PW Consulting: Digital Ureteroscopes Market Poised for 6.5% CAGR During 2026–2032, Signaling Strong Global Growth

Digital Ureteroscopes Market 2026: Strategic Imperatives for Clinical, Commercial and Manufacturing Leaders

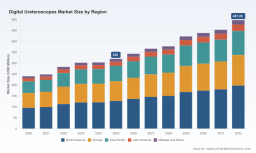

PW Consulting’s latest market study on Digital Ureteroscopes synthesizes five years of historical performance (2020–2025) and provides a seven-year outlook (2026–2032) to equip executive teams with the evidence and scenario-based counsel required to make high-consequence decisions in 2026. The market is on a steady growth trajectory with a compound annual growth rate (CAGR) of 6.5% across the forecast window. Our model places the market size at USD 320.0 Million in the base year (2025), with the industry expected to exceed USD 497 Million by 2032 under a central-case projection.

Digital Ureteroscopes Market

Why this study matters for 2026 planning

- Hospitals, ambulatory surgery centers (ASCs), device OEMs and investors face a convergent set of clinical, economic and regulatory pressures that will reshape procurement and product roadmaps in 2026. This report isolates actionable levers—pricing architecture, infection-control economics, imaging differentiation, and capital allocation—that meaningfully alter ROI timelines.

- Consolidation of purchasing power and evolving reimbursement pathways make 2026 a pivotal year for negotiating commercial terms. Our concentration analysis finds a top-three market share cluster that commands substantial influence over pricing and channel dynamics (CR3 ~65%; CR5 ~85%).

- Technology choice—single‑use versus reusable digital platforms—no longer rests solely on clinical preference. It is now an integrated financial, operational and regulatory decision. The report quantifies the break-even and risk thresholds under multiple throughput and utilization scenarios to guide deployment strategies.

Market outlook — what the numbers say (high-level)

Aggregate demand for digital ureteroscopes has expanded steadily over the past half-decade, driven by rising procedure volumes, higher adoption of advanced visualization, and increasing penetration of single‑use solutions in key care settings. The combination of moderate CAGR and robust long‑term growth underpins a market that is both attractive for new entrants focused on niche differentiation and strategically important for established medtech platforms that can defend scale economics and service capabilities.

Digital Ureteroscopes Market

While this summary intentionally omits granular breakdowns by region, product subtype and procedure mix (those granular splits are preserved in the full report to protect the integrity of proprietary analysis), executives should note that growth is multifactorial—rooted in procedural demand, shifting site-of-care economics, and regulatory movements that affect device lifecycle costs.

Digital Ureteroscopes Market

Dynamics shaping the competitive battleground

- Regulatory posture: Digital flexible ureteroscopes remain Class II devices in the U.S., requiring 510(k) clearances. Regulatory pathways continue to favor well-documented, incremental innovations (e.g., imaging sensors, pressure telemetry) that demonstrate performance parity or improvement against recognized predicates.

- Reimbursement and site-of-care economics: Established CPT codes and payment structures support both single‑use and reusable strategies, but the capture of incremental reimbursement—particularly when novel device features lower complication rates or enable quicker case turnover—will be a differentiator.

- Infection control and total cost of ownership: Single‑use platforms address cross‑contamination risk and eliminate reprocessing and repair costs; yet, their value proposition must be balanced against per-case device cost and supply-chain resilience. Reusable platforms, meanwhile, rely increasingly on service, repair networks and accessory ecosystems to sustain competitive margins.

- Technology and clinical differentiation: Advances such as real-time intrarenal pressure monitoring, ARC imaging and higher-resolution CMOS sensors are shaping purchasing criteria. Vendors that can couple clinical outcomes data with operational benefits will displace feature-only competitors.

Competitive landscape — strategic positions and implications

The market is composed of a mix of established global endoscopy leaders, innovative device specialists and new entrants focused on single‑use offerings. Key players profiled in our analysis include Boston Scientific, KARL STORZ, Olympus, Dornier MedTech, Ambu, OTU Medical, Richard Wolf and Stryker. Each brings a distinct go-to-market axis:

- Boston Scientific: Leveraging product extensions of its single‑use LithoVue Elite platform—now with additional configurations and intrarenal pressure monitoring capabilities—Boston Scientific is optimizing for clinical evidence that links device telemetry to procedural safety and efficiency. Their regulatory pathway history and reimbursement resources create a playbook for rapid scale-up in hospital systems.

