PW Consulting Forecast: Phased Array Antenna Module Market to Skyrocket at 17.15% CAGR, Reaching USD 12,769.18 Million by 2032

Phased Array Antenna Module Market: Strategic Imperatives for 2026 — PW Consulting Insights

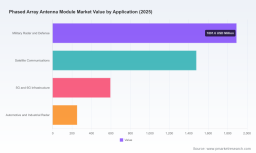

Executive summary

PW Consulting’s latest market intelligence on the Phased Array Antenna Module market sets a clear directional signal for executive teams making budgetary, R&D, and M&A choices in 2026. Our model shows the market expanding from an estimated USD 4,216.65 Million in the 2025 base year to roughly USD 12,769.18 Million by 2032, reflecting a compound annual growth rate of 17.15% over the forecast horizon. That trajectory is driven by accelerating adoption across defense radars, satellite communications, and mobile infrastructure coupled with rapid component-level innovation (notably GaN-on-Silicon RF solutions) and growing demand for compact, electronically steerable antennas for mobile and enterprise connectivity.

Phased Array Antenna Module Market

Why this report matters for 2026 decisions

Leaders face competing pressures: accelerate product roadmaps to capture emerging 5G/6G and LEO/MEO satellite opportunities, while simultaneously hardening supply chains and navigating export controls. The market’s high-growth profile creates both high-reward opportunities and high operational risk within a relatively concentrated supplier landscape—our analysis shows the top three firms control roughly 43% of market revenue and the top five nearly 59%—making strategic partner selection and capability investments particularly consequential.

Phased Array Antenna Module Market

What PW Consulting’s report delivers (practical, operationally focused)

- Actionable market sizing and scenario modeling: Base-year calibration (2025) and three-tier scenario forecasts (conservative, base, upside) through 2032 to quantify timing and magnitude of addressable demand under alternative macroeconomic and geopolitical pathways.

- Technology roadmaps and adoption curves: Comparative analysis of active versus passive phased array approaches, millimeter-wave modules for SATCOM/5G, and the implications of GaN-on-Silicon and advanced beamformer IC adoption on cost, size, and power budgets.

- Supply-chain resilience playbook: A mapped supplier ecosystem for RFICs, T/R modules, substrates and packaging, with supplier risk scores, critical single points of failure, and mitigation options including dual-sourcing and near-shoring scenarios.

- Go-to-market and product positioning frameworks: Segmented buyer personas (defense primes, satellite ISPs, telecom integrators, automotive OEMs), procurement timelines, and a pricing/value communication matrix to support commercial negotiations.

- M&A and partnership diligence pack: Financial and technical red-flags for targets, integration heatmaps for capabilities (RF front end, beamforming, digital signal processing, thermal management), and a valuation sensitivity model reflecting technology obsolescence and export-control exposure.

- Regulatory impact assessment: Practical guidance on ITAR/EAR exposure, export licensing strategies, and compliance-driven manufacturing and data partitioning approaches to preserve market access.

- Test, qualification, and manufacturability diagnostics: KPI checklists for production ramp (DFM/DFT readiness), thermal testing protocols for high-density T/R modules, and recommended third-party test labs aligned to customer acceptance criteria.

Competitive landscape — who matters and why

The market is shaped by strong incumbents and a vibrant set of specialized innovators. U.S.-based defense primes continue to dominate high-end defense radar and surveillance systems, while specialized suppliers and semiconductor companies enable commercial SATCOM and telecom deployments. Key strategic positions to watch include:

Phased Array Antenna Module Market

- Raytheon Technologies (RTX) — a leader in large-scale AESA architectures for naval and enterprise air surveillance. Recent contract awards, including a significant U.S. Navy production modification announced in January 2026, underscore continued defense procurement momentum and important unit-cost reduction trajectories enabled by modular designs.

- Northrop Grumman — focused on integrated AESA and digital beamforming for next-generation long-range radar; completion of a major critical design review in late 2025 illustrates progress toward fielding ambitious ground-based systems.

- L3Harris, BAE Systems, Lockheed Martin, Leonardo — these firms offer scaled platforms and multi-domain phased array capabilities that position them as go-to integrators for defense and security customers.

