PW Consulting: Aviation Oxygen Systems Market (Base Year 2025) Poised to Hit USD 9,010.13 Million by 2032 at a 6.8% CAGR (2026–2032) — North America Leads with USD 2,126.23M

PW Consulting: Strategic Brief — Aviation Oxygen Systems Market Outlook 2026 (Executive Trailer)

As airlines, OEMs, defense integrators, and aftermarket players finalize budgets and capital plans for 2026, the aviation oxygen systems market presents a mix of steady expansion, regulatory-driven churn, and concentrated competitive dynamics. PW Consulting’s forthcoming full-length market study — based on a 2025 base year and a 2026–2032 forecast horizon — synthesizes macro growth, regulatory inflection points, and tactical go-to-market playbooks that executives will need to convert opportunity into defensible revenue and margin streams.

Aviation Oxygen Systems Market

Macro snapshot: measured growth, durable upside

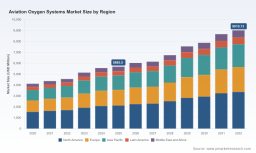

The global aviation oxygen systems market has demonstrated resilient recovery and multi-year expansion. From a market size of approximately USD 4.12 billion in 2020, the industry reached roughly USD 5.69 billion by the 2025 base year and is projected to surpass USD 9.01 billion by 2032. That trajectory corresponds to a compound annual growth rate (CAGR) in the mid-single digits — 6.8% in our core forecast — underpinned by fleet renewals, increased regulatory scrutiny of portable breathing equipment (PBE) and oxygen delivery devices, and broader aftermarket spending on life‑support systems.

Aviation Oxygen Systems Market

For strategy teams planning resource allocation in 2026, this is neither a hypergrowth story nor a static, commoditized market: it is a steady expansion with episodic regulatory and technology-driven windows that reward timely investment in MRO capacity, product compliance, and integrated system offerings.

Aviation Oxygen Systems Market

Why this matters for 2026 decision cycles

- Budget prioritization: With a predictable growth path and clear regulatory vectors, CFOs can justify targeted CapEx for certification and MRO expansion while preserving optionality for inorganic growth.

- Product roadmap alignment: R&D and product leaders should synchronize next‑generation offerings — from pulse‑dose delivery and low‑weight cylinder tech to on‑board oxygen generation systems (OBOGS) for specific platforms — with the regulatory calendar and fleet modernization timelines.

- Aftermarket and service-led differentiation: As operators seek to de-risk in-flight safety and reduce ground time, MRO and service contracts will be a major driver of aftermarket revenues in 2026 and beyond.

Regulatory environment: the near-term gating items

Regulation is an active and structural market force in aviation oxygen systems. Recent airworthiness directives and operational mandates affecting portable breathing equipment and maintenance practices have increased the compliance burden for operators and suppliers. FAA requirements for supplemental oxygen use by crew and for passenger oxygen deployment at defined flight levels remain foundational constraints that drive both equipment specifications and training/MRO cycles.

Additionally, oxygen purity and cylinder maintenance standards (including hydrostatic testing intervals) create recurring demand for certified repair stations, spare parts, and replacement units — all categories with differentiated margin profiles. These regulatory realities mean that companies that can demonstrate rigorous process control, documented traceability, and quick compliance turnarounds will capture outsized share in the aftermarket.

Competitive landscape — concentrated but dynamic

The market exhibits moderate concentration: the top three firms control a meaningful share of industry revenues, and the top five reach a clear majority. That structure creates a two-speed competitive field: larger incumbents focus on systems integration, OEM partnerships, and defense contracts, while agile specialists compete on niche products, aftermarket service, and certification speed.

- Aerox Aviation Oxygen Systems (Bonita Springs, FL) — strong footprint in portable and installed solutions plus recent MRO expansion through acquisition activity. Their move into certified repair capabilities materially alters their service economics and shortens lead times for operators.

- Safran Aerosystems Oxygen (AVOX Systems) (Lancaster, NY) — a global designer/manufacturer with a long legacy in passenger and crew oxygen hardware; recent regulatory actions impacting certain PBEs have elevated the visibility of their product family across operators and regulators.

- Collins Aerospace (RTX) (Charlotte, NC) — leverages scale in integrated cabin systems and PSU/oxygen integration, a go‑to partner for large commercial platforms where cross‑system integration wins contract awards.

- Precise Flight, Mountain High, Meggitt/Parker, Honeywell Aerospace — each firm brings domain specialization, from general aviation pulse‑demand systems to military OBOGS and modular airborne oxygen systems; these players are the primary competition in niche and mission‑critical segments.

