PW Consulting: Tubular Cable Lugs Market to Expand from USD 432.5 Million in 2025 to USD 706.0 Million by 2032 at a 7.25% CAGR

Tubular Cable Lugs Market — Strategic Preview for 2026 Decision-Making

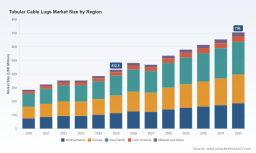

PW Consulting today publishes a strategic preview of our comprehensive Tubular Cable Lugs Market Report (base year 2025, forecast 2026–2032). As global electrification and industrial modernization accelerate, tubular cable lugs — the humble but mission-critical link in power and control cabling — are moving from a commoditized component to a focal point of supply-chain and product strategy. Our analysis shows that the global market expanded materially over 2020–2025 and is projected to continue growing at a compound annual growth rate (CAGR) of 7.25% through 2032. The market grew from a multi-hundred-million-dollar base in 2020 to an estimated USD 432.5 million in 2025, and, under the central forecast, is expected to approach roughly USD 706 million by 2032.

Tubular Cable Lugs Market

What this preview delivers for 2026 planning

-

Actionable foresight to inform procurement and purchasing commitments as raw-material volatility intensifies.

Tubular Cable Lugs Market -

Supply-side and demand-side scenario thinking to prioritize investment and capacity moves in 2026.

Tubular Cable Lugs Market -

Competitive maps and strategic imperatives for manufacturers, distributors, and major end-users to sharpen go-to-market and risk-mitigation choices.

Macro trajectory and near-term inflection points

The tubular cable lugs market’s trajectory is constructive but non-linear. Our historical reconstruction shows meaningful expansion between 2020 and 2025, reflecting infrastructure spending, replacement cycles in utilities and industry, and incremental demand from automotive and renewable-energy integration. The central forecast embeds a 7.25% CAGR for 2026–2032, but year-to-year variation is expected — reflecting the interplay of raw material price shocks, inventory cycles, and demand seasonality.

Notably, our scenario runs highlight a short-term correction risk in 2026–2027 driven by a combination of elevated copper prices and the timing of project starts. Early 2026 saw copper trading at unusually high levels (reported around USD 12,000–14,500 per tonne), directly pressuring manufacturers’ cost structures and prompting a transient margin squeeze for producers with limited hedging or pass-through capability. This kind of upstream shock explains why the model anticipates a temporary plateau or dip in some near-term vintages of demand before the mid-cycle recovery resumes.

Key dynamics shaping 2026 choices

-

Raw material volatility: Copper and aluminum price swings have immediate P&L and working-capital consequences. Manufacturers that combine disciplined hedging, cost-efficient production footprints, and alternative alloy strategies will preserve margin and protect delivery performance.

-

Standards and compliance: Compression and tubular lug designs are governed by established dimensional and performance standards (for example, DIN 46235 for compression connections). Compliance is table stakes for access to utility, industrial, and OEM channels — and an area where documentation, testing, and traceability can be monetized as a premium service.

-

Concentration and competitive dynamics: The market shows moderate consolidation. Our concentration metrics indicate a mid-level CR3 and CR5 presence that leave room for regional champions and specialized players to capture niches through quality, service speed, and certification.

-

End-market evolution: Electrification in transportation, grid modernization, and industrial automation continue to push technical requirements — finer stranded conductors, higher-current ratings, and more demanding environmental performance — creating an opening for differentiated product architectures and value-added services (pre-assembly, testing, certs).

Competitive landscape — what matters for procurement and partnership strategy

Our competitive review emphasizes a mix of global specialists and regional manufacturers. A non-exhaustive selection of influential players helps illustrate strategic archetypes:

-

Klauke (Germany) — positioned as a high-quality specialist with product depth in electrolytic copper tubular lugs and DIN-compliant solutions for fine and superfine stranded conductors. Recent product updates (e.g., updated two-hole lug designs rolled out mid‑2025) signal continued investment in fit-and-performance features aimed at professional installers and OEMs.

-

Pioneer Power International (India) — a volume-oriented producer offering copper and aluminum tubular lugs, heavy-duty XLPE-compatible types, and compression terminals. The profile exemplifies India-based manufacturers’ dual role as domestic suppliers and export-oriented OEMs.

