PW Consulting: Cerebrovascular Accident Drug Market Expected to Grow at a 6.45% CAGR, New Insight Reveals

Cerebrovascular Accident Drug Market — 2026 Strategic Outlook and PW Consulting Executive Summary

Executive snapshot

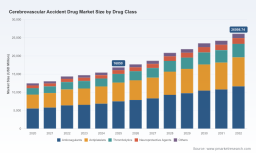

PW Consulting’s latest Cerebrovascular Accident Drug Market report synthesizes clinical, commercial, regulatory and supply-side intelligence to inform corporate decision-making across 2026 and beyond. The market is on a sustained upward trajectory: using 2025 as the base year, our model projects a compound annual growth rate (CAGR) of 6.45% across the 2026–2032 forecast period. This trajectory reflects both near-term adoption shifts in acute ischemic stroke management and medium-term changes from novel secondary-prevention therapies. For leaders needing an evidence-based roadmap for product launches, portfolio prioritization, M&A screening and market-access planning in 2026, the report translates these macro trends into actionable choices.

Cerebrovascular Accident Drug Market

What the report delivers — practical, transaction-ready insights

- Concise market sizing and high-confidence forecasts anchored to an updated 2025 base year and mid-range scenarios across 2026–2032, with sensitivity bands for low/high clinical adoption and pricing pressure.

- Commercialization playbooks for acute thrombolytics and next-generation anticoagulants: channel strategies, hospital procurement touchpoints, emergency department adoption drivers, and key payer levers to secure formulary status.

- Regulatory and guideline impact analysis — mapping how recent approvals and guideline updates translate into addressable patient populations, reimbursement timelines and likely adoption curves in major markets.

- Clinical development prioritization frameworks for R&D and BD teams, including go/no-go triggers, comparator-selection guidance and pragmatic trial designs to accelerate market differentiation.

- Manufacturing and supply-chain due diligence, with particular emphasis on biologic tPA variants and the operational constraints that affect time-sensitive acute-care therapies.

- Deal-clinic templates: valuation sensitivities, royalty/earn-out structures, and M&A screening criteria tailored to high-impact asset classes (thrombolytics, Factor XIa inhibitors, neuroprotectives).

- Real-world evidence (RWE) playbook and HTA positioning: which endpoints, registries and economic models move the needle for payers and hospital systems.

Market dynamics: the levers behind the 6.45% CAGR

Our analysis identifies three structural drivers underpinning market growth. First, recent regulatory and guideline changes have materially altered the acute-treatment landscape, which in turn affects short-term uptake and hospital inventory planning. Second, the advance of Factor XIa inhibitors and other next-generation anticoagulants is reshaping secondary-prevention strategies, creating a wave of prescribing shifts over the medium term. Third, demographic and care-pathway trends — including expanded imaging-based thrombectomy windows — continue to increase the pool of patients eligible for reperfusion and secondary-prevention interventions.

Cerebrovascular Accident Drug Market

These dynamics create both upside (faster-than-expected adoption of new agents) and downside (pricing pressure, hospital budget constraints). The report’s scenario suite quantifies those trade-offs so executive teams can stress-test market-entry and investment plans against plausible clinical and payer outcomes.

Cerebrovascular Accident Drug Market

Competitive landscape — strategic implications for incumbents and challengers

- Genentech (Roche Group)

Genentech’s March 2025 FDA approval of TNKase (tenecteplase) as a single-bolus therapy for acute ischemic stroke is a clear inflection point. The approval shortens administration time in emergency settings and aligns with guideline shifts endorsing tenecteplase as an alternative to alteplase. For Genentech, the tactical priorities are rapid ED education, stroke-network contracting, and securing early-adopter centers to lock in treatment pathways where single-bolus workflow advantages are most salient. - Boehringer Ingelheim

As a long-standing supplier of thrombolytics outside certain markets, Boehringer’s strengths lie in global supply relationships and established clinical trust. The company will likely defend market access through lifecycle activities and hospital partnerships where alteplase remains entrenched. - Bristol Myers Squibb & Janssen / Johnson & Johnson

The late-stage clinical programs for milvexian (Factor XIa inhibitor) position these groups at the center of secondary-prevention innovation. Success in Phase 3 and regulatory filings would translate into portfolio-shaping opportunities for cross-sell with antiplatelet agents and differentiated post-stroke prevention regimens. Strategic alliances, label differentiation and payer dossiers will determine realized value. - Bayer

Bayer’s positive OCEANIC-STROKE Phase 3 readout (asundexian plus antiplatelet) in late 2025 signals competitive pressure on incumbent regimens for recurrent ischemic stroke prevention. Bayer faces the commercial task of integrating fixed-dose strategies and co-prescribing messaging into cardiology and neurology pathways. - Other multinational portfolios (Pfizer, AstraZeneca, Sanofi, Daiichi Sankyo, Novartis)

These companies retain diverse playbooks — from antiplatelet/anticoagulant offerings to integrated cardiovascular franchises — and will compete through bundle positioning, hospital-level contracting and therapeutic differentiation supported by RWE.

