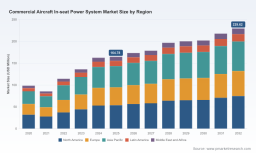

PW Consulting Forecasts Commercial Aircraft In‑Seat Power Market to Grow from USD 164.78 Million in 2025 to USD 229.62 Million by 2032 at a 4.85% CAGR

Commercial Aircraft In-Seat Power Systems Market: Strategic Intelligence for 2026 Decision-Makers

PW Consulting today publishes an executive briefing accompanying our full Commercial Aircraft In-Seat Power System Market report (base year 2025). The companion analysis synthesizes market sizing, supplier dynamics, regulatory drivers and actionable decision frameworks that procurement, product and fleet-planning teams need to make defensible investments in 2026. Our macro findings: the global in-seat power market reached approximately USD 164.8 Million in 2025 and is forecast to grow at a 4.85% CAGR through our 2026–2032 projection horizon, reaching roughly USD 229.6 Million by 2032. These headline metrics frame the commercial logic; the full report provides the granular scenarios, competitive scorecards and supplier playbooks required to convert intent into outcomes.

Commercial Aircraft In Seat Power System Market

Why this intelligence matters in 2026

-

Time-sensitive procurement windows — With OEMs and retrofit cycles aligning to narrowbody and widebody refreshes in many fleets, procurement teams face trade-offs between linefit upgrades versus staged retrofits. Selecting the wrong migration path can lock operators into suboptimal weight, power and certification profiles for an entire fleet sector.

Commercial Aircraft In Seat Power System Market -

Regulatory inflection points — The industry is coalescing around universal USB‑C standards and higher wattage delivery to support 60–100W device charging. Decisions made now will determine compliance costs, certification timelines and long-term passenger experience differentiation.

Commercial Aircraft In Seat Power System Market -

Supply chain and design constraints — Raw material dynamics and fuel-efficiency mandates are reshaping engineering choices. Constraints on high-grade copper and mandates for slimmer, lighter power converters mean hardware choices now affect wiring architecture, aircraft weight and cabin space for years to come.

-

Competitive concentration — Market structure is moderately concentrated: the leading three suppliers command a substantial share of installed bases, and the top five firms capture an even larger portion of market activity. This concentration affects negotiation leverage, aftermarket support options and the pace of technology diffusion.

What the PW Consulting report delivers — practical content mapped to execution

-

Market sizing and scenario modeling: A defensible baseline market size (base year 2025) and three forecast scenarios through 2032 that stress-test assumptions about device power demand, retrofit rates and new-build penetration.

-

Procurement playbook: Step-by-step sourcing templates for RFIs/RFPs, evaluation matrices that weight certification risk, TCO, modularity and support contracts, and negotiation levers we’ve validated with airline and OEM partners.

-

Retrofit vs. linefit decision framework: A practical decision tree incorporating downtime costs, installation labor profiles, electrical rework scopes and passenger experience uplift modeling to justify capital allocation.

-

Supplier benchmarking and scorecards: Comparative assessments of product families across key dimensions — power density, certification status, modularity, mean-time-between-failure, and aftermarket service footprints — without disclosing proprietary vendor revenue breakdowns.

-

Certification and regulatory checklist: Task-level guidance for meeting evolving USB‑C standards, EMI/EMC constraints and lightweight design mandates — including likely certification timelines and critical path items.

-

Supply chain risk assessment: Scenario-based mitigation plans for raw-material shortages and single-source dependencies, and engineering responses such as adoption of higher-voltage distribution networks that reduce conductive-material usage.

-

Commercial models and TCO templates: CapEx/Opex modeling templates for fleet planners and finance teams to evaluate payback windows under multiple charging-usage profiles and maintenance cost assumptions.

Competitive landscape: who to watch and how to align

The in-seat power ecosystem blends established avionics suppliers, specialized enablers and vertically integrated cabin-systems players. Our report profiles core suppliers and synthesizes their strategic posture as of 2026, helping buyers judge which partners best fit a chosen route-to-market — whether linefit integration with OEMs, aftermarket retrofits or bundled IFE + power offerings.

-

Astronics Corporation (East Aurora, NY) — A market leader with a broad installed base and mature EmPower product family. Recent product launches reinforce a focus on high-power USB‑C outlets and dual-port options designed for both retrofit and linefit. Astronics’ combination of certified hardware and award-winning product iterations makes it a default consideration for operators prioritizing proven reliability and certification readiness.

