PW Consulting Forecast: Hot Melt Glue Market to Expand at a 6.2% CAGR Through 2032

Hot Melt Glue Market 2026: Strategic Imperatives from PW Consulting’s New Industry Brief

Executive snapshot

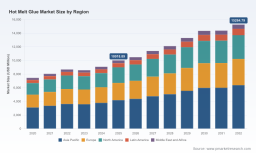

As manufacturers, procurement leaders and corporate strategists prepare budgets and roadmaps for 2026, the hot melt glue market presents a blend of steady growth, supply-chain complexity and regulatory pressure that demands intentional strategy. Our latest market brief — rooted in five years of historical analysis and a seven-year forecast — shows the global hot melt market expanding materially: from approximately USD 7,450 million in 2020 to USD 10,019 million in 2025, with a projected rise to roughly USD 15,265 million by 2032. PW Consulting’s forecast period (2026–2032) assumes a compound annual growth rate (CAGR) of 6.2% — a runway that rewards both innovation-led differentiation and disciplined operational execution.

Hot Melt Glue Market

Why this matters for 2026 decision-making

-

Timing of investment. Moderate, predictable growth combined with episodic raw-material shocks means capital investments (capacity expansion, new lines, or automation) should be staged and conditioned on scenario triggers rather than one-off bets.

Hot Melt Glue Market -

Margin resilience. Rising raw-material costs and regulatory compliance costs are compressing historical margin cushions. Procurement and product teams must coordinate hedging, formulation flexibility and price architecture to protect EBIT.

Hot Melt Glue Market -

Market structure. The sector displays moderate concentration: the top three players account for roughly 32% of sales and the top five about 46%. This dynamic rewards both scale strategies and nimble specialization by challengers.

Macro and supply-side dynamics shaping 2026

Several forces are converging to define competitor advantage next year:

-

Raw-material volatility. EVA copolymer prices have moved markedly (industry sources reported roughly a double-digit percentage increase year-over-year in recent periods), and hydrocarbon tackifier resin spot prices have surged to levels that materially affect formulation cost curves. These inputs often represent a large share of variable cost in hot melt formulations and generate stress on OEM and converter margins.

-

Regulatory tightening. New restrictions under major chemical regulations and labeling laws — including restrictions on certain phthalates and heightened consumer-facing disclosure regimes — raise compliance and substitution costs. Some U.S. states and the EU have implemented or signaled tighter thresholds that will accelerate reformulation needs.

-

Trade and tariff risk. Ongoing tariff regimes and trade measures continue to influence sourcing decisions and regional supply-chain designs, especially for resin and additive imports.

-

Sustainability and product innovation. Demand for lower-VOC, bio-based and more easily recyclable adhesive systems is expanding across packaging, hygiene and consumer segments. Suppliers with validated bio-based portfolios and third-party sustainability claims will find pricing and win-rate advantages.

Competitive landscape — positioning and recent moves

The market map combines global majors, regional specialists and contract manufacturers. PW Consulting’s qualitative benchmarking highlights the following strategic postures among incumbent leaders:

-

H.B. Fuller (St. Paul, MN) — Strengths: deep penetration in packaging and nonwovens with branded product families and a recent launch focused on e-commerce packaging. Strategic emphasis: rapid-response product development and sales-led adoption in high-volume channels.

-

Henkel (Düsseldorf) — Strengths: diversified end-market exposure and capacity investments in Europe. Strategic emphasis: industrial-scale production coupled with close OEM partnerships in automotive and assembly segments.

-

Bostik / Arkema (Colombes) — Strengths: innovation in metallocene and hygiene-grade chemistries with a pipeline of speciality hot melts. Strategic emphasis: niche leadership in hygiene and construction adhesives, with sustainability messaging.

-

3M (St. Paul, MN) and Avery Dennison (Mentor, OH) — Strengths: platform breadth across industrial and labeling applications, plus strong IP and distribution reach. Strategic emphasis: premium, specification-driven products and certification-led differentiation.

-

Global polymer suppliers and additive providers (Dow, BASF, Evonik, Huntsman) — Role: upstream innovation partners enabling next-generation formulations, performance additives and supply continuity.

-

Contract manufacturers and private-label players (Texas Eastern Products, Jowat) — Role: agility for smaller OEMs and regional converters, providing cost-effective formulations and private-brand capabilities.

