PW Consulting: Prefabricated & Modular Data Centers to Surge from USD 72.5 Billion in 2025 to USD 210.6 Billion by 2032 at a 16.45% CAGR

Prefabricated And Modular Data Centers Market: Strategic Intelligence for 2026 Decision-Makers

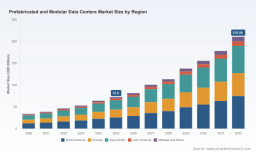

PW Consulting’s latest market study on Prefabricated And Modular Data Centers (base year 2025) is released at a moment when capital allocation, site-selection, and technology choice decisions will determine enterprise competitiveness for the decade ahead. Between 2020 and 2025 the market scaled rapidly — from roughly USD 34.0 Billion to about USD 72.5 Billion — and our forecast extends that momentum through 2032, reaching an estimated USD 210.56 Billion. The forecast window 2026–2032 is underpinned by a compound annual growth rate of 16.45%. For senior executives, infrastructure planners, and investors, this report reframes modular data center purchasing from tactical procurement to strategic capability building.

Prefabricated And Modular Data Centers Market

Why 2026 Is a Strategic Inflection Point

-

Acceleration of AI and high-density compute: The rapid adoption of AI, HPC, and high-density workloads is reshaping requirements for power delivery, cooling (including liquid cooling), and rack-level infrastructure. Modular systems — factory-built, pretested, and optimized for density — are no longer a niche alternative but a primary deployment model for enterprises needing predictable, rapid capacity.

Prefabricated And Modular Data Centers Market -

Regulatory and utility dynamics: 2026 introduces meaningful regulatory shifts in several jurisdictions where data centers are being required to internalize new infrastructure costs and disclose energy impacts. Multi-state actions and formal pledges by hyperscalers to protect ratepayers are changing the economic calculus for siting and operating facilities. Rising residential electricity prices and utility rate cases in recent years further compress margins and require scenario-driven energy planning.

Prefabricated And Modular Data Centers Market -

Supply chain and factory integration become competitive levers: Organizations that lock early to factory-integrated modular solutions gain control over schedule risk, quality, and integration of advanced cooling and power topologies. Recent product launches and collaborations across major vendors demonstrate a race toward factory-delivered AI-ready modules.

What This Report Delivers — Practical, Actionable Intelligence

This is a market intelligence deliverable designed for operators, CIOs, real estate and facilities heads, M&A teams, and infrastructure investors who must translate macro trends into executable choices in 2026. The report combines macro forecasting with practitioner-grade tools and includes:

-

Quantitative market model (2020–2032) with high-resolution scenario layers. The document traces historical growth, baseline forecasts, and up/down scenarios calibrated to demand drivers including AI adoption curves, edge densification, and policy shocks.

-

Vendor profiles and competitive playbooks. Deep, vendor-specific analyses synthesize product roadmaps, factory capabilities, channel models, and go-to-market strategies — enabling readers to build shortlists matched to technical and commercial constraints.

-

TCO and lifecycle toolkits. Modular CAPEX/OPEX templates, sensitivity calculators, and lifecycle replacement scenarios allow procurement teams to compare prefabricated options against traditional stick-built alternatives on equal footing.

-

Site selection and regulatory risk matrices. Practical checklists and scoring models map grid readiness, permitting timelines, taxation and incentives, and local regulatory exposure to support data-driven location decisions.

-

Implementation playbooks. From factory acceptance testing protocols and shipping logistics to on-site commissioning and phased capacity activation, the report outlines standardized processes that reduce schedule risk and integration costs.

-

Supply chain stress-tests and mitigation strategies. Scenarios model critical component constraints, pricing shocks, and vendor concentration, with recommended sourcing and contractual hedges.

Note: To preserve the value of our original research, the full report contains detailed regional and segment-level breakdowns, and downloadable financial models. Core regional/application-level splits and proprietary segment figures are available in the source report.

Competitive Landscape — Who Matters and Why

The modular data center market is moving from fragmented vendor competition to a more structured marketplace where factory integration, systems engineering, and channel execution matter as much as component performance. While concentration is rising, the market remains contestable: the three largest firms account for a significant portion of the market and the five largest firms approach half of total market share, a dynamic that shapes procurement strategy and negotiating leverage.

