PW Consulting Forecasts Aldosteronism Treatments Market to Hit USD 3,127.6 Million by 2032

Aldosteronism Treatments Market 2026: Strategic Imperatives from PW Consulting’s New Market Intelligence Brief

As health systems and biopharma executives enter 2026, choices made this year will materially shape competitive positioning across the aldosteronism treatments landscape for the remainder of the decade. PW Consulting’s new market research brief — using 2025 as its base year and projecting through 2032 — provides an actionable, decision-focused view of the market that bridges clinical science, commercial realities, and payer dynamics.

Aldosteronism Treatments Market

Headline market pulse (concise)

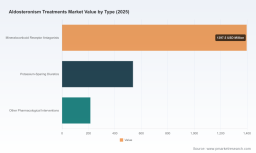

Our proprietary market model estimates the global aldosteronism treatments market at approximately USD 2,150.0 Million in 2025, growing to about USD 2,268.3 Million in 2026 and reaching USD 3,127.6 Million by 2032. The model assumes a mid-term compound annual growth rate (CAGR) of 5.5% for the 2026–2032 forecast window. Market concentration is moderate: the top three competitors account for a material share, and the top five together control a clear majority of the commercial value — an important indicator for competitive and M&A strategy.

Aldosteronism Treatments Market

Why this brief is strategic for 2026 decision-making

- Timing of competitive inflection: 2026 marks the commercial introduction of new mechanism-of-action agents alongside an entrenched generic base. Our brief synthesizes how these forces interact and what they mean for launch sequencing, pricing, and contracting.

- Payer and guideline dynamics: Updated clinical guidelines and evolving reimbursement practice are already reshaping standard-of-care choices. Executives who align clinical development and HEOR efforts to payer expectations early will secure advantaged access pathways.

- Portfolio prioritization: With constrained R&D budgets and heightened M&A activity in specialty cardiovascular/metabolic space, the brief helps teams differentiate high-conviction opportunities from low-return investments.

- Operational readiness: Supply-chain continuity for steroidal APIs, hospital channel dynamics, and retail/online distribution strategies are all covered with scenarios and contingency plans actionable in 2026.

What’s inside — practical deliverables for commercial and clinical leaders

The report is built as an execution toolkit rather than an academic exercise. Key actionable components include:

Aldosteronism Treatments Market

- Market sizing and multi-scenario forecasts (base, conservative, and accelerated adoption) with transparent assumptions and sensitivity levers to stress-test executive hypotheses.

- Go-to-market blueprints tailored to product archetypes (innovator small-molecule, non-steroidal MRA, aldosterone synthase inhibitor, and generic), including hospital procurement, retail pharmacy, and digital channel playbooks.

- Payer and HTA playbooks: coverage likelihood matrices, pricing ceilings by scenario, and evidence-generation roadmaps that accelerate formulary acceptance and rebate negotiations.

- Clinical strategy alignment: recommended Phase II/III endpoints, trial design optimizations to support label expansion into primary aldosteronism, and targeted RWE protocols to demonstrate comparative effectiveness.

- Commercial due diligence templates and M&A scorecards that quantify strategic fit across clinics, geographies, and distribution routes.

- Regulatory pathway mapping and a risk register covering approval timelines, labeling implications, and post-market obligations.

Competitive landscape — who matters and why

The market remains a mix of established brand leaders, emerging innovators, and a broad generic supply base. Our competitive analysis synthesizes clinical positioning, patent and manufacturing footprints, and channel strength to project how share moves under alternate scenarios.

- AstraZeneca (Cambridge, UK) — Recent regulatory progress materially alters strategic dynamics. AstraZeneca’s aldosterone synthase inhibitor received regulatory approval in mid-2026 as an add-on therapy for uncontrolled hypertension, and its Phase 2a program has shown promise in primary aldosteronism. This entrant represents a new, non-MRA mechanism capable of creating distinct clinical niches and placing pressure on incumbent MRAs to demonstrate differentiated value.

- Pfizer Inc. (New York, USA) — As the commercial steward of legacy MRAs, Pfizer’s brands remain central to treatment algorithms and hospital procurement decisions. Their stewardship of existing portfolios and ability to pair clinical data with broad commercial reach is a key competitor dynamic.

- Bayer AG (Leverkusen, Germany) — With a non-steroidal mineralocorticoid receptor antagonist in market, Bayer’s positioning is clinically relevant in patient segments where tolerability and kidney-cardiac benefits are prioritized.

