PW Consulting: Oat Flakes Market to Expand at 5.2% CAGR (2026–2032), Hitting USD 9,411.4 Million by 2032

Oat Flakes Market 2026 Strategic Outlook — A PW Consulting Preview for Executive Decision‑Making

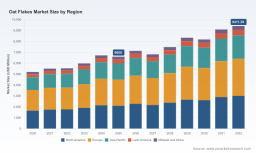

As global food systems rewire for resilience, convenience and nutritional value, oat flakes have moved from a commodity breakfast staple toward a strategic ingredient in food, personal care and ingredient innovation. PW Consulting’s Oat Flakes Market report (base year 2025; forecast period 2026–2032) synthesizes market sizing, supply‑chain dynamics and competitive strategy into a practical playbook for C‑suite, corporate strategy and commercial leaders. The market stood at approximately USD 6.6 billion in 2025 and is projected to expand at a 5.2% CAGR through 2032, reaching the upper‑end of the forecast range by the end of the period. This briefing highlights the report’s strategic value for 2026 planning while deliberately withholding segment‑level datapoints that are available in the full report.

Oat Flakes Market

Why this report matters for 2026 decision cycles

-

Capital allocation and capacity decisions. Supply‑chain restructuring and announced processing investments are compressing the window for high‑impact capital deployment. Our report equips decision makers to decide whether to invest in own capacity, enter tolling partnerships or lock long‑term offtake agreements with strategic suppliers.

Oat Flakes Market -

Product and portfolio strategy. Oat ingredients are being redeployed across formulations — from high‑protein cereals to plant‑based dairy analogues and clean‑label cosmetics. The analysis helps prioritize which formulations to scale in 2026 based on margin, route‑to‑market complexity and consumer willingness to pay.

Oat Flakes Market -

Risk management and procurement. With raw‑material volatility and supply shifts, procurement and risk managers need granular scenarios for pricing, yield and shortage risk. Our modeling provides practicable hedging and contract structures tied to realistic production outlooks.

-

M&A, partnerships and route‑to‑market. As the market remains moderately fragmented (top‑three and top‑five concentration are material but far from monopolistic), there are tactical acquisition and JV opportunities for scale, capability or geographic access. The report maps sensible targets and integration risks.

What’s inside the report — operational deliverables (practical, not theoretical)

-

Market model (2020–2032): an accessible, editable financial model (USD, revenue unit: Million) with base‑case, upside and downside scenarios for revenue, per‑unit pricing and input cost pass‑through dynamics.

-

Scenario playbooks: three prioritized scenarios for 2026–2028 (Base Continuity; Supply Tightening; Premiumization Accelerates) with decision triggers, KPIs and contingency actions tailored to commercial, supply and finance teams.

-

Supplier and capacity map: verified profiles of major millers, co‑packers and new builds accompanied by proximity‑sourcing matrices and operational lead‑time implications for common corridors.

-

Raw material outlook and hedging framework: a short‑term (18‑month) price volatility assessment tied to futures signals and a recommended hedging ladder calibrated for different risk tolerances.

-

Innovation & NPD scoring tool: a go/no‑go matrix for product launch prioritization that balances speed‑to‑market, margin potential and supply resilience.

-

M&A playbook and vendor DD checklist: prioritized value levers, integration risks (capex, quality systems, traceability) and a commercial glide path for synergies.

-

Regulatory and certification implications: impact analysis for organic, purity‑protocol and gluten‑free positioning — and templates for evidence needed to access premium channels.

-

Quality & recall readiness framework: lessons learned and operational controls derived from recent recall events and best practice traceability implementations.

Key market dynamics shaping near‑term strategy

-

Supply expansion and regional shifts. Global oat production has recently increased materially, altering export availability patterns and creating both opportunity and friction points for buyers who require consistent specification and traceability. New processing capacity announced in traditional producing regions — and greenfield mill developments in strategic markets — change the calculus for inventory strategies and localization.

-

Price volatility. Oat futures have shown notable swings in recent months, reflecting weather, logistics and speculative positioning. This volatility amplifies the value of a disciplined procurement strategy that combines forward contracts, index‑linked pricing and selective physical coverage to avoid margin erosion.

