PW Consulting: Retail Supply Chain IT Transformation Market Poised to More Than Double to USD 27.99 Billion by 2032 (9.85% CAGR)

Supply Chain IT Transformation Services for Retail: Strategic Imperatives for 2026

PW Consulting’s latest market research — Supply Chain IT Transformation Services for Retail Market (base year 2025, forecast 2026–2032) — is designed as an operational playbook for retail leaders making pivotal investment decisions in 2026. The research synthesizes market dynamics, vendor capabilities, regulatory pressures and pragmatic implementation guidance so executives can convert digital supply chain intent into measurable outcomes. This briefing summarizes the report’s strategic value and points executives to the specific modules in the full study that will accelerate decision-making and de-risk program delivery.

Supply Chain IT Transformation Services for Retail Market

Market trajectory: scale, growth and the investment window

The market for supply chain IT transformation services serving retail has moved from a niche investment to a mainstream strategic priority. Our market sizing shows expansion from roughly USD 9 billion in 2020 to USD 14.5 billion in 2025, with an expected uplift into the mid‑teens in 2026 and a longer-term trajectory that reaches the high‑twenties by 2032. The compound annual growth rate through the forecast window is 9.85%, underscoring sustained vendor investment, growing buyer demand, and an ongoing shift toward platform-centric, analytics‑driven supply chains.

Supply Chain IT Transformation Services for Retail Market

For 2026, the practical takeaway is clear: the market is large enough to support multiple program approaches (internal build, platform partnership, or managed service), but still captures outsized value for organizations that move early to modernize core planning, fulfilment and compliance capabilities. The size and growth imply a robust vendor ecosystem and healthy buyer choice — but success will depend on rigorous vendor selection and staged execution to convert potential into realized value.

Supply Chain IT Transformation Services for Retail Market

Primary drivers shaping 2026 decisions

- AI and visibility acceleration: Industry tracking shows a meaningful step‑change in AI adoption for supply chain visibility — a material share of retailers already embed AI today, and adoption is accelerating year‑over‑year. Expect rapid expansion in projects that fuse AI with real‑time telemetry to reduce stockouts, improve demand sensing and automate exception management.

- Regulatory traceability demands: New rules such as the EU’s Packaging and Packaging Waste Regulation (PPWR), Extended Producer Responsibility (EPR) requirements and similar regional mandates are translating directly into IT requirements for traceability, digital product passports and recycled‑content reporting. These are not peripheral IT upgrades — they require integration across PLM, ERP, WMS and supplier networks.

- Data privacy and governance: GDPR, CCPA and evolving privacy frameworks mean that supply chain telemetry and customer‑linked fulfilment data need robust governance, privacy‑by‑design, and contractual controls with third‑party technology vendors.

- Workforce and operational cost pressures: Rising labor costs and jurisdictional labor reforms — for example, shifts to shorter workweeks or enhanced pay transparency requirements in multiple markets — increase the premium on automation, ergonomics, and workforce optimization features in transformation programs.

- Omnichannel complexity and resilience: Customer expectations and e‑commerce persist as structural drivers; retailers investing in orchestration layer, distributed fulfilment and advanced order management realize differentiated service economics.

2026 strategic priorities — a practitioner’s checklist

- Start with visibility and forecasting: Prioritize projects that reduce lead time and improve demand accuracy. Early wins often come from integrating point‑of‑sale and inventory telemetry with cloud‑based demand engines and a single source of truth for inventory.

- Embed compliance as a feature, not a bolt‑on: Treat traceability, recycled content validation and digital passporting as core functional requirements for any modernization program — this reduces rework and shortens certification timelines.

- Adopt an AI‑first, outcomes‑driven approach: Focus pilots on measurable outcomes (forecast accuracy, inventory turns, order‑fulfilment cost). Use PoCs to validate models and build measurable business cases before enterprise roll‑out.

- Design for hybrid architectures: Balance edge and cloud processing for latency‑sensitive fulfilment tasks while centralizing analytics on cloud platforms for cross‑store optimization and advanced forecasting.

- Prioritize vendor‑partnership models: Choose partners with retail‑specific IP, proven execution references and ecosystem alliances — success is rarely achieved by a single supplier acting in isolation.

Competitive landscape — how to interpret vendor capabilities in 2026

The competitive environment blends global systems integrators, large professional services firms and specialized retail consultancies. Leading integrators bring scale, cross‑industry delivery models and broad platform partnerships; boutique players contribute vertical depth and rapid configuration for retail specifics.

