PW Consulting: Global Lock Market at USD 38,500 Million in 2025, Set to Reach USD 58,466 Million by 2032 at a 6.15% CAGR — Asia‑Pacific, Mechanical Locks and Residential Demand Drive Growth in a Fragmented Market (CR3 18.5%)

Lock Market 2026: Strategic Imperatives from PW Consulting’s New Market Research Release

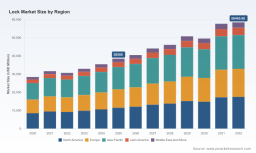

PW Consulting’s latest Lock Market report — built on a 2025 base year with a detailed historical archive (2020–2025) and forward-looking forecasts for 2026–2032 — delivers an operationally focused playbook for executives who must make decisive investments and commercial choices in 2026. The global market is already substantial and poised to expand at a mid-single-digit pace: our base-year sizing puts total industry revenues in 2025 at approximately USD 38.5 billion, growing to nearly USD 58.5 billion by 2032 under the central forecast trajectory (CAGR ~6.15% for the forecast window).

Lock Market

Why this report matters for 2026 decision-makers

- Timing: The coming 12–18 months will determine which manufacturers and channel partners can translate product innovation, supply-chain resilience, and regulatory navigation into durable margin improvement.

- Tactical guidance: Rather than high-level generalities, the report supplies hands-on tools — scenario models, supplier risk heat maps, pricing sensitivity analyses, and M&A due-diligence checklists — that senior leaders can apply to near-term budgeting, procurement decisions, and product roadmaps.

- Risk-adjusted investment lenses: Our financial models incorporate macro shocks and tariff pathways so capital-allocation choices for 2026 are stress-tested across plausible policy and commodity environments.

Market snapshot and macro drivers

The lock market’s trajectory through 2025 reflects a mix of cyclical recovery and structural shifts: steady modernization of building stock, accelerating adoption of electronic and smart access solutions, and durable demand from retrofit and replacement cycles in residential, commercial, and institutional end markets. Over the forecast window to 2032, our central scenario projects the market to expand at roughly 6.15% CAGR — a pace that rewards scale, software-enabled differentiation, and supply-chain agility.

Lock Market

Two structural dynamics deserve emphasis for 2026 strategy: first, the industry remains fragmented — the combined share of the leading suppliers does not yet approach levels that would constrain competition, leaving room for both regional champions and global consolidators to grow; second, product-layer convergence and software monetization are reshaping value capture, allowing pure-play hardware vendors to chase subscription and services uplift.

Lock Market

Competitive landscape: players and positioning

Our review profiles more than a dozen strategic players, from global conglomerates to specialist high-security houses. The competitive set includes multinational access-solution providers and regional industrial champions. Notable dynamics for 2026 include:

- Consolidation of high-security capabilities: recent M&A activity — including the integration of a specialist high-security lock manufacturer into a leading access-solution group in late 2025 and early 2026 — tightens the supply of premium, certified locking systems for government and financial applications, while expanding integrated systems capabilities for commercial customers.

- Market segmentation along capability stacks: incumbents with broad product portfolios are extending into software and access-management platforms; niche vendors are defending margins through certified mechanical and electromechanical solutions targeted at regulated verticals.

- Regional supply bases and go-to-market models continue to differ: global names maintain scale advantages in procurement and standard product lines, while local players win through cost-competitive manufacturing, fast field-service networks, and channel intimacy.

Profiles in the report include corporate strategies, technology roadmaps, distribution models, and M&A/partnership histories for the core companies we track. We analyze where each player is likely to compete more aggressively in 2026 — whether it’s premium electromechanical systems, cloud-enabled access platforms, or low-cost mechanical hardware for emerging markets.

Operational and commercial playbook: what’s inside the report

To support actionable 2026 plans, the report contains a suite of practitioner-oriented deliverables:

- Financial models and scenario planning templates that let you re-run the forecast under alternative tariff, commodity, and adoption-rate assumptions.

- Supplier risk heat maps and transition plans that help procurement teams quantify the cost and lead-time impact of steel and aluminum shocks.

- Go-to-market blueprints with channel segmentation, pricing levers, and installer economics for accelerating penetration of electronic and smart-lock offerings.

- M&A diligence checklists, integration playbooks, and valuation sensitivities for buyers targeting consolidation or capability acquisition.

