PW Consulting Forecast: Instrument Transformers Market to Reach USD 261.9 Million by 2032 at a 6.5% CAGR; Current Transformers Estimated at USD 97.0 Million

Instrument Transformers Market — Strategic Imperatives for 2026 Capital Allocation

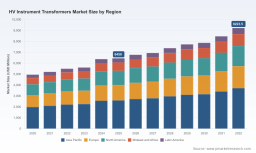

PW Consulting’s new market research briefing synthesizes the commercial and technical realities shaping the worldwide high‑voltage instrument transformers (HVIT) market in 2026. Anchored on a 2025 base year and a validated historical series for 2020–2025, our forecast horizon runs to 2032. The global market is expanding at a steady 6.5% CAGR: from an assessed size of USD 169.0 Million in 2025 to an expected USD 261.9 Million by 2032, with the first forecast year 2026 estimated at USD 180.7 Million. These headline figures are deliberately selective — they establish the market scale and momentum while inviting readers to consult the full report for granular regional and application distributions.

Instrument Transformers Market

Why 2026 is a critical inflection for capital allocation

Investors and corporate strategists face compressed decision windows in 2026 due to three converging dynamics:

- Grid modernization programs and accelerated renewable integration increase demand for precision measurement and protection at HV nodes, raising the performance bar for instrument transformers.

- Regulatory tightening on metering accuracy and traceability — including stronger national‑level accuracy requirements — increases certification lead times and supplier switching costs.

- Supply‑chain re‑shoring and capacity investments by established players are shortening the opportunity to secure long‑lead manufacturing slots and design wins for major substation projects.

Market trajectory and the practical implications for operators

The market’s 6.5% CAGR reflects predictable volume growth plus structural changes in product mix and procurement behavior. Key implications for decision‑makers in 2026 are:

- Time‑to‑market is as strategic as cost: securing early design wins on new substations materially influences 3–5 year revenue streams.

- Quality and traceability are non‑negotiable: utilities now require verifiable linkage to national accuracy standards and audited test protocols.

- Materials and insulation choices (oil‑paper, gas‑insulated variants, epoxy systems) create differentiated cost and compliance profiles that must be evaluated across the BOM rather than at single component level.

Report toolkit: what PW Consulting delivers and how it solves 2026 pain points

The published report contains modular, operational tools designed for immediate deployment by procurement, engineering and M&A teams. These include:

- Supply‑chain mapping with tiered supplier risk scoring — enabling teams to quantify supplier concentration, bottlenecks and lead‑time exposure without requiring proprietary data dumps in this summary.

- BOM decomposition logic and cost modelling templates — structured to reveal where small yield or materials shifts produce outsized cost impacts in HVIT manufacturing.

- Yield‑adjustment and factory ramp models — calibrated for real‑world commissioning schedules so CAPEX planners can model break‑even points under alternative demand curves.

- Technology roadmaps and feature tradeoff matrices — juxtaposing insulating media, sensor electrification (electronic instrument transformers), and GIS compatibility to prioritize R&D and capex decisions.

Each tool is presented with use cases: e.g., how a BOM re‑weighting reduces total cost of ownership in a substation rollout, or how yield models shorten qualification timelines for design wins. The intent is to enable pragmatic decisions on cost control, compliance pathways and production scaling in 2026 — not to substitute for client‑specific engineering work that requires access to confidential plant data.

Competitive landscape — dimensions that determine winners

The HVIT market in 2026 is shaped less by pure product commoditization and more by a set of competitive dimensions that PW Consulting tracks across incumbent and specialist suppliers. Our analysis examines these dimensions rather than publishing prescriptive 2026 strategies for individual firms.

- Scale and geographic footprint: Large diversified suppliers bring global manufacturing, systems integration capabilities and long‑tail service agreements that support multinational utilities and OEMs.

- Manufacturing and test infrastructure: Independent test fields and ISO‑certified production lines are decisive in winning utility tenders that require traceability to national accuracy standards.

- Material and design IP: Proprietary insulating materials, encapsulation techniques, and design practices for bushing and GIS variants create defensible performance differentials.

