PW Consulting: Tetramethyl Ammonium Hydroxide Market Poised to Hit USD 702.1 Million by 2032

Tetramethyl Ammonium Hydroxide Market 2026: Strategic Imperatives for Capital Allocation and Operational Resilience

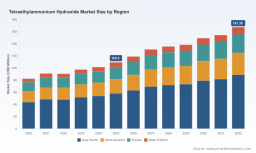

PW Consulting releases an executive briefing distilled from our comprehensive Tetramethyl Ammonium Hydroxide (TMAH) market study, calibrated for 2026 decision-making. Our analysis synthesizes macro trajectory, competitive structure, regulatory inflection points and practical operating tools designed to aid capital allocation, M&A screening and procurement strategies. The global market is growing—from a 2025 base of USD 487.3 Million—and is projected through our 2026–2032 forecast horizon at a compound annual growth rate (CAGR) of 5.2%, reaching approximately USD 702.1 Million by the end of 2032. This growth profile and the market’s concentration metrics create a narrow window in 2026 for advantaged actors to lock in scale, secure design wins and re-engineer supply chains for compliance and cost flexibility.

Tetramethyl Ammonium Hydroxide Market

Why 2026 Is a Pivotal Year

Three converging forces make 2026 a strategic inflection year for TMAH participants:

- Regulatory tightening: Recent amendments proposed by the U.S. Department of Transportation (PHMSA) reshape hazardous-material classification, packaging and special provisions for quaternary ammonium hydroxide solutions and solids. This raises near-term compliance costs and accelerates the need for packaging redesign and transport rerouting strategies.

- Industrial upgrading: Semiconductor and advanced material manufacturers continue to press for higher-purity chemistries and predictable supply, driving more stringent supplier qualification regimes and longer Design Win lead times.

- Market consolidation dynamics: The TMAH market demonstrates mid-to-high concentration; our analysis shows that the three largest suppliers control a clear majority share, and the top five account for an even larger portion—conditions that favor scale-based defenders and create entry barriers for undifferentiated supply.

What PW Consulting’s Report Delivers — Practical Tools, Not Platitudes

Our full report is deliberately operational. It moves beyond static forecasting to provide the toolset that procurement, operations and strategy teams need to act in 2026. Key deliverables include:

- Supply-chain topology maps that identify single points of failure, dual-sourcing opportunities and freight-mode sensitivities under new hazardous-material rules.

- BOM decomposition logic that links end-product cost sensitivity to TMAH purity grades and packaging choices, enabling granular scenario-based cost modeling without exposing proprietary supplier price points.

- Yield-adjustment and process-loss models that quantify the impact of raw-material variability and form-factor (solution vs. solid) on throughput and waste—useful for capex prioritization on containment and in-line QA.

- A technology roadmap tracing pathway options for incremental purity upgrades, alternative chemistries and containment/neutralization investments aligned to ESG and safety compliance timelines.

Each tool is built to be applied within a corporate decision cycle: stress-test budget proposals, prioritize retrofit investments, and inform contractual protections tied to regulation-driven logistics risk. Rather than publishing prescriptive parameter values, the report shows you the levers and the analytical templates so internal teams can quickly plug in proprietary numbers and derive investment-grade outputs.

Competitive Landscape: Where Moats Matter in 2026

Our competitive assessment focuses on the dimensions that will determine winners and losers in 2026—without publishing confidential strategic forecasts. Pw Consulting evaluates each competitor across a consistent set of strategic vectors:

- Scale & geographic reach — ability to absorb regulatory compliance costs and re-route logistics without service interruption.

- Quality differentiation — demonstrated capacity to deliver electronic-grade material and the supplier controls that underpin long-term semiconductor qualifications.

- Customer intimacy & design wins — distribution of technical support, co-development capability and speed of qualification that convert pilot engagements into multi-year contracts.

- Operational resilience — redundancy in feedstock, in-house packaging capabilities and audited downstream traceability.

