PW Consulting: Hydrocarbon and PTFE High-Speed Digital CCL Market Poised for 9.2% CAGR Through 2032

Hydrocarbon and PTFE Resin High‑Speed Digital Copper Clad Laminate (CCL) Market — Strategic Preview for 2026 Decision‑Makers

Executive snapshot

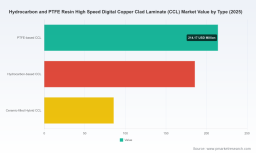

PW Consulting’s latest market study on Hydrocarbon and PTFE Resin High‑Speed Digital Copper Clad Laminates (CCL) provides a concentrated, decision‑grade briefing tailored for executives planning capital allocation, supply‑chain strategy, and product roadmaps in 2026. Anchored on a 2025 base year and a 2026–2032 forecast horizon, the market is expanding at a compound annual growth rate of 9.2%. After rising from the low hundreds of millions in 2020 to roughly USD 485 million in 2025, we project continued acceleration that pushes the market toward approximately USD 900 million by 2032. This trajectory is being shaped by simultaneous demand ramps in data centers, 5G infrastructure, and automotive radar/ADAS, interacting with material supply dynamics and evolving regulatory pressure.

Hydrocarbon and PTFE Resin High-Speed Digital Copper Clad Laminate (CCL) Market

What the report delivers — practical, executable intelligence

- Robust market sizing and a transparent forecasting methodology (historical series 2020–2025; forward view 2026–2032) with scenario modeling to stress‑test CAPEX and procurement decisions.

- Actionable supply‑side analysis: supplier capacity maps, recent expansions, throughput risk scoring, and an up‑to‑date supplier playbook for dual sourcing and qualification prioritization.

- Demand segmentation and adoption curves for PTFE, hydrocarbon and hybrid ceramic systems aligned to end‑market performance requirements (data center, cloud compute, telecom, automotive, aerospace).

- Price‑sensitivity and margin impact modules that translate raw material volatility and pass‑through assumptions into EBITDA stress scenarios for manufacturers and OEMs.

- Regulatory impact assessments (including PFAS/REACH developments) and a compliance roadmap with estimated timelines and cost buckets for design and process remediation.

- Competitive intelligence: detailed profiles and strategic positioning matrices for the leading CCL players, plus M&A and partnership opportunity maps.

- Tactical playbooks for procurement, inventory optimization, qualification acceleration, and technology selection to shorten time‑to‑market while protecting gross margins.

Market dynamics that will shape 2026 decisions

Three converging forces define the near‑term strategic landscape:

Hydrocarbon and PTFE Resin High-Speed Digital Copper Clad Laminate (CCL) Market

- Demand concentration in high‑growth end segments. Higher data rates (112 Gbps and beyond), densification of network infrastructure and ADAS adoption continue to push spec demands upward — prioritizing materials that deliver ultra‑low loss and consistent dielectric behavior at mmWave frequencies.

- Material supply and price volatility. High‑purity PTFE resin supply is concentrated among a small set of global producers, creating potential price swings in the mid‑teens to mid‑twenties percent range during supply stress. PTFE price references in 2025–2026 show material cost differentials across geographies and a structural sensitivity to feedstock availability. Separately, hydrocarbon resin cost pressures have manifested as producer price increases implemented in 2026 due to operating cost and feedstock constraints.

- Rising compliance and regulatory complexity. Proposed restrictions on certain PFAS chemistries (e.g., under EU REACH frameworks) introduce project‑level compliance cost, certification lag and potential formulation change risk for PTFE‑based systems. These dynamics favor firms that can rapidly execute reformulations or qualify alternative low‑loss systems without interrupting customer supply.

Competitive landscape — who’s positioned to win and why

The sector exhibits moderate concentration; the leading three and five suppliers account for a majority share of the market by revenue, creating an environment of advantaged scale for established players while leaving tactical openings for specialized or regional challengers. Key market participants demonstrate differentiated strategies:

Hydrocarbon and PTFE Resin High-Speed Digital Copper Clad Laminate (CCL) Market

- Rogers Corporation (Chandler, Arizona): A technology and application leader with established RO4000 hydrocarbon ceramic laminates and PTFE‑based XtremeSpeed lines. Rogers combines product breadth with manufacturing investments geared to defense and automotive high‑frequency applications.

- AGC Inc. and Taconic (Tokyo / Petersburgh): AGC brings integrated capabilities across hydrocarbon HF‑series and PTFE systems; Taconic augments that portfolio with PTFE specialty laminates focused on RF and high‑speed digital segments. AGC’s vertical integration into resin supply chains is a strategic differentiator.

