PW Consulting: Frozen and Freeze‑Dried Pet Food Market Poised to Grow at 6.5% CAGR, New Insight Report Says

Frozen and Freeze‑Dried Pet Food Market: Strategic Imperatives for 2026 Investors and Operators

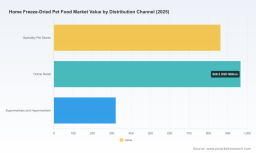

In 2026 the frozen and freeze‑dried pet food market sits at an inflection point. After reaching a global market size of USD 1,905.0 million in 2025, PW Consulting projects continued expansion at a compound annual growth rate (CAGR) of 6.5% through 2032, taking the market into the low‑thousand‑million range by the end of the forecast period. This growth trajectory reflects sustained premiumization of pet diets, rapid product innovation in raw and minimally processed formats, and rising retail and direct‑to‑consumer adoption. For companies allocating capital or revising operating plans in 2026, understanding the operational levers behind that headline growth—rather than the headline alone—is the core utility of our research.

Frozen and Freeze-Dried Pet Food Market

Why 2026 Is Pivotal

Several converging forces make 2026 a decisive year for strategic positioning in frozen and freeze‑dried pet foods:

Frozen and Freeze-Dried Pet Food Market

- Regulatory acceleration: Model changes from AAFCO and state‑level label modernizations that began rolling out in 2024–2025 increase compliance complexity for ingredient declarations, nutrition displays and intended‑use statements.

- Supply‑side tension: Heavy overlap between pet and human protein supply chains—particularly chicken and beef—creates price and availability volatility that can rapidly erode margin if not actively managed.

- Quality & safety signals: A cluster of voluntary recalls in 2025–2026 has raised buyer sensitivity to micronutrient profiling and pathogen risk, elevating the value of traceability and lab‑verified controls.

- Competitive creep: Incumbent mass and premium brands are introducing hybrid SKU formats (e.g., dry kibble with freeze‑dried bites), compressing shelf space and forcing legacy artisanal players to scale or specialize.

Report Utility: Actionable Tools for 2026 Decisions

PW Consulting designed this research to be decision‑centric for 2026 strategic moves. The report packages diagnostic frameworks and executable tools that translate market signals into boardroom choices without requiring clients to extrapolate raw tables.

- Supply chain map and capacity heatmap — identifies bottlenecks by node (ingredient sourcing, primary processing, co‑pack capacity, cold chain logistics) so CFOs can prioritize capacity investments or contractual hedges.

- BOM (Bill of Materials) decomposition logic — a repeatable model showing how formula changes and yield differentials interact with ingredient cost inflation to affect gross margin, enabling scenario planning under multiple price paths.

- Yield adjustment and loss models — practical routines for converting laboratory rehydration yields and plant yields into SKU economics without exposing proprietary sample numbers.

- Technology and capital roadmap — a staged view of automation, cold‑chain monitoring, and in‑line testing investments that lift throughput and reduce recall risk, with payback bands tailored to 2026 cost structures.

- Compliance and labeling playbook — a matrix matching likely AAFCO/state adoption timelines to label redesign checkpoints and required documentation, helping legal and regulatory teams sequence workstreams.

- Co‑manufacturing and outsourcing decision tree — a structured approach to when to in‑source versus partner with contract freeze‑dryers, including vendor selection criteria and KPI targets for Design Wins.

How These Tools Solve 2026 Pain Points

Executives tell us their immediate priorities are (1) protecting margin amid input volatility, (2) avoiding disruptive safety events, and (3) securing retail placements while scaling DTC. The tools above address those priorities directly:

- Cost control: BOM decomposition and yield models let procurement and operations stress‑test supplier mixes and substitution scenarios before contracts are signed.

- Compliance readiness: The labeling playbook reduces rework risk and shortens time to market for reformulated SKUs required by new state rules.

- Commercial momentum: The co‑manufacturing decision tree and technology roadmap align capacity with retail calendar cycles, improving the probability of winning shelf space and sustaining DTC availability.

Competitive Landscape — Dimensions That Determine Winners

The competitive map in 2026 remains fragmented—CR3 is 22.5% and CR5 is 28.5%—which favors nimble brand plays and local capacity leaders. Rather than predicting which firm will grow faster, PW Consulting focuses on the structural dimensions that determine competitive advantage in freeze‑dried and frozen segments:

- Supply moats: Long‑term preferred partnerships with protein suppliers, secured through multi‑year contracts or backward integration, protect margin during commodity cycles.

