sales services.

-

Practical templates: procurement RFx checklists, fleet transition roadmaps, telematics ROI models and sample service‑contract SLAs.

How to use this briefing in 2026

Use the briefing to set the agenda for board discussions, revise capital expenditure priorities, and renegotiate supplier contracts. The material helps identify where short‑term defensive moves (material hedges, inventory buffers) should give way to long‑term strategic shifts (platform modularisation, electrification partnerships, and subscription‑based aftermarket offerings).

Conclusion & next steps

The coming 12–18 months will disproportionately reward organisations that combine disciplined supply‑chain execution with selective technology and channel plays. PW Consulting’s Construction Site Dumper Market Report provides the analytically robust foundation to make those calls with confidence. This release highlights the actionable implications for 2026 while reserving the full, granular segment datasets and scenario outputs for the complete report.

For access to the full report, interactive dashboards and bespoke advisory engagements, contact PW Consulting or visit our report landing page to request a sample executive deck and schedule a briefing with one of our industry specialists.

For detailed analysis of this topic, please visit the official page: Construction Site Dumper Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.