Collectively, the market’s top-tier players maintain a concentrated footprint that creates high entry barriers for smaller challengers but also opens opportunities for niche innovation and targeted licensing. New approvals and positive Phase 3 results accelerate transition windows; incumbents must decide between defensive lifecycle investments and selective footprint expansion into adjacent prevention niches.

Regulatory, guideline and reimbursement context

Two regulatory and guideline developments deserve strategic emphasis. First, the FDA’s approval of tenecteplase for acute ischemic stroke in March 2025 eliminated a long-standing label gap — a change that unlocks single-bolus workflows and may shift hospital protocol adoption curves. Second, the 2026 Acute Ischemic Stroke Guideline update endorses tenecteplase and extends imaging-based thrombectomy eligibility, altering the effective addressable population for acute therapies.

From a reimbursement standpoint, thrombolytics remain embedded within established hospital reimbursement frameworks in major markets; however, pricing pressure and bundled-emergency-care models mean that manufacturers must demonstrate either clear clinical/cost offsets (e.g., reduced length of stay, fewer complications) or secure hospital-level pathway adoption via outcomes-linked agreements. For secondary-prevention agents, HTA dossiers will hinge on absolute risk reduction and cost-effectiveness versus standard antiplatelet regimens — areas where robust RWE and well-designed economic models will materially influence formulary outcomes.

Operational considerations: biologics manufacturing and supply resilience

Thrombolytic agents that rely on recombinant tPA manufacturing present distinct supply-chain and scale-up risks. Biologic production capacity, cold-chain logistics and single-dose presentation choices all affect total cost of ownership for hospitals and payers. Our report provides a manufacturing risk matrix and supplier due-diligence checklist that procurement and manufacturing leaders can use immediately when evaluating capacity expansions, contract manufacturers or contingency inventories in 2026.

Strategic playbook for 2026 — five priority moves

- Launch readiness: Prioritize emergency-department and stroke-network pilots that demonstrate workflow efficiency gains (time-to-treatment, staff burden reduction) — these operational endpoints are persuasive to hospital procurement committees.

- Payer and HTA engagement: Build economic models now that incorporate the 2026 guideline context and thrombectomy-window expansion to pre-empt payer objections and support value-based contracting.

- RWE and registry investment: Commit to multicenter registries that capture functional outcomes and health-economic endpoints within 12–18 months of launch to accelerate reimbursement wins.

- Manufacturing de-risking: Secure redundant biologic capacity and validate cold-chain partners; consider vial/pen presentations and single-bolus formats that reduce administration complexity.

- Portfolio and BD discipline: Use the report’s deal-screening framework to prioritize partnerships and M&A targets that either close clinical gaps (e.g., neuroprotective adjuncts) or provide scale in hospital procurement channels.

Why PW Consulting’s report matters for 2026 decision-makers

Our report is built to translate complex, fast-moving clinical and regulatory developments into executable commercial and financial decisions. It pairs rigorous market models (with sensitivity analyses anchored to the 6.45% CAGR baseline) with operational playbooks, payer-engagement templates and due-diligence tools ready to use in board-level deliberations. Importantly, while this summary outlines strategic direction and company-level implications, the full report contains the granular segmentation, hospital workflow models, and downloadable data tables necessary for transaction execution and internal financial modeling.

Next steps

Leaders planning launches, negotiating partnerships or evaluating M&A opportunities in 2026 should use the report as the single source of truth for market sizing, adoption scenarios and operational risk. PW Consulting is offering tailored briefings and custom modelling workshops to translate the report’s insights into client-specific go-to-market and investment blueprints. For access to the full dataset, segment-level analysis and the complete set of vendor and partner scoring tools, please visit our report page.

For detailed analysis of this topic, please visit the official page: Cerebrovascular Accident Drug Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.