PW Consulting Predicts Chromatography Columns Market Poised for a Steady 5.5% CAGR Through 2032

Chromatography Columns Market 2026: Strategic Preview for Corporate Leaders

As laboratory workflows evolve and biopharma and environmental testing demand sharper separations, the chromatography columns market is entering a decisive phase for corporate strategy. PW Consulting’s new market study—anchored on historical performance through 2025 and a detailed forecast to 2032—translates industry dynamics into practical choices for manufacturers, buyers, and investors. This preview highlights the report’s strategic value for 2026 decision-making, surfaces the forces reshaping the sector, and summarizes competitive moves to watch. For full segment-level metrics and granular scenario tables, access the complete report on the PW Consulting site.

Chromatography Columns Market

Market Trajectory: A Sustainable Growth Path

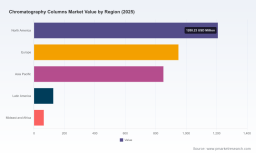

Between 2020 and 2025 the global chromatography columns market expanded steadily, moving from the low billions to an estimated USD 3.2 billion in 2025. Our forecast models—based on supply-chain scenarios, regulatory shifts and demand-side drivers—project a compound annual growth rate (CAGR) of approximately 5.5% over the 2026–2032 horizon. Under central-case assumptions the market crosses into the mid‑single‑digit billion range by the early 2030s, reflecting resilient demand across analytical, preparative and process-scale chromatography.

Chromatography Columns Market

Importantly, this growth is not uniform: pockets of premiumization (high-performance UHPLC, bioseparation consumables), industrialization of process chromatography (mRNA and protein purification), and geographic rebalancing due to trade and regulatory pressures create differentiated margins and risk profiles. The PW Consulting report quantifies these different trajectories and provides scenario-based revenue implications for each strategic posture.

Chromatography Columns Market

Key Dynamics Driving 2026 Decisions

-

Raw material volatility and input-cost pressure: Feedstock changes—most notably silica gel price movement—are affecting BOMs for many column manufacturers. Procurement strategies, supplier diversification and hedging tactics will materially influence 2026 margin outcomes.

-

Regulatory tightening and compliance overlays: New controls on silica particle sizes and local product-labelling obligations in major jurisdictions are increasing the compliance burden. Companies must assess reformulation, testing and certification lead times when planning new SKUs or entering specific regional markets.

-

Trade and tariff disruptions: Recent tariff actions and transport surcharges have raised landed costs and encouraged near‑shoring of capacity or regional inventory hubs. Pricing strategy and supply-chain footprint choices in 2026 will determine competitiveness for cross-border business.

-

Product and application evolution: The market remains technology-led. Innovations in UHPLC, bio‑affinity media and single‑use membrane columns are shifting value to specialty consumables and differentiated service models (testing, application support, column life-extension services).

-

Market concentration and competitive behavior: The three largest players collectively command a meaningful share of the market, and the top five further consolidate position. This concentration underpins strong brand and channel effects but also opens opportunities for focused challengers in niche bioseparation and custom-phase offerings.

Strategic Implications for Corporate Decision-Makers in 2026

-

Portfolio strategy—balance standardization and premiumization: For legacy manufacturers, protecting core HPLC/GC volumes is table stakes; the higher-margin path runs through advanced phases, column technologies tailored to proteomics and mRNA purification, and bundled services (method transfer, extended warranties). Product roadmaps should prioritize modular platforms that support both analytical and preparative use cases.

-

Supply-chain redesign and risk mitigation: Given input-price swings and tariff environments, establish dual-sourcing for critical packing media, evaluate regional contract manufacturing, and adopt dynamic inventory policies. Small changes in ocean freight or raw-material cost can have outsized P&L impacts in a commoditized portion of the market.

-

Regulatory-first product development: Integrate regulatory risk assessment into R&D gating criteria. Pre-certification for pharmacopeial standards, early dialogue with certification bodies, and transparent material composition trails will shorten time-to-market in regulated end-markets.

-

Go‑to‑market differentiation: Sales and marketing must pair technical excellence with outcome-based messaging. Offer application-specific protocols, rapid method transfer bundles and digital tools (e.g., column selection advisors, lifetime tracking) to convert price-sensitive buyers into loyalty-driven accounts.

-

M&A and partnerships: Expect acquisitions to concentrate on capability gaps—specialty bioseparation media, single‑use purification technologies, and regional manufacturing nodes. Strategic partnerships with instrument OEMs and service labs also accelerate adoption through co-marketing and joint validation.