Recent industry developments illustrate how competitive and regulatory events can immediately re‑rank suppliers. Notably, MRO capability expansion via acquisition and airworthiness directives targeting portable units have both reshuffled attention and created short‑term replacement demand. For market entrants and incumbents alike, those dynamics translate to concrete pressures: the need to prove compliance, maintain parts inventories, and manage certification pathways efficiently.

Report highlights — what the full study delivers (practical, executable content)

PW Consulting’s full report is intentionally operational. It is built for strategic and commercial teams that must make executable decisions in 2026 rather than academic forecasts. The core deliverables include:

- Proprietary market sizing and forecast model (2020–2032) with scenario toggles for fleet renewal pace, regulatory shock events, and defense procurement cycles;

- Risked financial archetypes for OEMs, MRO operators, and aftermarket suppliers that quantify unit economics, service margins, and inventory/certification capital requirements;

- Regulatory impact mapping that translates airworthiness directives and oxygen purity/maintenance rules into product‑level compliance roadmaps and time‑to‑market implications;

- Supplier capability matrix and sourcing playbook covering certification speed, geographic service coverage, lead times, and strategic MRO partnerships;

- Go‑to‑market options for both incumbents and new entrants: value‑based pricing models, bundled service contracts, digital monitoring/telemetry for predictive maintenance, and aftermarket growth strategies;

- Execution checklists for 100‑, 365‑ and 1,000‑day planning horizons to operationalize actions across R&D, regulatory, supply chain, and commercial teams;

- Downloadable data tables and an interactive dashboard supporting custom scenario analysis for board presentations and investment committees.

To preserve competitive confidentiality, the public executive summary intentionally omits the granular geographic and application splits — these are available in the full dataset and model package on the PW Consulting portal.

Strategic imperatives for each leadership agenda in 2026

- CEO/Board: Treat MRO capabilities and certification velocity as strategic assets. Consider tuck‑in acquisitions or partnerships that reduce time‑to‑service and widen addressable aftermarket.

- CFO: Reframe CapEx to include certification pipelines and inventory buffers for critical oxygen components. Evaluate service subscription and extended warranty structures to smooth revenue seasonality.

- Head of Product/R&D: Prioritize low‑weight, low‑cost pulse‑demand solutions for general and business aviation while accelerating resilience and fail‑safe designs for crew and military systems. Build certification milestones into product timelines.

- Commercial/Sales: Offer bundled compliance packages (equipment + installation + documentation + scheduled hydrostatic testing) to convert regulatory pain into recurring revenue.

- Supply Chain: Secure dual sources for critical components; optimize cylinder lifecycle management; and partner with certified repair stations to reduce lead times.

Opportunities and risks — a pragmatic view

- Opportunities: Aftermarket services, MRO, and compliance upgrades generate higher margin and recurring revenues; integrated systems (e.g., oxygen + PSU integration) create defensible OEM relationships; technology upgrades (OBOGS, smarter regulators) unlock premium pricing.

- Risks: Regulatory actions can create one‑off replacement demand but also raise certification costs and product obsolescence risk; supply chain fragility for specialty cylinders and valves can disrupt delivery schedules; consolidation among top suppliers can intensify procurement competition for smaller players.

How to use this study in 2026 planning

Executives should use the PW Consulting report to calibrate three decisions before the H1 2026 budget freeze:

- Which product lines receive accelerated investment (R&D and certification) versus which are transitioned to third‑party MRO partners?

- What service bundles and subscription pricing structures to pilot in Q2–Q3 2026 that convert regulatory compliance into recurring revenue?

- Which acquisition or partnership targets (MRO networks, certified repair stations, telemetry providers) to prioritize in order to reduce time‑to‑market and expand aftermarket control?

Next steps — where PW Consulting adds immediate value

PW Consulting offers an executive briefing package and bespoke scenario workstreams designed for rapid integration into 2026 planning cycles. Options include a 90‑minute board briefing, a custom five‑year P&L stress test with your product mix, and a certification acceleration playbook tailored to your manufacturing footprint.

Note: The public executive trailer is intentionally high‑level. The full report includes the granular market model, country and application splits, unit‑level cost assumptions, and a log of regulatory notices. Those datasets are essential for precise revenue forecasting, bid pricing, and capital allocation and are available to licensed subscribers.

Final thought

The aviation oxygen systems market in 2026 will reward disciplined operators who can marry technical compliance with aftermarket service excellence. With a clear mid‑single digit CAGR and predictable regulatory cycles, the path to differentiated returns is through certification velocity, service integration, and nimble supply chain management. PW Consulting’s full report equips leaders to make those choices with confidence — and converts regulatory complexity into strategic advantage.

For detailed analysis of this topic, please visit the official page: Aviation Oxygen Systems Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.