- Isola Group (Chandler, Arizona): Offers a mix of hydrocarbon and low‑loss laminates targeted to high‑speed digital boards, with emphasis on manufacturability and reliability in high layer‑count PCBs.

- Taiwan Union Technology (TUC) and ITEQ (Taiwan): Regional leaders with strong customer relationships in server, telecom and networking OEMs; they emphasize rapid qualification cycles and localized supply continuity for Asia‑centric demand.

- Shengyi Technology (Dongguan) and Panasonic (Japan): Shengyi has signaled capacity commitment with recent plant investments to meet 5G and data center needs; Panasonic’s MEGTRON line was recently extended with ultra‑low loss materials designed for server networks operating above 112 Gbps.

Recent corporate moves — capacity additions, targeted product launches and geographic expansion — underscore an active competitive arms race to secure long‑term supply and technology leadership. For example, several manufacturers completed or announced capacity projects and new ultra‑low‑loss products in 2025, reflecting how supply and innovation are tightly coupled.

How we translate insight into 2026 strategic actions

Based on our integrated analysis, we prioritize the following actions for different stakeholders. Each recommendation is calibrated to a 12–18 month execution window typical of materials qualification and manufacturing ramp cycles.

- Manufacturers (CCL producers): Fast‑track capability statements and customer co‑development agreements for hybrid and ceramic‑filled solutions to capture clients seeking alternatives to PTFE under regulatory pressure. Hedge near‑term resin exposure via a mix of forward contracts and strategic inventory while negotiating long‑dated offtake terms with major end customers.

- OEMs and system integrators (servers, telecom, automotive): Reassess total cost of ownership (TCO) by including qualification cost, compliance timelines, and yield impacts. Introduce staged qualification windows: prioritize mission‑critical SKUs for the shortest qualification path; defer lower‑priority SKUs to allow for supplier diversification.

- Raw material suppliers and traders: Invest in transparency and traceability programs to help CCL manufacturers and OEMs meet compliance mandates. Consider strategic capacity partnerships or captive agreements to stabilize volumes and lock in margin via value‑added integrated offerings.

- Investors and M&A teams: Focus on targets with niche, hard‑to‑replicate capability (e.g., specialty PTFE compounding, ceramic‑fill processing expertise) and on regional capacity providers that can be consolidated to realize manufacturing synergies and accelerate qualification access to OEMs.

- Procurement leaders: Move from transactional buying to integrated supplier risk management: layer multi‑tier sourcing, institute trigger‑based buy‑ups tied to resin price indices, and secure capacity with clauses for priority allocation during supply shocks.

Practical 2026 roadmap — recommended sequence

- Q1–Q2 2026: Conduct a materials risk audit (resin exposure, qualification backlog, regulatory impact) and create a prioritized supplier shortlist using PW Consulting’s supplier risk scorecard.

- Q2–Q3 2026: Execute dual‑sourcing pilots for critical SKUs; secure conditional capacity commitments and lock pricing collars for immediate needs.

- Q3–Q4 2026: Accelerate product qualification cycles with cross‑functional teams; finalize long‑term commercial agreements where pilot outcomes meet performance and cost gates.

- 2027 and beyond: Reassess portfolio allocations with learnings from pilot programs and start targeted CAPEX or M&A to insource critical capabilities if ROI thresholds are met.

Why this report matters for 2026 decisions

Two reasons make this report particularly timely for 2026 planning cycles. First, market growth at a mid‑single‑digit to high‑single‑digit CAGR compresses time‑to‑revenue for new capacity and pushes suppliers to balance scale with specialization. Second, material and regulatory volatility create asymmetric risks: firms that move early to secure materials, diversify supplier footprints, and qualify resilient material platforms will avoid costly qualification delays and margin erosion later in the cycle.

Next steps — how to convert insight into competitive advantage

PW Consulting’s full study contains the granular segmentation, vendor scorecards, price‑sensitivity models and scenario outputs we intentionally omit here to preserve the value of the full dataset. Subscribers and corporate clients will receive an interactive model, supplier benchmarking sheets, and a step‑by‑step procurement playbook designed to support contract negotiations and capex prioritization in 2026.

To access the complete analysis, datasets, and tailored advisory support — including confidential one‑on‑one briefings and a customized supplier risk simulation for your portfolio — please contact PW Consulting via our corporate channels. Our team will help you translate the market view into a prioritized action plan that aligns with your growth, margin and compliance objectives for 2026 and beyond.

For detailed analysis of this topic, please visit the official page: Hydrocarbon and PTFE Resin High-Speed Digital Copper Clad Laminate (CCL) Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.