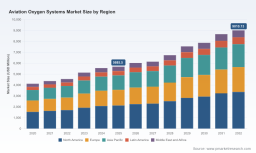

PW Consulting: Aviation Oxygen Systems Market to Expand from USD 5,685.5 Million in 2025 to USD 9,010.1 Million by 2032 at a 6.8% CAGR — North America Leads with USD 2,126.2M

Aviation Oxygen Systems Market: Strategic Outlook for 2026 Decision-Making

PW Consulting’s latest market intelligence on the Aviation Oxygen Systems market synthesizes five years of observed dynamics (2020–2025) and projects industry evolution across a seven-year forecast window (2026–2032). The global market—measured in USD Million—has expanded steadily through the base year 2025 and PW’s forecasting model anticipates continued compound growth at a 6.8% CAGR through 2032. This release is intended as an executive briefing: it highlights the strategic inflection points that matter to OEMs, airlines, MROs, defense planners, and investors in 2026, while preserving the granular split data and proprietary scenario outputs for readers who access the full report.

Aviation Oxygen Systems Market

Headline market trajectory

After a recovery and growth phase during 2020–2025, the Aviation Oxygen Systems market reached a substantial global volume by the 2025 base year. PW’s scenario-driven forecast shows the market expanding further through the late 2020s and into the early 2030s, reflecting a combination of fleet growth, retrofits, regulatory tightening, and aftermarket expansion. The trajectory underscores a durable expansion opportunity for companies that can couple certified product portfolios with resilient MRO and supply-chain strategies.

Aviation Oxygen Systems Market

Why this matters for 2026 strategic decisions

- Investment timing: With a multi-year recovery firmly established by 2025, 2026 is a pivotal year to commit capex to production scale-up, certification pathways, or MRO capacity. Waiting risks misspent cycles as parts of the market move from retrofit to integrated-system demand.

- Regulatory tailwinds and constraints: Recent airworthiness directives and tightening compliance for portable breathing equipment and onboard systems create replacement and upgrade demand—unpredictable in timing but certain in magnitude. Firms without rapid certification or replacement supply chains will face procurement constraints and contract exposure.

- Aftermarket premium: The economics of oxygen systems increasingly favor aftermarket services—MRO, spare parts, inspection cycles, and cylinder hydrostatic testing—creating annuity-like revenue streams that materially affect valuation models in 2026.

Key demand and technology drivers

- Regulatory compliance and safety standards: Regulatory frameworks (notably FAA rules on supplemental oxygen thresholds, cylinder hydrostatic testing, and purity/contamination standards) continue to be primary demand levers. Compliance-driven replacements and mandated maintenance cycles create predictable windows of opportunity.

- Fleet modernization and interior retrofits: Commercial and business aviation operators are incorporating passenger-centric systems and integrated PSUs as part of broader cabin upgrade programs, increasing demand for integrated oxygen delivery and monitoring solutions.

- Military and specialized applications: Defense procurements for OBOGS, compact regulators, and high-altitude solutions remain technologically differentiated, driving R&D investment among a handful of established suppliers.

- Product innovation: Advancements in pulse-demand delivery, lighter composite cylinders, digital monitoring of oxygen consumption, and modular portable systems are reshaping total cost of ownership and maintenance patterns.

Competitive landscape and concentration

The market displays a moderate-to-high level of concentration among established system integrators and specialized manufacturers. The combined market share of the top three and top five suppliers indicates that lead players exert substantial influence over certification standards, aftermarket ecosystems, and OEM supply chains. For 2026, competitive advantage will be determined less by single-product innovation and more by integrated propositions—certified product portfolios, fast-turn MRO capability, and deep OEM/airframe partnerships.

Aviation Oxygen Systems Market

- Aerox Aviation Oxygen Systems (Bonita Springs, FL, USA) – A leading provider spanning portable and installed systems, noteworthy for expanding its MRO footprint through recent acquisitions and FAA-certified repair capabilities.

- Safran Aerosystems Oxygen (AVOX Systems) (Lancaster, NY, USA) – Offers comprehensive passenger and crew oxygen solutions; recent airworthiness directives affecting portable breathing equipment have direct operational consequences for units in service.

- Collins Aerospace (RTX) (Charlotte, NC, USA) – Focuses on integrated oxygen and passenger service unit systems for both commercial and military platforms; strength lies in systems integration with larger avionics and cabin architectures.

- Precise Flight, Inc. (Bend, OR, USA) – Specialist in GA systems with a reputation for durable, PMA/OEM-compatible equipment and long product warranties that favor owner-operators and FBOs.

- Mountain High Equipment & Supply Co. (Redmond, OR, USA) – Known for pulse-demand delivery technology and a portfolio that spans portable to built-in systems.

