PW Consulting: Lacrimal Stent Tube Market to Reach USD 317.85 Million by 2032 at a 5.48% CAGR — North America Leads with USD 79.83 Million

Lacrimal Stent Tube Market 2026 Strategic Preview: Actionable Intelligence for Boardrooms and Business Units

Executive summary

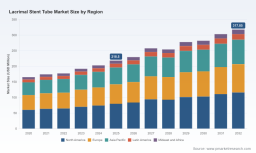

As healthcare systems normalize post-pandemic and outpatient ophthalmic procedures continue to expand, the lacrimal stent tube market is entering a phase of steady, investment-grade growth. Our latest market model projects the global market rising from USD 218.5 Million in 2025 to approximately USD 317.9 Million by 2032, reflecting a compound annual growth rate (CAGR) of roughly 5.5% over the 2026–2032 forecast horizon. That trajectory is driven by converging forces: aging demographics and procedural volumes, iterative product innovation (materials, coatings, and delivery systems), and incremental reimbursement tailwinds for lacrimal procedures.

Lacrimal Stent Tube Market

This preview summarizes the strategic value of PW Consulting’s full Lacrimal Stent Tube Market report for organizations making 2026 resource-allocation decisions. It highlights the practical, executable insights the report delivers for portfolio leaders, M&A teams, commercial executives, and regulatory affairs groups—while intentionally withholding granular segment breakdowns to preserve the premium consultative value found in the full publication.

Lacrimal Stent Tube Market

Why this market matters to 2026 decision-makers

-

Predictable, mid-single-digit growth creates a low-risk runway for targeted investments. The market’s projected climb to roughly USD 318 Million by 2032 signals an environment where product refinements and channel optimisation can deliver measurable returns without needing mass-market disruption.

Lacrimal Stent Tube Market -

Fragmented clinical needs and durable clinical pathways (DCR, CNLDO, punctal & canalicular repair, and bypass procedures) mean multiple routes to commercialization: disposable intubation sets, long-term bypass solutions, and specialty consumables. Each route carries distinct margin profiles and go-to-market implications.

-

Regulatory and reimbursement landscapes are navigable but require tactical planning. Most lacrimal stents fall under FDA Class II pathways and 510(k) submissions; reimbursement typically aligns with established CPT codes for nasolacrimal interventions. These realities lower time-to-market and support near-term launch strategies—provided regulatory programs and coding strategies are planned up-front.

What the full PW Consulting report delivers

Our market study is designed as an operational playbook for 2026. The report blends quantitative forecasting with hands-on, executable guidance:

-

Market sizing and scenario modeling: base case and two stress cases with pricing, reimbursement, and procedure-volume sensitivities to test assumptions under different healthcare recovery paths.

-

Commercial segmentation frameworks: clinician decision drivers, procurement behaviors in ambulatory surgery centers and hospitals, and a channel map for OEMs and distributors—presented so commercial leaders can reallocate sales force activities and tailor messaging.

-

Product development priorities: material and coating trends, delivery-system ergonomics, and evidence-generating study designs that meaningfully shorten adoption cycles among otolaryngologists and oculoplastic surgeons.

-

Regulatory and reimbursement playbooks: stepwise 510(k) strategies, FDA predicate analysis, and CPT/coverage tactics that align clinical evidence plans to near-term coding opportunities.

-

M&A and partnership intelligence: target archetypes, valuation multipliers, and integration checklists that reflect the market’s competitive dynamics and consolidation potential.

-

Risk matrix and mitigation templates: supply-chain contingencies, sterilization validation priorities (ISO-compliant processes), and clinical device stewardship for single-use labeling that reduce recall and liability risk.

Competitive landscape — who moves the market

The competitive field combines specialist manufacturers, diversified ophthalmic device players, and regional producers. Key industry participants profiled in the report include established suppliers with deep lacrimal portfolios and niche innovators in materials and delivery systems. Representative examples:

-

FCI Ophthalmics (Pembroke, MA) — A broad lacrimal portfolio with multiple self-retaining and canalicular solutions; commercial momentum is underpinned by sustained product presentations and clinician engagement.

-

Kaneka Medical (Osaka / U.S. operations) — Focused offerings with hydrophilic coatings aimed at improving handling and insertion performance in both congenital and acquired indications.