Representative players we track include established global specialty chemical houses and regional bulk suppliers. For example, firms with multinational production footprints can leverage cross-border sourcing to mitigate localized transport or packaging shocks, while domestic-focused producers often compete on price and responsiveness. Technical suppliers that have cultivated process support teams and clean-room-compatible grades exhibit stronger defense against commoditization through repeat Design Wins.

PW Consulting’s company dossiers benchmark these dimensions qualitatively, illustrating how protective “moats” are constructed—whether through regulatory compliance expertise, proprietary quality controls, or customer co-development capabilities. For a complete set of competitor profiles and the proprietary scoring matrix used to assess 2026 readiness, see the full report: Access the full TMAH market research .

Regulatory Shock-Testing and Operational Response

The PHMSA proposals in early 2026 alter the operating envelope for TMAH in ways companies cannot ignore:

- Reclassification and packaging mandates increase the fixed cost of distribution and raise the return on investment for in-region packaging and warehousing.

- New special provisions and toxicity designations make end-to-end traceability and documented neutralization plans a commercial requirement in many RFQs.

- Transport-mode constraints will drive modal shifts and trigger re-evaluation of landed cost models across customer portfolios.

Our scenario modules let teams evaluate the impact of these permutations on landed cost, lead time, and working capital. That analysis clarifies whether to invest in packaging modernization, local repackaging hubs, or contractual price escalators tied to regulatory milestones.

ESG, Compliance & Insurance: Board-Level Stakes in 2026

Buyers and risk committees increasingly treat chemical-handling compliance as a capital-allocation issue. Investors now demand documented mitigation against transport incidents and evidence of responsible end-of-life handling. Insurance underwriters are pricing in regulatory risk—making it costly to under-invest in compliance. Our report provides a compliance-risk matrix that links specific investments to reduced regulatory and insurance exposure, enabling CFOs to justify spend on packaging redesigns, local repackaging, and enhanced QA.

Methodology — Layered Triangulation for Actionable Intelligence

PW Consulting’s conclusions rest on layered triangulation and transparent provenance. Our approach combines:

- Patent and regulatory corpus analysis to detect technology adoption trends, supplier IP positioning and lag times between patent filing and commercial qualification.

- Primary interviews with procurement heads, quality managers and logistics officers across semiconductor fabs, specialty chemical distributors and major end-users to capture non-public qualification timelines and cost sensitivities.

- Trade-flow and customs analytics to infer shipment patterns, modal mix and supplier origin-destination pairs—cross-checked against audited supplier disclosures and on-site verification where available.

- Supplier BOM reverse-engineering and on-site sampling where permitted to validate purity profiles and packaging practices.

These layers are reconciled using statistical and judgmental weighting to deliver both directional accuracy and confidence intervals around key operational metrics. Importantly, our method allows us to reconstruct sensitive insights (for example, where Design Wins are clustering or where single-supplier dependencies exist) without exposing commercial details that would compromise client confidentiality.

Actionable Recommendations for 2026 Executives

For executives preparing 2026 budgets, the following actions are priority-ranked in our playbook:

- Immediate regulatory gap assessment: map current packaging and transport practices to proposed PHMSA rules and prioritize investments that materially reduce landed-cost volatility.

- Supplier qualification acceleration: allocate resources to accelerate technical trials with tier-one suppliers that demonstrate electronic-grade capability and logistical flexibility.

- Localized contingency capacity: evaluate near-market repackaging or warehousing to avoid cross-border regulatory exceptions and reduce insurance premiums.

- Design Win playbooks: institutionalize cross-functional squads (R&D, quality, procurement) to compress qualification cycles and secure multi-year purchasing commitments.

Next Steps & How to Obtain the Complete Intelligence

This briefing highlights the report’s value in supporting capital-allocation decisions and operational interventions in 2026. PW Consulting’s full report contains the detailed distribution maps, the supplier scoring matrices, and the downloadable analytical templates needed to operationalize the above recommendations. For organizations that need immediate implementation modules—procurement checklists, contractual clauses keyed to regulatory milestones, and scenario-ready cost models—our full dataset and appendices are available. To obtain the full research package and tailored advisory options, visit: View the complete TMAH market research report .

For detailed analysis of this topic, please visit the official page: Tetramethyl Ammonium Hydroxide Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.