-

KID-Systeme GmbH (Buxtehude, Germany) — A specialist with strengths in cabin electronics and system integration for passenger and corporate aircraft. Their value proposition centers on innovation in seat-level integration and adaptability for differentiated cabin architectures.

-

Collins Aerospace (RTX, Charlotte, NC) — Integrates power and data ports within broader seating and IFE ecosystems. Collins positions itself as a systems integrator that can streamline supplier interfaces for OEMs and airlines seeking turnkey cabin solutions.

-

Burrana Pty Ltd (Cannon Hill, QLD) — Leverages its RISE cabin technology to position in-seat power as part of a broader cabin modernization play, targeting narrowbody refurbishments where integrated digital-cabin architectures deliver higher passenger perceived value.

-

IFPL Group Ltd (Isle of Wight, UK) — A high-volume supplier of in-seat power modules and interfaces with deep aftermarket reach. IFPL’s long history and extensive unit shipments make it a strong candidate for operators prioritizing supply continuity and unit-level cost advantages.

-

Mid-Continent Instrument Co. / True Blue Power (Wichita, KS) — Focused on certified USB power systems and chargers, offering TSO-certified solutions attractive to operators focused on rigorous compliance and cockpit/cabin safety standards.

-

Panasonic Avionics (Lake Forest, CA) — Bundles high-power USB‑C delivery within its Astrova IFE platform; operators aiming for an integrated passenger entertainment and power experience should evaluate the trade-offs between bundled systems and best-of-breed component selection.

-

Astrodyne TDI (Hackettstown, NJ) — Supplies custom power modules and EMI filters that increasingly matter as operators pursue lighter, higher-density power architectures.

Notable recent developments underline the market’s technological momentum: Astronics launched a dual USB‑C outlet in 2026; Burrana elevated its RISE in-seat offering at AIX 2026; IFPL celebrated three decades and showcased new modules; and Panasonic’s Astrova deployments with high-wattage USB‑C entered commercial service. These product and market moves accelerate standardization and increase pressure on lagging suppliers to update portfolios or partner to remain competitive.

Regulatory and technical dynamics shaping strategy

-

USB‑C standardization is not merely convenience — it is a sourcing and certification pivot. Operators must decide whether to mandate universal USB‑C across new-builds and retrofits now, or to accept a phased conversion with increased spares complexity and customer inconsistency.

-

Raw-material constraints (notably on high-grade copper) are driving system architects toward higher-voltage distribution topologies that reduce conductor mass by an estimated margin. That shift has implications for converter placement, thermal management and certification effort.

-

BYOD consumer behavior has made basic seat power an operational baseline rather than a premium amenity. Suppliers and airlines must therefore separate “table stakes” power delivery from premium differentiated services (e.g., guaranteed 60–100W ports, managed power allocation, or subscription-based fast-charging access).

-

Fuel efficiency and slimline design mandates require power converters and modules to occupy less cavity space and weigh less — design constraints that favor suppliers investing in high power-density, low-profile architectures.

How to use this report in 90 days

-

Procurement teams: Adapt our RFP template, run a short-list evaluation against the supplier scorecard, and secure a trial installation on a pre-selected aircraft within 60–90 days to validate integration assumptions.

-

Engineering leads: Use the TCO and wiring-architecture scenarios to determine whether a high-voltage distribution migration yields net weight and cost benefits across the fleet within a 5–7 year horizon.

-

Commercial leaders: Quantify passenger experience uplift versus incremental cost and decide on a uniform USB‑C policy for new-builds versus selective retrofit rollouts to optimize ancillary revenue and NPS impact.

Conclusion — strategic value proposition

For executives and practitioners planning capital allocation, vendor selection or cabin modernization roadmaps in 2026, the PW Consulting Commercial Aircraft In-Seat Power System Market report delivers the synthesis required to act with confidence. It pairs headline market sizing and a validated CAGR with operationally focused tools — procurement templates, certification checklists, supplier scorecards and risk-mitigation playbooks — so that decisions made in 2026 align to the technology, regulatory and supply-chain realities that will define fleet competitiveness through 2032.

To access the complete dataset, vendor scorecards and downloadable decision-support templates that underpin this briefing, please consult the full report on our website. The headline intelligence above is intended to orient your 2026 strategy; the full report contains the granular analyses that will convert strategy into executable programs.

For detailed analysis of this topic, please visit the official page: Commercial Aircraft In Seat Power System Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.