- Generic manufacturers (Viatris, Teva, Sandoz, Sun Pharma, Amneal, Accord, CMP Pharma and others) — Generics anchor price expectations and reimbursement pathways. Their manufacturing scale and long-standing presence in hospital and retail channels maintain a durable floor on share and pricing pressure.

Collectively, the market’s top three players control a material single-digit-to-double-digit share (moderate concentration), and the top five control a clear majority. That structure enables targeted disruption — for example, a well-evidenced novel therapy can capture premium pricing in defined populations despite a dominant generic background.

Recent regulatory, clinical and reimbursement shifts to watch

- Guideline updates in 2025 emphasized screening and endorsed established MRAs as first-line medical therapy in many primary aldosteronism scenarios. This created a near-term demand tail for generics while raising the evidentiary bar for new entrants seeking to replace or complement MRAs.

- FDA approval of a first-in-class aldosterone synthase inhibitor in 2026 (add-on for uncontrolled hypertension) expands therapeutic options and triggers rapid reassessments of treatment algorithms where clinicians seek steroid-sparing alternatives.

- Reimbursement pathways for generic spironolactone and eplerenone are well-established, reducing reimbursement risk for generics but increasing the need for premium therapies to demonstrate meaningful clinical and economic value.

- API supply dynamics for steroidal compounds remain stable, supported by multiple global suppliers — a resilience factor for manufacturers and contract manufacturers alike.

Strategic options for 2026 — recommended plays and near-term KPIs

Executives should adopt a portfolio approach to select from complementary strategic plays. Below are high-conviction options, each with recommended near-term KPIs for 2026:

- Defend core generics: Optimize hospital tender participation, secure preferred formulary positioning, and reduce manufacturing cost via supply-chain optimization. KPIs: tender win rate, unit production cost, gross margin retention.

- Invest in differentiated clinical assets: Accelerate Phase II/III readouts and HEOR programs for agents that address tolerability or organ-protection endpoints. KPIs: enrolment velocity, time-to-primary-endpoint, payer dialogue outcomes.

- Strategic M&A / licensing: Target bolt-on assets that provide label expansion or geographic breadth. KPIs: NPV accretion thresholds, time-to-integration, incremental revenue capture.

- Real-world evidence partnerships: Collaborate with academic centers and registries to generate comparative-effectiveness data that supports premium reimbursement and guideline inclusion. KPIs: RWE protocol approvals, published outcomes, payer decision impact.

- Payer-centric commercial models: Develop outcomes-based contracts and shared-savings arrangements for premium products in defined populations. KPIs: contract uptake, net price realized, patient adherence metrics.

How PW Consulting’s report converts insight into execution

PW Consulting’s brief is intentionally structured as a “strategy-to-execution” playbook. Clients receive:

- Transparent forecasting models with downloadable scenario inputs to re-run assumptions against custom product-level plans.

- Go-to-market templates and negotiation playbooks tailored to hospital, retail, and online pharmacy channels.

- Payer and HTA engagement roadmaps aligned to clinical endpoints and real-world evidence priorities.

- Competitive response playbooks keyed to potential AstraZeneca-type entrants, generics price erosion curves, and hospital formulary dynamics.

- M&A diligence checklists and valuation sensitivity analyses keyed to market concentration dynamics.

What we intentionally withhold in this public preview

In keeping with our “preview” principle, this note surfaces the market direction, competitive inflection points, and strategic frameworks without disclosing the granular segment-level splits, channel-level revenue allocations, or region-by-region monetary breakdowns contained in the full study. Those detailed tables, full company scorecards, and dataset extracts are available only through the full report and dataset package to preserve commercial confidentiality and to ensure clients receive a complete analytical context around critical segmentation assumptions.

Closing: take decisive steps this year

2026 is a pivotal year for aldosteronism treatments: new mechanisms are arriving while an established generics base continues to define pricing norms. Companies that translate the market’s macro trajectory (5.5% CAGR into 2032 and a projected near-term growth inflection) into clear, evidence-driven commercial and clinical programs will secure disproportionate value. PW Consulting’s report is designed to convert that macro trend into market-winning tactics — from launch sequencing and payer contracting to M&A screening and RWE deployment.

To access the full dataset, company scorecards, and downloadable scenario models that underpin these conclusions, please visit our report landing page or contact PW Consulting’s healthcare strategy team for a briefing and bespoke scenario modeling.

For detailed analysis of this topic, please visit the official page: Aldosteronism Treatments Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.