- Operational moats: Proprietary cold‑chain SOPs, validated yield profiles and co‑manufacturing governance reduce recall exposure and shorten remediation timelines.

- Brand moats: Verified ingredient provenance and animal‑welfare narratives create willingness‑to‑pay in premium cohorts, but they require proof points and audit trails to scale credibly.

- Design Wins: Retail and subscription channel design wins are driven by consistent shelf life, attractive pack formats for omnichannel sales, and demonstrable in‑store velocity in initial test markets.

Examples from the competitive set illustrate these dimensions without divulging our proprietary scenario work. Companies focused on freeze‑dried raw formats (e.g., those emphasizing human‑grade sourcing and small‑batch production) derive brand moats from ingredient transparency and premium positioning. Co‑manufacturers and legacy producers derive leverage from scale, repeatable process controls and the ability to serve multiple private‑label customers. For commercial partners and investors, the key is to map potential partners or acquisition targets against the four competitive dimensions above, and evaluate whether a target’s strengths are defensible under stress scenarios such as a recall or protein price spike.

Risk Signals and Early Warning Indicators

Our market monitoring in 2026 focuses on a compact set of early warning indicators that predict revenue and margin shocks:

- Recall frequency and root cause clustering — repeated incidents tied to micronutrient imbalance or pathogen detection shorten shelf life of brand equity.

- Ingredient cost divergence — rapid spreads between human‑food and pet‑food protein bids signal immediate margin pressure for non‑hedged SKUs.

- Regulatory adoption milestones — staggered state adoptions of model labeling rules create a rolling compliance calendar that must be resourced.

- Capacity utilization at large freeze‑dry contractors — utilization spikes often precede lead‑time extension and price creep in co‑manufacturing contracts.

PW Consulting observed multiple relevant events entering 2026, including voluntary recalls and new hybrid product launches that validate these indicators as actionable triggers for risk mitigation.

Methodology and Research Rigor

PW Consulting’s conclusions are grounded in layered triangulation and transparent audit trails. Our methodology combines:

- Primary research: Structured executive interviews across ingredient supply, co‑manufacturing, retail buyers and logistics providers; plant tours and capacity validation exercises.

- Proprietary data: SKU‑level scanner and e‑commerce performance feeds, combined with contract and procurement snapshots obtained under NDA and normalized for comparability.

- Technical verification: Analytical laboratory assays for rehydration yield and micronutrient profiling, cross‑checked against regulatory filings and recall databases.

- Open‑source and alternative data: Patent citation analytics, customs and shipment flows, and satellite imagery for capacity verification.

We avoid publishing raw, non‑public datasets in the public summary. Instead, decision makers receive calibrated models and verifiable signposts that allow them to run internal “what‑if” scenarios using their own commercial data.

Strategic Imperatives for 2026

For management teams and investors preparing 2026 budgets, the following high‑level imperatives encapsulate the most efficient use of capital and management focus:

- Prioritize traceability and lab validation investments that convert recall risk into competitive differentiation.

- Align procurement strategy to include active hedges or diversified protein baskets, rather than single‑source exposures to human‑food supply chains.

- Opt for staged automation and modular freeze‑dry capacity that can be scaled with demand rather than large, single‑stage CAPEX commitments.

- Negotiate co‑manufacturing contracts with explicit SLAs for yield, pathogen control and turnaround to preserve Design Wins with retail and DTC partners.

- Use labeling readiness as a commercial lever—repackaging to comply with new requirements can be an opportunity to refresh merchandising and DTC messaging.

Call to Action

PW Consulting’s full report contains the interactive market maps, the BOM templates, yield‑adjustment calculators and the vendor scorecards that enable precise capital allocation decisions for 2026. To access the comprehensive technical annex and the downloadable toolset, visit our report page: Download the Frozen and Freeze‑Dried Pet Food Market report .

Closing Frame

2026 rewards firms that can convert operational discipline into commercial advantage. The market’s growth path is clear at the aggregate level, but the profit pools will be determined by execution on traceability, flexible capacity and validated product performance. PW Consulting’s modular toolset is built to convert market signals into executable, measurable moves—without exposing clients to the noise of raw segmentation tables. Companies that adopt this structured approach in 2026 will most effectively capture the upside of a growing market while insulating themselves from the downside shocks already visible in today’s supply chains and regulatory environment.

For detailed analysis of this topic, please visit the official page: Frozen and Freeze-Dried Pet Food Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.