- Analog Devices and Qorvo — critical enablers at the component level, supplying beamformer ICs, GaN T/R chipsets, and RF front-end building blocks that determine unit cost, bandwidth and thermal performance across module categories.

- Specialists and new entrants (Kymeta, Viasat, Sivers, Requtech, C-COM, ALCAN, Kyocera) — they are accelerating commercialization of electronically steerable flat-panel arrays, millimeter-wave modules, and conformal antenna concepts that challenge traditional form factors in SATCOM and mobile broadband markets.

Recent market signals reinforce both demand and competitive dynamics: Kymeta’s January 2026 launch of an enhanced electronically steerable mobile SATCOM antenna highlights commercial momentum in high-throughput mobile broadband; C-COM’s late-stage development progress in February 2026 signals continued R&D investment in flat-panel Ka-band architectures; and Sivers’ 2025 announcements underscored rapid millimeter-wave product development relevant to 5G/6G and SATCOM. Together, these moves show incumbents defending systems business while specialists attack commercial niches.

Key market forces and risks shaping 2026 strategy

- Export controls and geopolitical friction: ITAR/EAR constraints and U.S.-China tensions materially affect market access, partner selection, and supply routing. Companies must balance growth ambitions against compliance and potential market exclusions.

- Semiconductor and raw-material fragility: Dependence on GaN, GaAs, and specialized RFIC supply chains creates exposure to capacity bottlenecks and tariff-driven cost pressure. Strategic procurement, inventory hedging, and long-term offtake contracts are high-priority levers.

- Technology-driven miniaturization: Adoption of GaN-on-Silicon and advanced integration reduces size, increases power density, and shifts value capture toward component suppliers and system integrators who master thermal and signal integrity challenges.

- Concentration dynamics: Moderate concentration at the top of the market means new entrants face a high bar for scale, but niche differentiation—e.g., low-latency LEO tracking, conformal arrays, or cost-for-performance optimized modules—remains a viable route to commercialization.

Strategic playbook for executives in 2026

Based on cross-functional analysis and scenario modeling, PW Consulting recommends a prioritized set of moves for 2026:

- De-risk supply chains now: Lock in multi-year supply agreements for GaN and beamformer ICs, qualify secondary fabs, and evaluate near-shore assembly to mitigate tariff and logistical volatility.

- Move from components to systems-enabled services: Capture aftermarket and lifecycle revenue by packaging software-defined beamforming features, OTA update services, and managed SATCOM offerings alongside hardware sales.

- Invest selectively in GaN and thermal management: Target engineering investments that reduce per-element cost and improve power efficiency—these yield outsized gains in both defense procurement competitions and commercial SATCOM offerings.

- Pursue focused M&A and partnerships: Prioritize bolt-on targets that provide missing IP in beamforming, low-profile flat-panel antennas, or in-country assembly to navigate export constraints and accelerate market access.

- Adopt compliance-first international expansion: Design market-entry playbooks that integrate export licensing, data partitioning, and local partner structures to minimize regulatory shocks.

How buyers and investors should use this report

Procurement leaders can use our procurement timing matrices and supplier risk scores to optimize purchase windows and negotiate better terms. R&D leaders will find the technology adoption timelines and component cost curves invaluable for prioritizing projects with the highest ROI. Investors and corporate development teams can leverage our valuation sensitivity model and M&A diligence checklist to spot targets whose value is under- or over-stated given export risk and semiconductor access.

What we intentionally withhold here — and why

This release is designed as a strategic “trailer.” We surface the directional market sizing, growth rates, consolidation dynamics and concrete strategic implications, but we withhold detailed segmentation breakout data and proprietary scenario spreadsheets that underpin our target recommendations. Those detailed datasets—segment-level demand curves, regional revenue splits, customer price elasticity matrices, and vendor-level financial adjustments—are included in the full PW Consulting report and accompanying data workbook available via our subscription channels.

Next steps

For leadership teams preparing 2026 budgets, supply-chain contingency plans, or M&A pipelines, the full report provides the executable intelligence needed to convert market growth into competitive advantage. Contact PW Consulting to access the complete research package, the data workbook, and a tailored executive briefing that maps our findings directly to your organization’s strategy and risk profile.

For detailed analysis of this topic, please visit the official page: Phased Array Antenna Module Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.