Recent tactical moves underscore where near-term battles will be fought: product launches tailored to e-commerce packaging and hygiene, capacity expansions in strategic geographies, and sustainability-credentialing via certifications. These are signals for 2026 buyers and investors to expect intensified competition on formulation performance and supply reliability, not just price.

Strategic imperatives for 2026

Based on our integrated market model and scenario work, PW Consulting recommends five priority actions for executives making 2026 decisions:

-

Adopt flexible formulations and multi-sourcing frameworks. Design product roadmaps and procurement contracts that allow blenders to substitute resin families with minimal requalification time. Dual-sourcing binders and securing strategic volumes with key additive suppliers reduce single-point risk.

-

Embed regulatory scenario-planning into R&D roadmaps. Allocate explicit R&D bandwidth to REACH- and state-level compliance scenarios. Fast-follower reformulation capability will be cheaper than repeated post-facto recalls or label changes.

-

Price architecture and margin protection. Transition from commodity-based pricing to value-based pricing for differentiated hot melts (e.g., bio-based, low-temp, high-tack variants). Combine index-linked raw-material surcharges with productivity and yield programs to protect margins.

-

Selective capacity strategy. For producers contemplating capex, favor modular, scalable lines and regional mini-hubs over large single-site greenfield projects unless off-take contracts de-risk long-term utilization. Contract manufacturing partnerships can accelerate entry into new geographies.

-

Commercial and go-to-market sharpening. Sales motions must segment customers by adhesive performance needs and switching cost. Invest in application labs and joint-development agreements with top-tier converters and OEMs; winning specification deals in packaging and hygiene unlocks long-term revenue streams.

Report deliverables — what PW Consulting provides

This brief is an executive distillation. The full PW Consulting Hot Melt Glue Market report provides practical, transaction-ready tools designed for 2026 action:

-

Proprietary demand model with annual forecasts and scenario toggles for 2026–2032, including upside/downside cases driven by raw-material shocks and regulatory shifts.

-

Supplier scorecards covering technical capability, sustainability credentials, capacity footprints and commercial terms — benchmarked across global leaders and regional specialists.

-

Segment-level playbooks (By type, By application, By region) that translate market opportunity into sales targets, required product attributes and sample pricing bands — structured to be operationalized by product managers and commercial leaders.

-

Regulatory impact matrix mapping compliance timelines, reformulation levers and cost-to-comply estimates for key jurisdictions.

-

Strategic M&A and partnership framework including target archetypes, valuation heuristics and integration risk checklists for roll-up or bolt-on strategies.

-

Procurement toolkit: hedging templates, indexation clauses and multi-year sourcing strategies aligned to common manufacturing footprints.

To preserve the value of our proprietary models and to adhere to the “trailer” approach, this public brief intentionally omits granular regional and application-level tables and other licensed datasets that are included in the paid report.

How to use this intelligence in 90–180 days

-

90-day actions: stress-test supplier contracts for price-variation and force-majeure exposure; initiate formulation audits against imminent regulatory lists; pilot a dual-sourcing trial for the highest-spend resin component.

-

180-day actions: implement an SKU rationalization based on margin-to-complexity scores; negotiate strategic supply agreements with performance and sustainability KPIs; scope a modular capacity expansion or contract-manufacturing partnership aligned to demand hotspots.

Final perspective — why 2026 is a pivotal year

The hot melt market’s steady growth provides a predictable backdrop, but the combination of raw-material volatility, regulatory tightening and evolving customer sustainability expectations makes 2026 a pivot point: firms that align product portfolios, procurement strategies and commercial models now will capture disproportionate value through 2032. The levers are clear — formulation agility, supplier partnerships, targeted capex and pricing sophistication — but execution requires credible data, scenario plans and operational playbooks. That is precisely the tactical value PW Consulting’s full report delivers.

Next steps

For executive teams preparing 2026 budgets or investors evaluating strategic options, PW Consulting’s full Hot Melt Glue Market report includes the complete datasets, segmented forecasts and actionable templates referenced here. Visit our report page to access the full study, licensing options and bespoke advisory engagements. (Note: segmented tables and detailed regional/application forecasts are available exclusively in the paid report.)

For detailed analysis of this topic, please visit the official page: Hot Melt Glue Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.