- KARL STORZ: With high-resolution reusable platforms, KARL STORZ competes on imaging fidelity and service longevity. Their strategy centers on supplying durable reusable systems to high-volume centers that prioritize lifecycle cost control and imaging performance.

- Olympus: Emphasizing durability and image quality in flexible ureteroscopy, Olympus aims to defend installed base relationships and capture upgrade cycles in tertiary centers where procedure complexity and equipment utilization are high.

- Dornier MedTech & Ambu: Both have purpose-built single‑use offerings and recent commercial launches targeting the U.S. market. Their value propositions hinge on slim distal-tip profiles and simplified logistics—appealing to ASCs and hospital buyers prioritizing infection control and predictable per-case costing.

- OTU Medical, Richard Wolf and Stryker: These firms compete across niches—WiScope and Cobra/Boa platforms aim to deliver varied deflection and visualization packages, while players like Stryker bundle ureteroscopes into broader endoscopy portfolios to cross-sell into existing customer relationships.

Recent product launches and regulatory clearances (notably new single‑use introductions and additional 510(k) configurations) signal accelerating innovation velocity. The market is tilting toward a hybrid future where single‑use and reusable offerings coexist, and competitive success will depend on integrated solutions that include consumables, service contracts and digital health-enabled features.

What the full PW Consulting report delivers

- Methodology and rigor: Transparent forecasting model (2026–2032), sensitivity analysis, and a bottom-up construction rooted in procedure volumes, site-of-care shifts, device replacement cycles, and published OEM unit economics.

- Tactical playbooks: Go-to-market options for OEMs (direct vs distributor channel mix), procurement negotiation templates for hospital systems, and partnership archetypes (e.g., service alliance, capital leasing, managed service programs) designed for near-term implementation.

- Clinical and economic dossiers: Comparative analyses of single‑use vs reusable lifetime costs across utilization scenarios, plus modeled implications of innovation levers such as intrarenal pressure telemetry and enhanced imaging on procedure throughput and complication rates.

- Competitive matrix and M&A implications: Strategy roadmaps for incumbents and challengers, including inferred valuation multiples from recent transactions and criteria for bolt-on acquisitions to accelerate capability gaps.

- Regulatory and reimbursement intelligence: Up-to-date tracking of 510(k) trends, performance standards, and payer dynamics that influence adoption in hospitals and ASCs.

- Data room: Appendices with historic market sizing (2020–2025), comprehensive vendor profiles, primary interview highlights, and a downloadable scenario model to stress-test executive decisions.

How executives should use these insights in 2026

- CEOs and corporate strategists: Use the market model to prioritize R&D investments—favor features with demonstrable hospital economic impact (e.g., telemetry that reduces readmissions or shortens OR time) over cosmetic improvements.

- Head of Commercial & Partnerships: Re-evaluate channel strategies to capture ASC growth and negotiate value-based contracts that align device pricing with measurable clinical outcomes.

- Supply chain & operations leaders: Stress-test inventory, single-use supply continuity and circular-economy options; diversify suppliers for critical components to mitigate concentration risk from surging single‑use demand.

- Clinical leaders and procurement: Push for pilot programs that collect real-world evidence on per-case cost and infection metrics to inform enterprise-level adoption decisions.

Strategic signposts to watch in 2026

- Adoption velocity of single‑use platforms in ASCs versus high-volume hospital urology units.

- Regulatory decisions clarifying performance requirements for imaging and biocompatibility which will recalibrate entry barriers for new entrants.

- Payer signals linking procedural reimbursement to demonstrable improvements in safety or throughput enabled by device features.

- M&A activity that consolidates service networks or integrates consumable supply chains to lock-in device ecosystems.

Next steps and how to access the full intelligence

This briefing highlights the strategic contours of the Digital Ureteroscopes market and sets out the decision levers that matter most in 2026. For proprietary subsegment data, granular regional and application splits, full vendor scorecards, and the interactive scenario model (which deliberately contain the core numeric detail needed for transaction diligence), please consult the complete PW Consulting report. The full document is structured to serve as an operational playbook—enabling straight-through planning from boardroom strategy to procurement execution.

Contact PW Consulting to request the comprehensive report package, access a briefing with our senior analysts, or commission a custom sensitivity analysis calibrated to your portfolio and geographic exposure. Our team is prepared to run a rapid (2–4 week) engagement to convert these market insights into an executable 2026 roadmap aligned with your financial and clinical KPIs.

For detailed analysis of this topic, please visit the official page: Digital Ureteroscopes Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.