- Tata Consultancy Services (TCS): Noted for end‑to‑end supply chain transformation offerings, TCS combines advisory‑led transformation with AI‑powered optimization and deep platform partnerships. Recent analyst recognition underscores its execution capability on complex retail and CPG programs.

- Cognizant: Positioned on modernization, demand forecasting and resilience initiatives; strong in IT modernization paths that link digital planning with legacy landscapes.

- Accenture: Emphasizes network orchestration, AI and automation across Oracle and other core platforms — a common choice for large, multinational retailers seeking integrated transformation.

- Deloitte and PwC: These firms blend strategic supply chain advisory with systems implementation, and their public guidance emphasizes AI adoption, flexible networks and resilience as central to retail strategy in 2026 and beyond.

- IBM, Brillio and specialist consultancies (e.g., Parker Avery): These players offer combinations of advanced analytics, rapid forecasting capability and hands‑on retail experience for mid‑market and specialist use cases.

For procurement teams, the implication is to evaluate vendors on five dimensions: (1) retail domain IP and referenceability; (2) ability to deliver compliance and data governance; (3) outcome‑based pricing and TCO transparency; (4) integration accelerators and partner ecosystem; and (5) change management and adoption services.

What PW Consulting’s full report delivers (practical, implementation‑oriented)

- Actionable market sizing and trajectory: Granular macro view with base‑year context (2025) and a forward forecast (2026–2032) that shows where investment capacity is expanding and which capability investments index to the strongest growth pockets.

- Decision frameworks and roadmaps: Playbooks for rapid assessment, build vs. buy decision trees, pilot design templates and 12–36 month implementation roadmaps translated into procurement milestones.

- Vendor benchmarking and go‑to‑market playbooks: Comparative profiles, strengths/weaknesses and partnership strategies for integrators, consultancies and niche specialists — accompanied by vendor selection scorecards you can reuse in RFPs.

- Operational tools: TCO and ROI calculators, contract negotiation checklists (including data privacy and compliance clauses), KPI dashboards and implementation risk matrices tailored to retail contexts.

- Scenario and sensitivity modelling: Regulatory impact models (traceability, EPR), AI adoption scenarios (near, medium and long term) and workforce cost sensitivity analyses to inform prioritization and capital allocation.

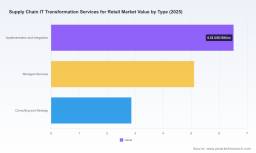

Importantly, the core segmentation insights (regional, service‑type and application breakdowns) and the more granular vendor share data are intentionally presented in the full report rather than in this briefing. That lets readers access the segmentation tables, heatmaps and downloadable tools that are most actionable for procurement and program planning.

Using the report to shape 2026 investments — recommended sequencing

- Immediate (0–6 months): Conduct a compliance gap assessment (traceability, packaging regulation, privacy). Run a rapid technology audit to identify integration blockers and low‑hanging automation opportunities.

- Short term (6–12 months): Execute focused PoCs on AI‑enabled visibility and demand sensing tied to clear KPIs. Negotiate modular contracts with outcome clauses and convertible pilots that permit scale‑up.

- Medium term (12–24 months): Roll out platform consolidation, integrate supplier data for full traceability, and scale workforce optimization technologies to align with labor regulation changes.

- Metrics to track: forecast accuracy, inventory days of supply, order fulfilment cost per order, compliance cycle time for packaging reporting, and measured ROI for AI pilots.

Concluding view — why 2026 is decisive

2026 represents a moment of convergence: regulatory requirements, rising labor and operational costs, and a clear maturation of AI and cloud technologies create a narrow window where early adopters can realize durable competitive advantage. The market’s growth profile — rising consistently from 2020 through the 2025 base year and forecast to expand materially across the 2026–2032 horizon — validates continued investment. But size alone does not guarantee success: disciplined prioritization, vendor selection finesse and pragmatic execution discipline determine winners.

PW Consulting’s Supply Chain IT Transformation Services for Retail Market report packages the macro market context with a hands‑on set of tools and frameworks to help retail executives make faster, less risky, and more measurable decisions in 2026. We deliberately present this summary as a strategic preview; detailed segmentation, vendor share matrices, downloadable tools and full implementation templates are available in the complete report.

To access the full intelligence, benchmarking tools and implementation playbooks that underpin this briefing, please visit PW Consulting’s report page or contact our advisory team for a tailored briefing. Our analysts are available to walk through scenario models and to co‑design a roadmap aligned to your specific retail operating model and regulatory footprint.

For detailed analysis of this topic, please visit the official page: Supply Chain IT Transformation Services for Retail Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.