- Meggitt (now part of Parker Hannifin) (UK) – Strong in military and high-altitude portable systems, with modular AMOS offerings for tactical platforms.

- Honeywell Aerospace (Charlotte, NC, USA) – Provides OBOGS and life support systems with a focus on fighter and transport platforms where reliability and integration with avionics are critical.

Recent strategic moves and implications

- Aerox’s acquisition of an FAA-certified repair station (early 2025) demonstrates an aggressive move to capture aftermarket and MRO margin pools. For competitors, this signals that vertical integration into maintenance and certification services will be a competitive imperative.

- Regulatory activity around portable breathing equipment—adopted ADs and EASA operational directives—creates immediate replacement demand and constrains installation options for certain legacy units. Market entrants without rapid replacement product approvals may encounter limited market access.

- Consolidation among component suppliers and OEMs is likely to accelerate as firms seek to control certification, reduce lead times for critical components (valves, regulators, certified cylinders), and protect aftermarket revenue.

Operational and supply-chain considerations for 2026

Across procurement, manufacturing, and service networks, executives must prioritize three operational questions this year:

- Certification velocity: How quickly can new product variants and retrofit kits achieve TSO/PMA and operator acceptance across jurisdictions?

- Aftermarket capacity: Do current MRO infrastructures align with forecasted hydrostatic testing cycles, AD-related replacements, and increased retrofit activity?

- Supply resilience: Are critical components—composite cylinders, precision regulators, electronic sensors—sourced from single vendors or dual-sourced to mitigate disruption risk?

Strategic playbook: recommended moves for core stakeholders

PW Consulting’s analysis distills pragmatic actions tailored to organizational roles and risk profiles. For 2026 decision-makers, we recommend the following prioritized moves:

- Airlines and fleet operators: Commission a gap analysis of installed oxygen systems against emergent ADs and regulatory guidance; prioritize pre-emptive retrofits where downtime can be scheduled during maintenance checks to avoid operational disruptions.

- OEMs and system integrators: Accelerate modular-certified offerings that reduce install time and interface risk with cabin and avionics systems; invest in field-demonstration programs with key operators to shorten acceptance cycles.

- MRO providers and independent repair stations: Expand hydrostatic testing throughput and develop bundled service packages (inspection + replacement + data reporting) to capture recurring revenue from rising compliance cycles.

- Investors and corporate development teams: Look for targets offering either aftermarket scale (MRO footprint, long-term service contracts) or differentiated tech (OBOGS, pulse-demand efficiency, digital monitoring) rather than pure-play hardware suppliers without service plays.

Report contents — what PW Consulting provides

The full PW Consulting report is designed as an actionable decision-support tool. Key deliverables include:

- A validated market-sizing model (historical 2020–2025 and forecast 2026–2032) with scenario toggles for regulatory shock, defense procurement acceleration, and fuel-price driven fleet utilization changes.

- Competitive positioning maps, supplier scorecards (certification status, aftermarket reach, OEM relationships), and an MRO capability heatmap to prioritize partnership targets.

- Regulatory impact analyses that translate airworthiness directives and FAA/EASA guidance into serviceable demand curves and compliance cost estimates.

- Investment cases and forward-looking business-model scenarios including subscription/MRO bundling, retrofit-as-a-service, and integrated cabin system partnerships.

- Implementation playbooks for 12-month, 24-month, and 36-month horizons tailored to OEMs, airlines, and MROs with recommended KPIs and go/no-go criteria.

What we are not disclosing here—and why it matters

To preserve the report’s value as a strategic research product and to respect client confidentiality where applicable, this briefing intentionally omits granular regional and application-level split figures and specific revenue assignments to subsegments. Those granular tables, supplier revenue breakdowns, and the full scenario outputs are included in the purchasable report and are essential for transactional diligence, bid preparation, and valuation modeling. The high-level insights provided here are sufficient to prioritize strategic investments and to detect where deeper analysis will yield the greatest ROI in 2026 planning cycles.

Conclusion: the 2026 strategic horizon

For executives setting strategy in 2026, the Aviation Oxygen Systems market presents a combination of steady organic growth and episodic upside driven by regulation and defense procurement. The 6.8% CAGR embedded in PW’s base forecast signals attractive expansion, but capturing value will require alignment across certification, aftermarket capability, and supply-chain resilience. Market leaders will be those who transform regulatory compliance into recurring service revenue and who integrate safety-critical equipment into broader cabin and avionics ecosystems.

PW Consulting stands ready to support board-level strategy sessions, due-diligence processes, and operational playbook rollouts. Access the full report or contact our aviation practice to obtain the complete data tables, supplier scorecards, and the scenario model that operationalizes these insights for your 2026 plans.

For detailed analysis of this topic, please visit the official page: Aviation Oxygen Systems Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.