PW Consulting: Lowdk Glass Fiber Cloth Market Set for 8.15% CAGR During 2026–2032

Lowdk Glass Fiber Cloth Market: Strategic Imperatives for 2026 — PW Consulting Advance Brief

PW Consulting’s latest industry briefing on the Lowdk Glass Fiber Cloth market synthesizes five years of historical trends (2020–2025) and delivers a forward-looking forecast through 2032. The market’s structural momentum — underpinned by AI-driven demand for high-frequency, low-loss substrates — presents a compelling growth opportunity for executives planning investments, capacity moves, M&A, and go‑to‑market strategies in 2026. Below we summarize the strategic takeaways and the reasons why the full report should be a required input into board- and strategy-level decision-making this year.

Lowdk Glass Fiber Cloth Market

Market Trajectory: Macro Picture and Growth Dynamics

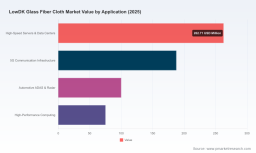

Our model (base year 2025) shows the Lowdk Glass Fiber Cloth market has entered a sustained growth phase. After passing an estimated USD 625.5 Million in 2025, the market is projected to expand at a compound annual growth rate of approximately 8.15% across the 2026–2032 forecast window, reaching an anticipated USD 1,082.5 Million by 2032. The dataset includes a consistent historical series (2020–2025) and a granular, scenario-based projection for 2026–2032 that incorporates demand pull from AI servers, 5G infrastructure, and next‑generation automotive radar and IC packaging.

Lowdk Glass Fiber Cloth Market

Two structural forces drive the growth profile: (1) product substitution toward ultra-low dielectric materials in high-speed digital and RF applications, and (2) a concentration effect where a relatively small set of specialized suppliers capture a disproportionate share of advanced-spec demand. Our concentration analysis indicates the market is moderately consolidated at the top: the leading three suppliers account for a majority share, and the top five capture an even larger portion of advanced product supply — important context for supply risk and competitive positioning.

Lowdk Glass Fiber Cloth Market

Why This Report Matters for 2026 Decisions

- Capital allocation and timing: With mid‑to‑high single-digit CAGR and pronounced short‑term supply tightness in advanced low‑Dk and low‑CTE materials, the timing of capacity investments materially affects return on invested capital. The report’s capital‑project stress-tests and lead‑time scenarios enable CFOs and investment committees to compare accelerated vs. staged expansions under practical price and yield assumptions.

- Supply‑chain risk management: Supplier concentration and regional exposure create geopolitical and operational risk. Our risk matrix quantifies exposure by supplier tier and proposes mitigation levers — dual sourcing, strategic inventory, and supplier co-investment — that materially reduce disruption odds for a 2026 product ramp.

- Pricing and margin modeling: ASP differentials between commodity E‑glass and advanced low‑Dk varieties are substantial. The report includes margin waterfall analyses for NE‑glass, NER‑glass and ultra‑low‑loss grades that help commercial teams set premiums while preserving share in volume-sensitive accounts.

- Go‑to‑market and channel design: As demand moves from commodity laminates to engineered cloths for IC substrates, manufacturers must evaluate direct OEM engagement versus distributor-led models. Our sales motion playbooks are tailored to both incumbent fabricators and new entrants pursuing high-margin IC substrate segments.

Practical Contents — What the Report Provides (Operational, Not Just Theoretical)

- Proprietary demand model (2020–2032) with scenario toggles for AI server intensity, 5G capex cycles, and automotive electrification uptake.

- Supply‑side capacity mapping and lead‑time sensitivity analysis that isolates critical bottlenecks through mid‑2027.

- Price and cost benchmarking with margin impact models across glass types and fabric constructions (commercially actionable ASP and cost drivers are included in the full report).

- Strategic playbooks for capacity expansions, joint ventures, technology licensing, and geographic diversification—each with a pragmatic implementation roadmap and KPI templates.

- M&A playbook focused on bolt‑on targets and technology acquisitions, including valuation templates that reconcile current multiples to projected demand profiles.

- Supplier due‑diligence checklists and an RFP template for procurement teams evaluating advanced low‑Dk material partners.

Note: In keeping with PW Consulting’s “preview” approach, detailed segment tables, site‑level capacity numbers, and client‑ready Excel modules are intentionally omitted from this brief. Access to the full dataset and interactive models is available through the complete report.

