PW Consulting: Aerospace Aircraft Stainless Steel Market to Expand at 5.45% CAGR During 2026–2032, 2025 Report Reveals

Aerospace Aircraft Stainless Steel Market: Strategic Intelligence for 2026 Decision-Makers

Executive Snapshot

PW Consulting is pleased to publish an actionable intelligence brief drawn from our comprehensive Aerospace Aircraft Stainless Steel Market study. Built on a base year of 2025 and projecting through 2032, the report synthesizes market-sizing, cost dynamics, regulatory pressures, supplier capabilities, and near-term demand scenarios that will shape procurement, production, and M&A decisions in 2026 and beyond.

Aerospace Aircraft Stainless Steel Market

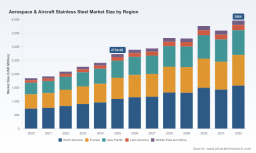

Key macro takeaways: the market has expanded steadily from recent historical levels and, with a compound annual growth rate (CAGR) of 5.45% over the forecast window, is set to continue its recovery and structural growth. Using revenue measured in USD Million, the industry’s trajectory from 2020 through our forecast to 2032 demonstrates both cyclical inflection points and enduring secular drivers that matter to C-suite and strategy teams planning for 2026.

Aerospace Aircraft Stainless Steel Market

Why this report matters for 2026 strategy

-

Timing and precision: 2026 is a pivot year—new regulatory regimes, commodity volatility, and sovereign industrial policy are converging to create asymmetric risks and opportunities across aerospace stainless steel supply chains.

Aerospace Aircraft Stainless Steel Market -

Tactical clarity: buyers, fabricators, and investors need near-term tools to translate price signals and regulatory impacts into sourcing, hedging, and capital allocation decisions. Our report provides those tools in operational form.

-

Portfolio reshaping: the combination of steady market growth and concentrated supplier positions means selective vertical integration, partnership, or bolt-on M&A can create outsized value; the report surfaces where those opportunities are most likely to materialize without exposing confidential segment-level payoffs in this summary.

Market trajectory: what the numbers tell us

The dataset anchoring the report tracks total market revenue (USD Million) through the historical period and out to 2032. From a post-pandemic recovery start in 2020, the market reaches an approximate midpoint in 2025 and is forecast to continue rising to materially higher levels by 2032. This pattern—steady annual expansion reflected in a 5.45% CAGR across the forecast horizon—signals robust demand fundamentals but with episodic volatility tied to commodity cycles and regulatory shocks. The report decomposes that macro trajectory into demand scenarios and supply-side reactions, enabling executives to stress-test plans under alternative 2026 market conditions.

Drivers, risks and structural dynamics

-

Commodity and input-cost pressure: North American stainless steel pricing data from March 2026 points to price levels that reflect significant upstream inflation; nickel remains a dominant driver of variable production cost—accounting for a very large share of the cost base in common austenitic formulations. This means small nickel price movements can materially change margins for processors and component manufacturers.

-

Policy and trade: The European Union’s Carbon Border Adjustment Mechanism (CBAM) entering its payment phase in early 2026 and the continued existence of U.S. Section 232 tariffs on steel and aluminum as of April 2026 introduce both cost and compliance layers that reshape cross-border sourcing economics, favor near-shore strategies, and alter supplier selection criteria.

-

Industrial strategy: National-level efforts—most notably policy signals from China emphasizing high-tech sectors including aerospace—add asymmetric demand upside for specialty stainless grades and advanced processing capabilities in targeted jurisdictions.

-

Market concentration: The competitive field exhibits measurable concentration at the top end; leading suppliers account for a substantial portion of supply, creating supplier power and signaling the potential for strategic partnerships or supplier risk should capacity shifts occur.

What PW Consulting’s report delivers (practical, decision-grade content)

This study was intentionally designed as a toolkit for executives who must make real-world decisions in 2026. Highlights include:

-

Market sizing and validated forecast models calibrated to 2025 base-year data, with scenario variants that isolate regulatory, commodity, and demand shocks.

-

End-to-end supply chain maps for aerospace stainless steel, showing where value concentrates, where single points of failure exist, and how material flows respond to trade and tariff shifts.

-

Cost-curve analysis that quantifies the sensitivity of tiered producers and distributors to nickel and ferroalloy movements, plus an embedded TCO (total cost of ownership) calculator to compare sourcing alternatives under CBAM and tariff regimes.

-

Proprietary supplier scorecards and a five-factor stress-test matrix for assessing continuity risk, carbon-intensity exposure, and scale economics across potential partners.