- Product portfolio optimization guides: margin-by-architecture analyses and recommended capex sequencing for migration from mechanical to electromechanical and cloud-enabled systems.

- Regulatory-impact briefings: practical steps to comply with evolving trade policy and to optimize cross-border sourcing under tariff uncertainty.

These materials are designed so strategy teams can convert insight into deliverables — updated budgets, prioritized R&D pipelines, and acquisition scorecards — within a 30–90 day execution window.

Regulatory, commodity and supply-chain shocks: actionable advice

Two interrelated pressures have recalibrated risk in 2025–26: elevated metal input costs and heightened trade barriers. Notably, steep tariff adjustments on key metals and import routes have materially increased procurement complexity for manufacturers that rely on steel and aluminum for housings, strike plates, and associated door hardware. Tariff actions in late 2025 also introduced frictions across North American supply chains.

For 2026, our recommended mitigations include:

- Diversify sourcing across alloy grades and suppliers; lock in multi-year contracts with explicit passthrough terms where feasible.

- Pursue design-for-material-substitution to reduce dependence on tariff-exposed inputs while maintaining compliance and corrosion-resistance standards.

- Rebalance inventory and supplier lead-time strategies: a shift toward higher safety-stock for critical components combined with nearshoring options for assemblies can reduce disruption exposure.

- Revisit pricing architectures to reflect input volatility: introduce flexible pricing clauses for large institutional contracts and accelerate value-based pricing for software and service layers.

Commercial and product strategy recommendations for 2026

Based on demand signals and our elasticity analysis, we recommend executives prioritize the following strategic moves in 2026:

- Accelerate modularization: develop common mechanical platforms that can accept electronic modules. This shortens time-to-market for smart products and reduces SKUs.

- Monetize software: introduce subscription tiers for access management, remote provisioning, and analytics, targeting property managers and corporate real-estate operators first.

- Service-forward models: bundle hardware with installation, certification, and ongoing support to capture higher lifetime value and differentiate against low-cost imports.

- Targeted premiumization: selectively invest in high-security product lines where certification barriers and patent-protected key control sustain margins.

- Channel modernization: invest in digital trade portals and installer enablement programs to shorten sales cycles and improve attach rates for electronic upgrades.

M&A and partnership lenses

Although the market is large, concentration metrics indicate meaningful fragmentation — the leading firms capture a limited share of total demand. This dynamic creates a fertile backdrop for bolt-on acquisitions that deliver capability (software, wireless communications, encryption), geographic reach, or certified product lines. Our M&A framework in the report lays out target scorecards, integration KPIs, and three valuation scenarios tied to synergies, R&D acceleration, and service monetization.

What we intentionally withhold in this public summary

Consistent with the “trailer” principle underlying this release, we have deliberately withheld the granular subsegment breakdowns and proprietary demand-by-channel matrices that underpin our commercial playbooks. The full report contains detailed regional and end-use disaggregations, SKU-level price and margin assumptions, and downloadable models that permit bespoke sensitivity testing — all essential for rigorous procurement, product, and M&A decisions. These materials are available through the PW Consulting report portal.

Practical next steps for executive teams

- Run the PW Consulting tariff-sensitivity model with your current supplier roster to quantify FY26 margin exposure and adjust supplier contracts accordingly.

- Prioritize two pilot projects in 2026 to convert mechanical product lines into modular platforms with basic connectivity — measure install time, failure rates, and incremental ASP.

- Identify one potential bolt-on acquisition or partnership that would accelerate a software or high-security product capability, and initiate early diligence using our M&A checklist.

- Deploy a channel digitization sprint to improve lead capture, installer onboarding, and aftermarket attachments in priority markets.

PW Consulting’s Lock Market report is built to convert insight into action. The high-level figures included here establish the scale and direction of opportunity; the complete study contains the granular datasets, scenario spreadsheets, and operational playbooks that executives will need to finalize budgets and make confident 2026 commitments. For access to the full dataset, downloadable models, and the complete company profiles and competitive matrices, please refer to the official report page linked from the PW Consulting newsroom.

Prepared by: PW Consulting — Senior Strategic Advisory & Industry Analytics. For inquiry on customized briefings, scenario runs, or executive workshops leveraging our Lock Market datasets, contact our Industry Team.

For detailed analysis of this topic, please visit the official page: Lock Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.