PW Consulting: Automotive Sunroof Market to Reach USD 33.7 Billion by 2032

Automotive Sunroof Market — Strategic Outlook 2026

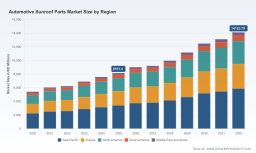

PW Consulting publishes a focused strategic briefing based on our latest market study, offering executive teams a forward-looking playbook for capital allocation, supplier selection and product roadmap prioritization in the automotive sunroof ecosystem. The global market reached USD 15.7 Billion in the base year 2025 and is now growing at a projected compound annual growth rate of 11.6% for the 2026–2032 forecast window, driven by glazing innovation, system integration and renewed OEM design activity.

Automotive Sunroof Market

Executive summary — why 2026 is a pivotal decision year

Automotive OEMs and tier‑1 suppliers are allocating development and manufacturing budgets in 2026 under three simultaneous pressures: tighter safety and recyclability regulations, the need to reduce vehicle curb weight for emissions targets, and premiumization of vehicle interiors that elevates sunroof specifications from optional accessory to perceived value differentiator. Against this backdrop, the sunroof market trajectory—more than doubling in size toward 2032—creates both urgency and runway for strategic moves now.

High‑level takeaways

-

Market momentum: The industry is in a structural growth phase; our base-year positioning and forecast window frame a multi‑year investment horizon rather than a short-term spike.

-

Concentration: Market concentration remains material—CR3 at 68.0% and CR5 at 81.0%—so winning design authority with OEMs yields outsized commercial returns.

-

Structural change: Materials (lightweight glazing, polycarbonate), integrated electronics (VIPV and sensor embedding) and manufacturability are now equal parts of product specification and cost targets.

Market dynamics shaping the 2026 competitive landscape

Our fieldwork and quantitative models identify four demand-side and four supply-side forces that together explain the current rapid expansion.

-

Demand-side drivers:

-

Vehicle premiumization — larger glass footprints and acoustic laminates shift bill‑of‑materials (BOM) composition.

-

Electrification and range optimization — lighter roof systems reduce energy penalty and are specified early in vehicle architecture decisions.

-

Customer experience — integrated shading, zonal tinting and solar energy capture (VIPV) are moving from concept to production intent.

-

Regulatory push — recyclability and impact/safety mandates are forcing platform redesigns in 2026 implementation cycles.

-

-

Supply-side drivers:

-

Material innovation — polycarbonate and multi‑layer laminated glass adoption to balance weight, safety and cost.

-

Scale and footprint — manufacturers are rebalancing capacity to be proximate to major OEM assembly hubs.

-

Manufacturing digitization — AI‑driven yield models and tighter supplier integration reduce warranty exposure for OEMs.

-

Vertical integration among glass, kinematics and drive suppliers is intensifying to protect design wins.

-

Operational tools: what the report delivers and how it solves 2026 pain points

The report is intentionally practical. It bundles analytical tools that go beyond market sizing to support immediate operational decisions in 2026:

-

Supply‑chain map: a layered supplier map that clarifies who supplies glass, kinematics, drives and sub‑assemblies — designed to accelerate dual‑sourcing and critical‑path risk mitigation.

-

BOM decomposition logic: a reproducible framework for disaggregating module cost drivers so procurement and engineering can target the top 20% of components responsible for 80% of cost volatility.

-

Yield‑adjustment models: scenario templates that translate process yields and scrap rates into near‑term cashflow and working capital implications for production ramp plans.

-

Technology roadmaps: a matrix linking material choices, testing requirements and compliance milestones to anticipated OEM platform launch windows.

-

Supplier scorecards and design‑win checklists: operational templates to evaluate partner fit on quality, IP, manufacturing capacity and ESG readiness.

Each tool is built to address 2026 priorities—cost control in the face of material inflation, accelerated compliance with recycling and safety directives, and minimizing ramp risk for new panoramic roof modules—without disclosing the report’s proprietary parameter sets in this release.

Competitive landscape — dimensions that decide winners in 2026

Our competitive analysis evaluates firms across repeatable dimensions that determine long‑term advantage. These dimensions, not the discrete forecasts we publish for each company, are what strategic teams should use to stress‑test their plans.