Competitive Landscape: Profiles and Tactical Moves to Monitor

The market is shaped by several established instrument and consumable manufacturers that combine R&D scale with channel reach. PW Consulting’s analysis profiles leading players and assesses the strategic implications of recent product and capacity investments.

-

Agilent Technologies (Santa Clara, CA): A leader in analytical columns across HPLC, GC and UHPLC, Agilent continues to expand its portfolio toward high-throughput bioanalysis. Recent product launches emphasize guard-column and UHPLC performance improvements—moves that reinforce Agilent’s share in method-driven markets and support cross-sell into instrument installs.

-

Thermo Fisher Scientific (Waltham, MA): Thermo Fisher’s breadth enables competitive coverage from LC proteomics to ion chromatography. New column series focused on proteomics resolution indicate a deliberate push into higher-value life-science segments where method reproducibility and throughput matter most.

-

Waters Corporation (Milford, MA): Waters’ emphasis on high-resolution chemistries and pharmacopeial certification supports premium positioning in regulated workflows. Recent certification expansions further strengthen its buy‑side proposition for pharmaceutical customers requiring validated methods.

-

Merck KGaA / EMD Millipore (Darmstadt): With a strong preparative and flash chromatography footprint, Merck’s product mix targets purification and process-scale needs. Its established reputation for media and consumables continues to support cross-segment relevance.

-

Shimadzu Corporation (Kyoto): Shimadzu’s focused SKU releases for biopharma analysis aim to capture incremental share where instrument compatibility and method migration paths matter. Regional product launches suggest a calibrated market entry playbook.

-

PerkinElmer, Restek, Phenomenex and other specialized players: These firms compete on niche chemistries, custom phases and GC dominance. Their agility allows targeted wins in environmental testing and food safety—segments that prize method sensitivity and local support.

-

Sartorius and Cytiva (bioprocess leaders): Firms focused on membrane chromatography and preparative/process columns are capitalizing on the biologics and mRNA production wave. Capacity expansions and targeted product investments are evidence of sustained demand for process-scale purification media.

Collectively, the top three and top five firms show concentrated control over established channels. That said, the rise of differentiated specialty media and regulatory-led product requalification creates entry points for nimble innovators.

Report Contents: What PW Consulting Delivers

The full PW Consulting report is built for action. It includes:

-

Historical market sizing through 2025 and scenario-based forecasts to 2032 with sensitivity analyses tied to raw-material, tariff and regulatory shocks.

-

Segment-level narratives across technology, application and regional clusters (including drivers, adoption curves and pricing dynamics). Note: the executive preview intentionally omits segment numerics—these are available in the full report.

-

Supply-chain maps highlighting critical nodes (packing media, column manufacturing, test labs), unit-cost models, and recommended sourcing strategies for 2026.

-

Competitive benchmarking: product portfolios, recent launches and certifications, capability gaps and M&A target screens tailored for corporates and PE investors.

-

Regulatory impact assessment and a timeline of known and anticipated rule changes, plus practical compliance checklists for product development and labeling.

-

Commercial playbooks—go‑to‑market, pricing, account segmentation, and service bundling templates proven to lift ASPs and retention in high-value accounts.

How Senior Leaders Should Use This Intelligence in 2026

-

Board-level strategy sessions: Rebaseline growth assumptions to reflect the current 5.5% CAGR backdrop and stress-test three-year investment cases under higher raw-material and transport-cost scenarios.

-

Product and R&D prioritization: Sequence investments that deliver near-term certification wins or performance differentiation while preserving longer-term platform bets in bioseparation.

-

Commercial execution: Redeploy field resources toward enterprise accounts where method validation and long-term contracts reduce revenue volatility.

-

PE and corporate development: Use our M&A scorecards to screen targets that close capability gaps or provide regional manufacturing presence that offsets tariff exposure.

Conclusion: Why 2026 Is a Pivotal Year

With the market at an inflection—steady macro growth but heightened operational and regulatory complexity—2026 will reward firms that blend engineering excellence with supply‑chain resilience and regulatory foresight. The competitive landscape favors those who can protect core volumes while capturing higher-margin niches through certification, targeted R&D and service-led differentiation.

PW Consulting’s full Chromatography Columns Market report provides the granular segmentation, financial models, and tactical playbooks necessary to act decisively. Our analysis combines market sizing, concentration metrics and company-level intelligence so that executives can convert insight into profitable decisions.

Next Steps

To access the complete dataset, segment-level forecasts, company scorecards and our recommended 24-month action plan, visit the PW Consulting report page. The full report includes downloadable model files and a workshop-ready presentation to accelerate your 2026 planning cycle.

For detailed analysis of this topic, please visit the official page: Chromatography Columns Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.