Competitive Landscape — Who Matters and Why

The advanced Lowdk Fabric market is shaped by a mix of integrated incumbents, specialty fiber producers, and agile regional fabricators. Key strategic players we profile in the report include longstanding integrated manufacturers that control upstream glass production and newer, nimble firms expanding capacity in demand regions. Recent strategic moves underscore shifting power dynamics:

- Integrated Japanese and Taiwanese suppliers continue to set technical benchmarks for ultra‑low dielectric and low‑CTE offerings; they hold a sizeable portion of advanced specs and maintain preferential relationships with high‑end PCB and IC substrate producers.

- North American specialty fiber producers are investing to secure local supply for on‑shore semiconductor and AI server demand, narrowing geographic risk and shortening lead times for regional customers.

- Regional fabricators and weavers, through partnerships and local capacity expansions, are capturing read‑to‑laminate demand in fast-growing production corridors.

Strategic implications: incumbents benefit from vertical integration and technical moats but are exposed to raw‑material supply constraints and price volatility. New entrants and incumbent fabricators can win commercial traction by optimizing lead times, developing close OEM partnerships, and differentiating on process yields rather than raw material cost alone.

Industry Signals and Recent Developments — What To Watch in 2026

- Price normalization is unlikely in the short term. Leading material suppliers implemented sizeable premium adjustments in 2025 and signaled additional increases in early 2026 amid tightness in advanced yarn supply. Businesses that assume stable ASPs risk margin compression when launching new product lines.

- Capacity expansion announcements and strategic partnerships are accelerating, particularly in North America and select APAC locations. These moves are intended to support semiconductor and AI server ecosystems and to reduce regional supply exposure.

- Lead times for advanced low‑Dk and low‑CTE fabrics remain extended and are expected to persist until mid‑2027 unless incremental brownfield capacity is commissioned faster than currently signaled.

- Order‑of‑magnitude price differentials between commodity glass and advanced low‑Dk glass mean product selection and qualification timelines will materially affect TCO for OEMs moving to next‑generation boards and substrates.

- Geopolitical dynamics and supply concentration in Taiwan and Japan continue to influence corporate decisions around localization and redundancy; manufacturers are evaluating southward CCL strategies and cross‑border collaborations to de‑risk supply chains.

Actionable Strategic Recommendations for 2026

- Prioritize secure supply pathways: Enter multi‑year purchase agreements with tier‑1 suppliers or structure co‑investment arrangements to lock in capacities and preferential lead times. For firms unable to secure long‑term allocations, plan for strategic inventory buffers calibrated against cost of capital and product shelf life.

- Stage capacity investments: Use a staggered investment profile with milestone‑based capital release. This reduces exposure to short‑cycle ASP volatility while preserving market access as demand materializes.

- Accelerate qualification timelines: Parallelize materials qualification with system integration workstreams to shorten time‑to‑revenue for new builds. The report includes a practical 9–12 month qualification checklist that can be executed by small cross‑functional teams.

- Leverage partnerships for speed: Consider technology partnerships or toll‑manufacturing arrangements with established weavers to gain fast access to low‑Dk fabrics without upfront plant risk.

- Hedge through product differentiation: Move up the value chain by developing fabric constructions and resin integrations tailored for high‑value applications (e.g., AI server interposers, high‑frequency CCLs) where ASP premiums and margin sustainability are highest.

- Embed geopolitical scenario planning: Maintain at least two qualified supply sources across political geographies for critical grades and develop contingency plans for southward shifts in CCL and fabrication footprints.

Concluding Note — Where PW Consulting Adds Immediate Value

For 2026, the Lowdk Glass Fiber Cloth market will reward surgical strategic moves: well‑timed investments, supplier certainty, and product differentiation. PW Consulting’s full report provides the operational playbooks, quantitative models, and supplier insights needed to translate market growth into durable competitive advantage. This brief is intentionally selective — the full deliverable contains the data‑rich modules, scenario analyses, and executable templates that boards and executive teams need to move from strategy to implementation.

To obtain the complete dataset, granular segmentation tables, and the interactive financial model referenced in this brief, please consult the full PW Consulting report or contact our industry advisory team for a tailored briefing.

For detailed analysis of this topic, please visit the official page: Lowdk Glass Fiber Cloth Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.