- Local production and supply security: New capacity investments and localized factories reduce procurement risk and can be decisive for projects constrained by trade or domestic content rules.

- Specialist niches and service depth: Firms with bushing or generator breaker specialties command premium positions in adjacent aftermarket and lifecycle services.

Representative vendors in the competitive set include well‑known global OEMs and regional specialists. PW Consulting’s analysis highlights how their moats are constructed — for example, through production footprint, test capability, materials expertise, long‑standing utility relationships, and localized capacity expansions. Recent industry developments, such as the announced construction of a high‑voltage manufacturing facility in Waynesboro, Georgia (Ritz Instrument Transformers, announced January 2025), demonstrate the market’s tilt toward capacity localization — a trend with direct implications for 2026 procurement strategies.

To review the full competitor profiles and the matrix linking supplier capabilities to utility tender criteria, access the complete report: Access the full report and complete distribution maps .

Market structure and concentration — what the numbers imply

The competitive environment shows a moderate concentration: the three‑firm concentration (CR3) sits at 35.0% while the five‑firm concentration (CR5) is 55.0%. This structure means scale and specialization both create routes to competitive advantage. Buyers retain leverage in many procurement scenarios, but long certification cycles and local content constraints give established suppliers attractive pockets of margin. New entrants seeking to disrupt pricing must therefore offset entry costs with targeted technology or local capacity that shortens buyer switching costs.

Regulatory, materials and ESG dynamics that matter in 2026

Regulatory and materials regimes continue to reconfigure supplier economics in 2026:

- Metering and accuracy standards drive procurement: compliance timelines and test traceability are routinely included as contractual milestones, increasing qualification overhead for new suppliers.

- Materials governance and insulation choices: traditional oil‑paper and SF6 gas approaches remain common, but regulators and customers pressure suppliers to demonstrate lifecycle emissions and alternatives, influencing product selection and cost structures.

- ESG and supply‑chain transparency: end buyers increasingly require validated carbon accounting and supplier audit trails, which alters total cost evaluations and favors suppliers who have integrated traceability into their manufacturing processes.

Methodology: why PW Consulting’s findings are robust and actionable

Our conclusions rest on layered triangulation that combines multiple independent sources to validate each datapoint. Primary inputs include structured interviews with utilities, OEM procurement teams and substation EPCs; site visits and factory audits; and BOM reverse‑engineering conducted in collaboration with independent test laboratories. We cross‑reference these with:

- Patent and technical literature citation analysis to identify emergent insulating materials and sensor architectures;

- Customs and trade flow analytics to estimate cross‑border equipment movements and capacity utilization;

- Supplier financials and capacity announcements to model supply elasticity and probable lead‑time impacts.

Where we rely on confidential company data or non‑public commissioning schedules, we validate via at least two independent sources and document the provenance in the full report. This approach allows us to present actionable, high‑confidence recommendations without disclosing sensitive client or supplier details in public summaries.

Strategic guidance for 2026 — three pragmatic actions

Based on our integrated analysis, executives should prioritize the following in 2026:

- Accelerate qualification pipelines: invest in pre‑qualification testing and traceability to shorten procurement windows and capture design wins on multi‑year substation programs.

- Re‑assess BOM and materials strategy: use BOM decomposition to identify where modest design changes yield durable cost and compliance advantages under tightening regulation.

- Hedge capacity risk through strategic partnerships or minority investments: secure access to localized manufacturing slots or flexible contract manufacturing to manage near‑term delivery risk without overcommitting fixed capital.

Next steps and where to find the full analysis

PW Consulting’s full Instrument Transformers Market report contains the complete regional and application distribution maps, supplier scorecards, scenario models and downloadable toolkits that enable immediate 2026 planning and capital allocation. For procurement teams, engineers and investors needing to convert the market’s 6.5% CAGR into concrete action plans, please consult the full dataset and model repository: Access the full report and complete distribution maps .

In an environment where certification timelines, materials compliance and capacity localization converge, 2026 is the year to convert market momentum into defensible business outcomes. PW Consulting’s briefing equips leaders with the analytical instruments — not just the raw numbers — to do so.

For detailed analysis of this topic, please visit the official page: Instrument Transformers Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.