-

Schneider Electric — A global systems leader with an established EcoStruxure portfolio and recent product launches tailored to high-density AI workloads. Strong in integrated power and liquid-cooling architectures and in partnerships across hardware ecosystems.

-

Vertiv — A major provider of factory-integrated prefabricated infrastructure with product lines aimed at accelerated AI deployment, and recent global releases and partnerships that signal a push into turnkey, high-capacity factory modules.

-

Huawei — Vendor of containerized and prefabricated modular units optimized for telco, edge, and scalable deployments, with strong supply-chain integration and on-premises product families suited to rapid rollout.

-

Eaton, Delta Electronics — Power-centric suppliers offering modular solutions focused on resilience, UPS, and integrated power delivery — critical where uptime and local power constraints drive architecture.

-

Specialist integrators (BMarko, CenCore, Compu Dynamics Modular, PodTech, TAS) — These firms provide custom and turnkey factory-built solutions focused on edge, secure/TEMPEST-compliant deployments, and tailored high-density implementations for cloud providers, defense, and enterprise colocation.

Recent vendor moves underscore market dynamics: major launches and partnerships in late 2025 and early 2026 have accelerated the availability of AI-optimized prefabricated systems and strengthened factory-to-field value chains. Buyers should expect product roadmaps to be a decisive procurement criterion in 2026.

Strategic Implications for Enterprise Decision-Makers

-

From schedule to strategic capacity: Prefabrication converts months of on-site construction risk into factory-driven timelines. Organizations seeking rapid market entry, predictable OTTR (order-to-ready) windows, or phased capacity expansion will gain measurable advantage.

-

Energy and regulatory exposure must be modeled as a first-order cost. States and utilities are increasingly requiring data centers to fund incremental distribution and generation impacts; incorporate these scenarios into financial models and site comparisons.

-

Interoperability and vendor lock-in are expensive. Insist on modular interface standards, open mechanical and electrical designs where practicable, and contractual rights to migrate workloads across physical modules and vendors.

-

Financing and commercial models will diversify. Expect increased use of OPEX-based offerings, factory financing, and vendor-managed facilities as enterprises and hyperscale operators seek speed without capital overhang.

Five High-Impact Actions to Start Now

-

Embed regulatory scenarios in every site-selection and financial model: model utility rate pass-throughs, infrastructure cost allocation, and permitting timelines across best/worst/likely cases.

-

Require factory acceptance test (FAT) packages and systems-level interoperability clauses in RFPs to reduce integration risk and enable competitive multi-vendor sourcing.

-

Prioritize modular designs that are liquid-cooling ready and support high power density — retrofitting for advanced cooling is often costlier than specifying capability up-front.

-

Negotiate flexible commercial structures: hybrid CapEx/Opex contracts, milestone-linked payments, and warranty terms that align vendor incentives to operational performance.

-

Stress-test procurement against supply-chain shocks: include alternate sourcing, longer lead-time forecasts, and options for localized manufacturing or containerization to mitigate logistics risk.

Why PW Consulting’s Report Is Different

Our analysis couples large-sample quantitative forecasting (2020–2032) with primary interviews, vendor factory visits, and detailed procurement playbooks. The methodology blends macroeconomic drivers, policy simulations, and engineering-level cost models to produce a decision-ready output. Clients receive scenario-ready financial models, procurement templates, and a prioritized roadmap tailored to enterprise profiles — all designed to reduce time-to-decision and the probability of costly rework in deployment.

For strategic buyers and investors preparing plans in 2026, the difference between a playbook and a post-mortem is often the quality of the foresight applied today. This study is crafted to convert foresight into implementable actions.

To access the full report, including regional and segment-level breakdowns, the downloadable TCO tools, and our vendor scorecards, please consult the PW Consulting publication page. The detailed segment matrices and primary-source appendices are held in the full report to preserve the integrity of our proprietary research and to support high-trust client engagements.

PW Consulting — helping leaders translate modular infrastructure momentum into durable competitive advantage for the decade ahead.

For detailed analysis of this topic, please visit the official page: Prefabricated And Modular Data Centers Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.