PW Consulting: Aerospace Aircraft Stainless Steel Market Tops USD 2,734.08 Million in 2025, Signaling Strong Upside

PW Consulting Releases Strategic Brief: Aerospace Aircraft Stainless Steel Market — A 2026 Decision-Maker’s Playbook

As aerospace supply chains enter a new phase of structural transformation, PW Consulting today publishes an executive-grade industry briefing derived from our full "Aerospace Aircraft Stainless Steel Market" research. Built on a base year of 2025 and delivering forward-looking analysis across 2026–2032, this briefing translates market-scale dynamics into executable guidance for procurement chiefs, materials engineers, and corporate strategists preparing decisions in 2026.

Aerospace Aircraft Stainless Steel Market

Why this report matters for 2026

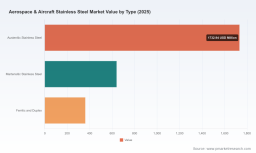

The global aerospace stainless steel market reached a substantive scale in 2025 (base year) and is on a sustained growth trajectory through the forecast window. Our topline modelling foresees steady expansion driven by fleet renewal, rising defense spending in select markets, and substitution dynamics where stainless grades compete with advanced alloys and composites. The 2026–2032 compound annual growth rate (CAGR) underpinning our scenarios is 5.45%, reinforcing the thesis that materials strategy will remain a core enabler of competitive aircraft programs.

Aerospace Aircraft Stainless Steel Market

For executives making sourcing, product development, or M&A decisions in 2026, three simple facts emerge from the numbers: the market is sizable and growing; cost volatility and regulation will be primary drivers of near-term margin pressure; and supplier selection will materially affect program risk and time-to-market.

Aerospace Aircraft Stainless Steel Market

What the full report delivers (practical, decision-ready content)

- Actionable executive summary mapping immediate 12–18 month strategic choices to medium-term portfolio outcomes.

- Topline market sizing and scenario modelling that translates macro drivers into spend trajectories and sensitivity runs for commodity price shocks.

- Supply-side heatmaps: capacity, lead-time risk, and single-source exposure across stainless grades used in aircraft applications.

- Procurement playbook: hedging options, contractual clauses for alloy price pass-through, collaborative product development templates with suppliers, and inventory strategies tuned to aerospace lead times.

- Engineering-cost workstreams: cost-to-manufacture breakdowns by stainless family, alloy substitution matrices, and guidance on qualification paths to accelerate new-material adoption.

- Regulatory and carbon-impact modelling that quantifies the profit-and-cost implications of emerging regimes (including EU carbon mechanisms and U.S. trade measures).

- Competitive supplier scorecards and an M&A watchlist focused on strategic tuck-ins, capacity expansion targets, and value-accretive vertical plays.

- Scenario-based risk register and mitigation playbooks for supply-disruption, raw-material shock, and policy shifts affecting cross-border flows.

Competitive landscape — who matters and why

The aerospace stainless steel value chain is shaped by a mix of global producers, specialist distributors, and precision fabricators. Our analysis highlights several players whose strategic decisions and investments are likely to shape market structure over the coming 24 months:

- Outokumpu (Helsinki, Finland) — https://www.outokumpu.com A global stainless producer with tailored alloys that meet the stringency of aerospace certifications. Their material technology and scale make them a partner of choice for OEMs seeking high-temperature and corrosion-resistant solutions.

- Service Steel Aerospace (Fife, WA, USA) — https://www.ssa-corp.com A leading aerospace-focused distributor with an expanding footprint; recent capacity investments enhance regional fulfillment and reduce lead-time exposure for U.S.-based programs.

- Universal Stainless (Bridgeville, PA, USA) — https://www.univstainless.com Specializes in aircraft-grade stainless and nickel alloys used in structural and engine applications; their production footprint supports qualification timelines critical to OEM programs.

- Carpenter Technology (Reading, PA, USA) — https://www.carpentertechnology.com Known for high-performance specialty alloys tailored for extreme operational envelopes—an important supplier where substitution away from titanium or nickel-based alloys is considered.

- BUTTING (Knesebeck, Germany) — https://www.butting.com A precision manufacturer of tubes and assemblies; its capability to deliver ready-to-install components reduces downstream integration risk for airframe suppliers.

- Continental Steel & Tube Co. (Fort Lauderdale, FL, USA) — https://www.continentalsteel.com Distributor with a broad product slate supporting diverse aircraft applications, valuable for buyers prioritizing logistics agility.