-

Bess Medizintechnik (Germany) and Aurolab (India) — Regional specialists that combine surgical instruments with stent solutions, serving both tertiary centers and high-volume regional markets.

-

Beaver-Visitec International (BVI Medical) — Part of a broader ophthalmic surgical portfolio; recent portfolio strengthening shows strategic intent to capture procedure-adjacent demand.

-

Gunther Weiss Scientific Glassblowing — A long-standing, niche supplier of glass Jones tubes for specialized bypass indications, illustrating the coexistence of commodity and high-specialty segments.

Market concentration is meaningful but not prohibitive—top players hold a material share of competitive advantage through channel relationships, clinician training programs, and IP on delivery mechanisms. Our report maps supplier positioning against clinician preferences, inventory dynamics, and purchasing behaviors so executives can prioritize competitive responses that matter in 2026.

Regulatory, reimbursement, and clinical dynamics

-

Regulatory pathways: The majority of lacrimal stents and intubation sets are eligible for FDA Class II 510(k) submissions, enabling faster market entry relative to novel implants. That said, device-specific sterility validation and labeling (single-use, sterile) are table stakes—our report provides a checklist to secure predictable 510(k) outcomes.

-

Reimbursement: Established CPT codes exist for nasolacrimal probing with tube/stent insertion, creating a clear coding anchor for commercial planning. Still, reimbursement levels and payer policies vary regionally—our payer-mapping tool quantifies the impact of coding changes on commercial viability.

-

Clinical practice patterns: Silicone remains the dominant material due to proven biocompatibility and handling characteristics. Temporary intubation is the common treatment course; however, long-term bypass solutions (e.g., Jones tubes) retain a specialized but important role. The report dissects clinical decision trees by indication and case complexity to identify the highest-impact use cases for targeted evidence development.

Strategic playbook for 2026

We advise commercial and corporate development leaders to focus on three parallel plays in 2026:

-

Product-line optimization: Prioritize incremental improvements that reduce OR time and enhance first-pass success (e.g., hydrophilic coatings, pre-loaded introducer systems). Investments here yield faster adoption and lower sales-cycle friction.

-

Channel and training investments: Shift a portion of selling resources toward high-volume outpatient centers and specialty clinics, supported by targeted clinician training and outcomes data. Our segmentation model identifies the subchannels with the highest ROI for field deployment.

-

Adjacency capture and partnerships: Consider bolt-on acquisitions or OEM partnerships to fill gaps in consumables, probes, and patient-facing product families. The market structure supports tuck-ins that expand procedure coverage without requiring steep incremental fixed costs.

Operational considerations and risks

Execution risks are manageable but real. Key operational levers to control in 2026 include sterilization and single-use validation, supplier quality and lead times for medical-grade silicone, and the cadence of clinical evidence collection to sustain payer conversations. The full report includes a prioritized mitigation roadmap and vendor assessment templates to reduce implementation friction.

Why PW Consulting’s full report is the right tool for your 2026 planning

-

Actionability: We translate market forecasts into executive-level resource allocations and 90–180 day tactical plans for product, commercial, and regulatory teams.

-

Proven methodology: Forecasts and scenarios are grounded in verified procedure volumes, device-class trends, and supplier intelligence gathered through primary interviews and validated secondary sources.

-

Competitive insights: Company profiles and recent developments are synthesized into defensible strategic options—whether the goal is to defend, grow, or consolidate positions.

-

Decision-focused deliverables: The package contains investment memos, win-loss hypotheses, and integration checklists designed for rapid use by corporate development committees and business unit leaders.

Limitations of this preview and next steps

This preview outlines the macro trajectory and strategic implications while withholding the granular segmentation tables, regional and application splits, and scenario-specific revenue waterfalls that are included in the paid report. Those detailed breakdowns are intentionally reserved to preserve the tactical advantage and the consultative value of the full deliverable.

For procurement teams, commercial leaders, M&A desks, and R&D heads preparing 2026 budgets, the full PW Consulting Lacrimal Stent Tube Market report provides the granular inputs and executable templates necessary to convert market opportunity into measurable outcomes. Contact our team to request the full report and receive a customized briefing tailored to your strategy, whether that is targeted product launches, market entry, or acquisition due diligence.

For detailed analysis of this topic, please visit the official page: Lacrimal Stent Tube Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.