-

Quality segmentation and certification demand. Demand for purity‑protocol and gluten‑free oat flakes continues to outpace supply expansion in premium channels, increasing the commercial premium for certified product and raising the operational bar for segregation in milling and packaging systems.

-

Diversifying end uses. Beyond breakfast cereals, oat flakes are gaining share in bakery, plant‑based dairy alternatives, convenience snacks and personal care. This diversification creates cross‑category growth pockets but also requires tighter alignment between buyers and ingredient suppliers on functionality specifications.

-

Margin pressure in North America. Shifting global dynamics have tightened supplies and compressed margins in certain regional corridors—necessitating stronger commercial coordination, yield improvement programs and, for some participants, a reappraisal of sourcing geography.

Competitive landscape — what leading players are signaling

-

Quaker Oats (PepsiCo): The company’s investment in manufacturing capacity in Asia signals an aggressive push to capture faster growth in key emerging markets and to shorten lead times for regional customers. Expect Quaker to prioritize scale, branded innovation and local partnerships as it broadens footprint.

-

Grain Millers Inc.: A major ingredient supplier with diversified format capabilities. Recent product recall activity underscores the continued importance of end‑to‑end food safety systems; procurement and COGS teams should reassess supplier scorecards to incorporate operational resilience criteria.

-

Morning Foods (Mornflake): The company’s premium, sustainability‑led positioning highlights a growing lane for regionally sourced, higher‑margin oats. Retail and private‑label teams should consider small‑batch or co‑branded partnerships to test premium consumer propositions.

-

Avena Foods & Richardson Milling: Both suppliers strengthen options for buyers seeking certified gluten‑free streams and scale capacity in North America. Their capabilities are especially relevant for customers targeting allergy‑friendly and clean‑label applications where traceability is non‑negotiable.

-

Lantmännen: The Nordic processor is at the forefront of functional oat ingredient development (e.g., beta‑glucan isolation, oat protein systems), offering a route for formulators to achieve nutritional claims without sacrificing processing efficiency.

-

Market structure: The market remains moderately fragmented — top‑three and top‑five concentration metrics indicate meaningful but incomplete consolidation — creating an active landscape for bolt‑on acquisitions, strategic alliances and capacity sharing arrangements.

Actionable recommendations for executives planning 2026 moves

-

Lock blended sourcing strategies early. Combine long‑term contracts for core feedstock with shorter, opportunistic purchases tied to futures and physical markets. This hybrid reduces exposure to spikes while keeping flexibility for premium procurement.

-

Invest selectively in segregation and certification lanes. If your strategy targets organic, purity‑protocol or gluten‑free niches, the incremental investment in segregated processing and third‑party certification is typically payback‑positive over a 24–36 month horizon.

-

Prioritize product formulations that tolerate specification variance. Where possible, design recipes that can absorb grade variation without quality degradation; this reduces forced rework and short‑term procurement premiums.

-

Tune M&A filters to capability gaps, not just scale. Targets that offer functional ingredient capabilities, traceability control or regional processing access score higher near‑term than bolt‑on volume plays alone.

-

Strengthen recall and supplier risk playbooks. Recent recall incidents demonstrate the business and reputational costs of lapses. Establish cross‑functional warrooms, redundant supplier mappings and rapid‑response communication templates now.

-

Test premium and co‑branded formats via limited launches. Use regional pilots to validate consumer willingness to pay for sustainability and functionality claims before scaling national rollouts.

Next steps — how organizations should use this preview

This briefing is a strategic trailer designed to orient 2026 planning teams. The full PW Consulting Oat Flakes Market report contains the granular market models, supplier matrices, scenario workbooks and playbooks required to operationalize the recommendations above. Core subsegment figures and the detailed, downloadable data tables are intentionally withheld in this preview to focus on strategic implications; they are available in the complete report package on the PW Consulting website for licensees and subscribers.

For commercial teams preparing budgets, for procurement teams negotiating FY‑2026 contracts, and for strategy teams evaluating M&A options, the report is built to convert insight into a 90‑day action plan. Contact PW Consulting to schedule a briefing and to obtain the report, model files and confidential annexes that support immediate decision‑making.

For detailed analysis of this topic, please visit the official page: Oat Flakes Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.