-

Design‑win moat: incumbency with OEM platform engineers, early integration into vehicle architecture, and proprietary sealing/actuation solutions.

-

Manufacturing scale and footprint: proximity to OEM assembly plants and capability to support multi‑shift, high‑volume ramps.

-

Material and glazing relationships: secured upstream supply of advanced laminated glass or polycarbonate and contractual terms that hedge raw‑material volatility.

-

Systems integration capability: ability to bundle glass, shading, electronics and drives into a single module reduces OEM integration cost and shortens validation cycles.

-

ESG and regulatory readiness: recyclability claims, CO₂e lifecycle reductions and evidence of compliance testing are increasingly gatekeeping criteria.

Industry leaders cited in our study—ranging from traditional roof specialists to glass manufacturers and broader vehicle suppliers—exhibit different mixes of these moats. Recent on‑the‑record moves illustrate how these dimensions play out in practice: Webasto expanded panoramic glass production and publicly launched a lower‑carbon "Greener Roof" platform; Inalfa introduced a multi‑panel panoramic system with acoustic laminates; and glass manufacturers are demonstrating vehicle‑integrated photovoltaic prototypes. These actions confirm the strategic direction we model in the full report.

To examine our company profiles and the competitive scorecards in detail, please consult the full intelligence package: Access the full Automotive Sunroof Market report .

Regulation, material trends and testing — compliance is a capital allocation driver

2026 sees a confluence of regulation and material shifts that have immediate capital implications:

-

Recyclable glazing mandates in key markets require retooling of glass assembly lines and proof points for end‑of‑life recovery.

-

Tighter rollover and impact standards compel reinforced frames and validation testing, influencing both part geometry and supplier selection.

-

Adoption of polycarbonate solutions in specific use cases reduces pedestrian impact risk but alters UV and scratch protection requirements.

These factors materially change the investment calculus for OEMs and suppliers in 2026—whether to retrofit existing lines, accelerate a platform redesign, or secure long‑lead raw material contracts.

Methodology — layered triangulation and proprietary data capture

PW Consulting’s conclusions reflect a disciplined research approach combining public and proprietary inputs. Our Layered Triangulation method superimposes multiple independent evidence streams to validate key outputs:

-

Patent citation mapping to identify technology diffusion and supplier IP density.

-

Teardown BOM analysis and cost‑model reverse engineering to infer supplier economics and margin pools.

-

Confidential interviews with OEM program managers and tier‑1 procurement leads conducted under NDA, supplemented by factory tours and process audits.

-

Customs shipment analytics and component‑level trade flows to verify capacity shifts and regional footprint movements.

Where our models rely on non‑public inputs, we describe the nature of the evidence (for example, number of OEM interviews or factory validations) rather than republishing proprietary figures in this press release—ensuring reproducibility for clients while protecting source confidentiality.

Strategic recommendations for management teams in 2026

Based on the analysis, we recommend executives prioritize three concurrent plays this year:

-

Secure strategic supply lines: prioritize long‑lead agreements for advanced glazing and evaluate near‑shoring where regulatory or tariff risk is concentrated.

-

Invest selectively in differentiated modules: fund technologies that accelerate design wins—integrated shading, acoustic laminates and VIPV readiness—while using BOM analytics to keep unit cost disciplined.

-

Build compliance and test capacity: allocate capex to meet recyclability and impact testing timelines, preventing last‑minute redesign costs and launch slippages.

Each recommendation maps to an operational template in the full report (risk matrices, supplier scorecards, and CapEx stress tests) that executives can apply directly to 2026 program decisions.

Next steps — how to use this briefing

This release is a strategic preview designed to help procurement, product and corporate development teams triage their 2026 priorities. For clients requiring executable artifacts—complete BOMs, supplier maps, design‑win playbooks and scenario‑tested financial models—our full automotive sunroof study contains the underlying datasets and templates to accelerate implementation.

For immediate access to the complete intelligence suite and templates, please visit: https://pmarketresearch.com/worldwide-automotive-sunroof-parts-market-research .

About PW Consulting

PW Consulting is a strategy firm specializing in automotive components and mobility ecosystems. Our hybrid research model combines advanced data science, in‑market verification and hands‑on engineering teardown work to produce investment‑grade intelligence for executives and investors navigating complex industrial transitions.

For detailed analysis of this topic, please visit the official page: Automotive Sunroof Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.