-

MG Electrica (India) — an ISO-certified player with broad product listings; catalog and price-list refreshes through 2025 illustrate sustained production and active market servicing.

-

Axis Electricals (India) — UL-listed capability with emphasis on high-conductivity ETP copper parts; a strategic example of combining certification and material-grade messaging to access rigorous end markets.

-

Yueqing Lilian Electric (China) and Apple International (India) — exporters and manufacturers that compete on breadth, availability, and price, particularly for commodity-grade tubular lugs and battery cable ends.

For 2026 planning, buyer-side players should weigh supplier selection through a multi-dimensional lens that includes: certification status, traceability and labeling practices, lead-time reliability, pricing-model flexibility in a volatile raw-material environment, and willingness to partner on product qualification exercises. On the sell side, manufacturers should consider targeted moves: premiumization through certified ranges, channel segmentation (value vs. spec-driven channels), and selective backward integration or strategic hedging of raw material supply.

What the full PW Consulting report contains (executive-operational toolkit)

-

Market sizing and validated demand history (2020–2025) and forward-looking scenarios 2026–2032, including sensitivity tables for raw-material price regimes.

-

Probability-weighted forecasts and three stress-case scenarios designed for procurement, commercial planning, and M&A diligence.

-

Segment-level analysis with product, application and regional lenses — strategic implications and commercialization playbooks. (Note: detailed subsegment tables are intentionally excluded from this preview and are available in the full report.)

-

Supplier benchmarking: capability matrices, certification mapping, lead-time portraits, and service scorecards for the key vendors referenced above.

-

Raw-material impact diagnostics and a price-pass-through model to support contract negotiations and margin-stress testing.

-

Regulatory and standards appendix (including requirements that reflect DIN 46235 and comparable norms) and a practical checklist for compliance-led product entry.

-

M&A and partnership playbook highlighting bolt-on targets, value-creation levers, and integration risks in mid-market transactions.

Strategic recommendations for corporate and procurement leaders in 2026

-

Hedge and tier raw-material exposure: Use a combination of short-term hedges and strategic supplier agreements with price-reset clauses tied to commodity indices. For buyers, consider multi-year framework agreements that trade a modest premium for price stability and guaranteed allocation.

-

Prioritize certification and traceability: Utilities and OEMs increasingly demand documented compliance. Investing in certified ranges and batch-level traceability reduces time-to-contract and defensibly supports premium pricing.

-

Flex manufacturing to blend material mixes: Equip plants to switch between copper, aluminum, and bimetallic production to respond to relative metal-cost eclipses without large retooling lead times.

-

Calibrate inventory with project pipelines: Given the projected CAGR and near-term volatility, adopt a more dynamic safety-stock policy that aligns with confirmed project schedules rather than static days-of-cover rules.

-

Pursue selective premiumization: Differentiate on design (e.g., enlarged internal geometries to support fine-stranded conductors), testing, and after-sales services where the market tolerates a value premium.

How to use this preview — and where to get the full data

This preview is intentionally focused on strategic signals and operational implications for 2026. It demonstrates the depth of our methodology — combining primary interviews, supplier audits, price-series analysis, and standards crosswalks — while withholding exhaustive subsegment tables and company-level revenue estimates to preserve the report’s actionable value for subscribers.

For procurement leaders, product managers, investors, and M&A teams planning in 2026: the full PW Consulting Tubular Cable Lugs Market Report provides the granular datasets, supplier scorecards, contract-play templates, and scenario models necessary for confident, defensible decisions. Contact PW Consulting to request the full report, obtain an executive briefing, or commission a tailored variant of our forecast and supplier-benchmark workstreams.

Closing perspective

As the industry moves through the 2026 planning horizon, the principal strategic tension will be between commoditization pressure and the opportunity to capture margin through compliance, service, and product fit. Market expansion at a mid-single-digit CAGR masks meaningful tactical complexity — and that complexity is where advantage is won. PW Consulting’s report equips executives with the analytic scaffolding to convert market growth into differentiated commercial outcomes while managing the raw-material and regulatory shocks that will define the next 18–24 months.

For detailed analysis of this topic, please visit the official page: Tubular Cable Lugs Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.