-

Procurement playbooks—covering hedging, contract structures, dual-sourcing arrangements, and inventory strategies—tailored to OEMs, tier suppliers, and distributors operating in the aerospace segment.

-

Capex and expansion decision frameworks for downstream fabricators: build vs. buy scenarios, greenfield vs. brownfield assumptions, and payback profiles under multiple price and demand paths.

-

M&A and JV prioritization guidance that aligns strategic intent with integration complexity and regulatory horizons—enabling acquirers to size deals and prioritize targets without exposing proprietary subsegment valuations in this summary.

Competitive landscape: profiles and strategic implications

The report includes a focused review of incumbent and emerging players whose strategic moves will define supply capacity, service quality, and product innovation over the next three years. Notable firms examined include:

-

Outokumpu (Helsinki, Finland) — A global stainless solutions leader whose technical portfolio and high-temperature/corrosion-resistant grades position it as a natural partner for advanced aerospace applications. The firm’s scale and R&D footprint make it a bellwether for pricing and specification shifts.

-

Service Steel Aerospace (Fife, WA, USA) — A major distributor focused on aerospace-quality stainless and alloys. Recent capacity additions in North America underline a strategy that pairs distribution scale with quick-turn service to OEMs and cross-border fabricators.

-

Universal Stainless (Bridgeville, PA, USA) — Specialty producer of aircraft-grade stainless and nickel alloys that plays a critical role in supplying structural and engine-related billets and forgings; its product mix makes it sensitive to nickel and alloy premia.

-

Carpenter Technology (Reading, PA, USA) — Serves extreme-performance niches with high-end alloys and tailored metallurgy for engine and high-stress applications; its portfolio is strategic for OEMs pursuing weight and life improvements.

-

BUTTING (Knesebeck, Germany) — Known for precision tubes and ready-to-install assemblies, an important supplier in regions prioritizing integrated component supply and near-net-shape manufacturing.

-

Continental Steel & Tube Co., Future Metals and other specialized distributors — Collectively, these channel players underpin speed-to-market, small-batch capability, and aftermarket responsiveness.

Recent industry developments—facility expansions by distribution firms, new manufacturing hubs aimed at defense and aerospace customers, and concentrated showing at regional trade exhibitions—reinforce the strategic value of combining scale, geographic reach, and certification depth. PW Consulting’s report provides decision-makers with a comparative matrix that captures capability, lead-time risk, and carbon exposure for each major supplier.

Actionable recommendations for 2026

-

Hedge and stress-test: Implement commodity hedges and run three-tier scenario stress tests (base, tariff-adverse, carbon-compliant) using the report’s models to understand margin corridors and working-capital needs.

-

Rebalance sourcing: Prioritize a mix of near-shore and certified global suppliers to hedge against tariff and CBAM shocks while preserving cost competitiveness.

-

Negotiate outcome-linked contracts: Use performance-based pricing and indexation mechanisms tied to key input price indices to share upside and downside with strategic suppliers.

-

Invest in low-carbon pathways: Start capex planning for decarbonization investments (recycling, electrification, green energy procurement) and engage with suppliers on shared carbon-intensity roadmaps to avoid CBAM penalties and to access green-premium markets.

-

Targeted M&A: Pursue bolt-on assets that deliver immediate capacity, certification, or geographic diversification—using the report’s acquisition screening framework to prioritize targets that improve resilience while keeping integration risk manageable.

Access and next steps

This announcement intentionally outlines the strategic contours and actionable takeaways from PW Consulting’s Aerospace Aircraft Stainless Steel Market report while reserving the full, granular datasets, supplier-level valuation models, and downloadable tools for subscribers. For teams deploying 2026 operating plans, the report offers the necessary modeling artifacts, negotiation templates, and scenario outputs to convert insight into execution.

Executives seeking to operationalize the analysis can request a tailored briefing, license the embedded calculators, or commission a bespoke deep-dive focused on their supply chain cluster. Our research supports integration into ERP/planning systems and provides client workshops to translate scenarios into 90–180 day tactical roadmaps.

Conclusion

As the aerospace sector recalibrates for a new regime of regulation, commodity volatility, and sovereign industrial strategy, decision-makers cannot rely on static benchmarks. PW Consulting’s market study provides a dynamic, implementable intelligence layer—combining validated market sizing (USD Million base-year 2025), a 5.45% CAGR forecast window, supplier concentration analysis, and operational toolkits—to guide procurement, capital, and M&A decisions in 2026. For the complete dataset, supplier scorecards, and interactive tools that underpin these recommendations, please consult the full report via our release portal.

For detailed analysis of this topic, please visit the official page: Aerospace Aircraft Stainless Steel Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.