PW Consulting Forecast: Robotics in Shipbuilding Market to Expand at a 7.5% CAGR

Robotics in Shipbuilding Market: Strategic Outlook and Decision Playbook for 2026

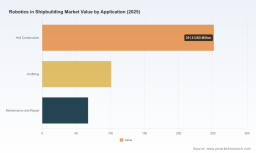

As shipyards confront accelerating demands for throughput, quality, and safety, robotics is moving from niche automation to a strategic infrastructure investment. PW Consulting’s latest market study — with a 2025 base year and a 2026–2032 forecast horizon — quantifies this transition and translates it into executable guidance for executives making investment and procurement decisions in 2026. At a headline level, the global Robotics in Shipbuilding market expanded to an estimated USD 420.0 Million in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 7.5% through the 2026–2032 forecast period (reaching modeled revenue nearing USD 697 Million by 2032). These macro trajectories reflect structural forces that make robotics not a cost center experiment but a strategic lever for competitiveness.

Robotics in Shipbuilding Market

Why 2026 is a Pivotal Decision Year

-

Labor and capacity pressures: Persistent shortages of skilled welders and fabricators have pushed shipbuilders to explore adaptive robotic welding and material handling as capacity-sustaining measures rather than optional efficiency projects.

Robotics in Shipbuilding Market -

Rapid advancement of physical AI: Partnerships and MOUs signed in early 2026 between major naval primes and physical-AI robotics vendors demonstrate a shift from pilot-stage proof-of-concept to integration-scale programs targeting measurable throughput gains.

Robotics in Shipbuilding Market -

Falling component costs and modular architectures: Key enabling components — including six-axis force-torque sensing and integrated control modules — have experienced significant price declines, lowering the entry threshold for complex applications such as force-guided welding and surface preparation.

-

Regulatory and safety tailwinds: Emerging standards for collaborative robots and guarded work cells support human-robot coexistence in shipyards, permitting higher utilization without the traditional safety fencing that fragments workflows.

-

Strategic public investment: Research grants and government commitments to AI-enabled shipbuilding underline national-level priorities to preserve industrial capacity while modernizing labor models.

What the Numbers Mean for Buyers and Investors

The market’s projected 7.5% CAGR and modeled progression from USD 420.0 Million in 2025 toward near-USD 697 Million by 2032 are not abstract forecasts; they are decision triggers. For procurement leads, these numbers imply a near-term imperative to establish vendor roadmaps and pilot sites: early movers will define standards, capture integration learning curves, and reduce long-run TCO. For CFOs, the growth trajectory supports allocating staged capital — a combination of targeted CAPEX for core systems and OPEX for AI/analytics subscriptions — to smooth adoption risk.

From a cost perspective, industrial robotic systems suitable for marine shipbuilding typically fall within a capital range that makes modular rollout an effective strategy: unit hardware expenditures can cluster in a defined mid-five-figure to low-six-figure band, with total installed cost multiples that reflect integration, fixtures, and commissioning. This dynamic favors phased deployments and vendor partnerships that bundle installation and application engineering rather than pure hardware procurement.

Report Offerings — Practical Intelligence, Not Just Projections

PW Consulting’s report is structured around the practical questions executives must answer in 2026. Rather than a catalog of market slices, the deliverables are designed to be directly operationalizable:

-

Executive decision framework: A buyer’s guide to determine build vs. buy, procurement sequencing, and pilot-to-scale criteria tailored to capital budgets and production cadence.

-

Total Cost of Ownership (TCO) models: Scenario-based TCO calculators that incorporate capital, integration, training, productivity uplifts, and maintenance across multi-year horizons.

-

Deployment playbooks: Step-by-step templates for pilot selection, system integration, human-machine-interface (HMI) design, and workforce reskilling plans.

-

Risk and compliance matrix: Practical mitigation strategies for intellectual property, cybersecurity of robotic control systems, and safety certification pathways for cooperative work cells.

-

Vendor selection toolkit: Scorecards and negotiation playbooks to capture lifecycle services, spare-part provisioning, and SLAs that matter in high-mix, low-volume shipyards.

-

Scenario planning and sensitivity analysis: Upside and downside cases tied to raw-material shocks, labor shifts, and policy interventions to stress-test investment decisions.

Competitive Landscape — Who Matters and Why

The market exhibits moderate concentration: the top three vendors account for a meaningful portion of industry revenues, while the top five capture a majority share. This structure yields a dual-path competitive dynamic: major global robotics suppliers continue to dominate core hardware, while specialist and software-first entrants compete on domain-specific capabilities and systems integration.

-

ABB (Switzerland) — A global leader in industrial robotics and automation, ABB supplies integrated welding, material handling, and precision assembly systems designed to scale across large vessel programs. Strategy implication: strong choice for end-to-end automation programs with global service footprints.