- Future Metals (Tamarac, FL, USA) — https://futuremetals.com Provides industry-standard forms and custom blanks; their supply chain flexibility is relevant to tier-2/3 fabricators pursuing rapid turn prototypes or low-volume production runs.

Our competitive mapping combines publicly available corporate disclosures, recent facility investments, and proprietary supplier assessments to score each firm across capability, geographic reach, certification depth, and supply-risk exposure. The full report includes anonymized benchmarking templates you can deploy immediately with incumbent suppliers.

Recent developments and why they matter for 2026 strategy

- Service Steel Aerospace completed a notable facility expansion in late 2025, increasing distribution capacity and improving regional responsiveness—an example of tactical capacity investments that materially shorten procurement cycles for U.S.-based programs.

- Industry trade-show activity in late 2025 signalled renewed supplier focus on aerospace-grade stainless solutions, with several vendors showcasing process and finishing capabilities that reduce downstream qualification pain.

- New production and advanced manufacturing center builds for stainless and alloy components will create pockets of incremental capacity — an opportunity for buyers to secure long-term offtake at favorable terms if negotiations begin in 2026.

Policy, commodity, and supply risks that will shape 2026

Material procurement in 2026 cannot be considered in isolation from policy and raw-material swings. Key inputs to our risk models include:

- Carbon regulation: The entry into the payment phase of the EU Carbon Border Adjustment Mechanism (CBAM) in 2026 introduces an added cost vector for imported stainless components, changing landed-cost calculus for European buyers and their global suppliers.

- Tariff environment: U.S. Section 232 measures remain in place as of April 2026, maintaining elevated trade frictions that continue to favor localized supply or tariff-mitigation strategies such as bonded inventories and tariff engineering.

- Raw material pressure: Stainless pricing in North America has experienced upward pressure (price points observed in early 2026), driven by rises in nickel, chromium, and ferroalloys. Notably, nickel can constitute up to 70% of the variable cost input for certain austenitic stainless productions — a dominant cost sensitivity captured in our stress-testing.

- Geopolitical industrial policy: National strategies—such as China’s emphasis on high-tech and aerospace in 2026—will support domestic demand for special stainless grades and could redirect regional flows of precision alloys.

Strategic priorities for executives in 2026

Based on scenario analyses and supplier scoring, PW Consulting recommends that decision-makers prioritize the following initiatives before mid-2026 to preserve optionality and reduce program risk:

- Embed carbon and tariff scenario clauses into supplier contracts. Short window to negotiate terms tied to CBAM pass-through and Section 232 exposure will differentiate cost outcomes over the next 18 months.

- Adopt a layered sourcing strategy: combine long-term strategic partnerships with flexible regional distributors to manage lead-time and compliance risk without inflating inventory carrying costs.

- Invest in alloy substitution pilots where feasible. Engineering-validation roadmaps in the report show where stainless subtypes can replace higher-cost alloys at acceptable lifecycle trade-offs.

- Accelerate supplier qualification and shared R&D agreements. Co-funded trials can significantly shorten qualification timelines for alternative stainless grades and finishing processes that improve fatigue life or weight efficiency.

- Use targeted M&A and capacity-as-a-service plays to secure critical upstream supply — particularly where certification and metallurgy knowledge creates effective barriers to entry.

- Lock-in price-hedging instruments for nickel-linked exposure and implement transparent pass-through mechanisms to protect program margins.

How PW Consulting’s deliverables translate into boardroom action

The full report is designed not as an academic exercise but as a direct inputs-to-decision system: each chapter concludes with a short set of board-level choices, estimated impact ranges under three scenarios, and recommended KPIs to include in quarterly supplier reviews. For procurement teams, we provide templates for negotiation, a supplier scorecard, and a six-month supplier engagement roadmap. For engineering and program leads, actionable route-maps outline test, qualification, and certification timelines tailored to the typical aerospace program cadence.

Accessing the full intelligence

This release is a strategic preview intended to demonstrate the depth and applicability of PW Consulting’s analysis while preserving the full granularity for subscribers. To unlock the complete dataset, segmentation tables, supplier scorecards, and downloadable tools (including the scenario model and negotiation templates), visit our report landing page or contact our industry practice. The complete study includes the granular splits by region, type, and application that underpin the strategies summarized here — essential inputs for any team preparing capital allocation and sourcing decisions in 2026.

PW Consulting remains available for bespoke briefings, supplier due-diligence engagements, and rapid-market-entry workshops tailored to aerospace OEMs, tier suppliers, and private-equity investors assessing opportunities in the stainless steel value chain.

For detailed analysis of this topic, please visit the official page: Aerospace Aircraft Stainless Steel Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.