-

FANUC Corporation (Japan) — Known for high-precision robots and high-volume reliability, FANUC supports large Asian shipyards where repeatability and throughput are the priority. Strategy implication: preferred where robust, high-duty-cycle hardware is essential.

-

KUKA AG (Germany) — Focused on complex automation tasks, KUKA targets welding, assembly, and handling tasks in constrained, marine-specific environments. Strategy implication: attractive where systems require deep application engineering and advanced path planning.

-

Yaskawa Electric Corporation (Japan) — Delivers Motoman robots with proven arc-welding performance, emphasizing reliability in heavy industrial settings. Strategy implication: strong candidate for retrofit and hybrid human-robot workflows.

-

Kawasaki Heavy Industries (Japan) — Combines robotics with heavy machinery expertise, useful for painting, structural assembly, and integrated production lines. Strategy implication: well-suited for yards integrating robotics across multiple production stages.

-

KRANENDONK (Netherlands) — Specialist provider of intelligent automation for panel, block, and pipe fabrication with adaptive gantries for non-repetitive work. Strategy implication: an option for yards with high product variability.

-

Inrotech (Lincoln Electric, Denmark) — Offers adaptive mobile welding systems that minimize programming requirements and work well in high-variation welding environments. Strategy implication: reduces dependence on high-end programming expertise for variable joints.

-

GrayMatter Robotics (USA) — An AI-driven provider focused on surface preparation, grinding, coating, and inspection; notable for partnerships with naval shipbuilders. Strategy implication: strong for modernization programs emphasizing physical-AI surface workflows.

-

Path Robotics (USA) — Supplies autonomous welding cells driven by physical AI and is active in naval and commercial shipbuilding partnerships. Strategy implication: attractive for programs seeking high autonomy levels in welding operations.

Competitive implications: expect consolidation around systems integrators that can bundle hardware, domain software, and lifecycle services. At the same time, niche innovators that solve discrete pain points — for example, adaptive welding in variable-joint environments or AI-driven surface preparation — can capture premium value through services and repeatable IP.

Recent Industry Signals and Their Strategic Consequences

-

Defense primes integrating physical AI : Partnerships and MOUs in 2026 between major shipbuilders and physical-AI vendors signal naval shipbuilding is accelerating automation adoption to address both labor shortages and production tempo. For commercial yards, these moves lower adoption risk by validating performance at scale.

-

Research and public funding : Multi-million-dollar grants for AI and digital-twin development reinforce a longer-term ecosystem bet on reducing the impact of design deviations and accelerating design-for-assembly approaches.

-

Cost structure evolution : Declines in force-torque sensor pricing and modular controller designs reduce entry barriers for advanced force-guided tasks, enabling more yards to trial collaborative robotic cells for tasks previously considered too complex or costly.

Actionable Recommendations for 2026 Decision-Makers

-

Prioritize pilot projects that de-risk integration — Select two to three high-value, repeatable tasks (e.g., arc welding of repetitive seams, automated surface prep for coatings) and run 6–12 month pilots coupled with TCO measurement and operator upskilling plans.

-

Structure procurement around lifecycle outcomes — Negotiate SLAs that include uptime guarantees, spare parts provisioning, and application engineering hours rather than procuring hardware alone.

-

Develop partnership ecosystems — Combine hardware incumbents with AI-focused integrators and local systems integrators to accelerate knowledge transfer and preserve operational control.

-

Invest in workforce transition — Channel savings from productivity gains into reskilling programs that transition welders and assemblers into robotic operators and QA specialists.

-

Adopt a phased capital plan — Use staged CAPEX aligned to milestone-driven scale-ups to avoid oversized initial investments and to incorporate insights from early pilots into broader rollouts.

Methodology and What’s Behind the Curtain

The study synthesizes historical market activity from 2020–2025 with field interviews, vendor financials, procurement data, and company disclosures. The forecast through 2032 blends bottom-up adoption modeling with scenario-driven macro assumptions around labor availability, policy interventions, and component-cost curves. Concentration metrics and vendor profiles are derived from cross-validated revenue estimates and primary research.

In keeping with the “trailer” principle — designed to provide strategic clarity while preserving actionable granularity for report subscribers — this article highlights the central trends, competitive dynamics, and pragmatic frameworks you need for 2026 decisions. Detailed segment-level breakouts, region-application revenue splits, and vendor-specific market share figures are reserved for the full report and interactive data tools.

Next Steps

For procurement directors, strategy teams, and investors evaluating robotics programs in shipbuilding, PW Consulting’s Robotics in Shipbuilding Market report provides the playbook to convert market momentum into measurable production outcomes. To access the full segment-level analysis, proprietary vendor scorecards, and scenario TCO models, visit the report page or contact a PW Consulting industry specialist to request an executive briefing and sample modules tailored to your operational context.

For detailed analysis of this topic, please visit the official page: Robotics in Shipbuilding Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.