PW Consulting Forecast: Global EV Market to Reach USD 1,139.5 Billion by 2032

PW Consulting: Strategic Preview — Electric Vehicles Market 2026 Intelligence Brief

PW Consulting releases a strategic preview of our upcoming Electric Vehicles (EVs) market research report, designed to inform executive decisions across corporate development, procurement, and manufacturing planning in 2026. This briefing demonstrates the depth of our analysis while preserving the proprietary, segment-level datasets that clients will access through the full report. Think of this piece as a trailer: rigorous, actionable, and calibrated to generate high-confidence decisions — but intentionally partial so that decision-makers must consult the complete dataset for transaction-grade execution.

Electric Vehicles (EVs) Market

Market Snapshot (High-Level)

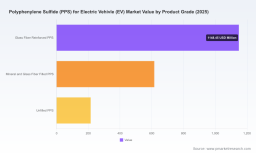

The global market for EV-related advanced polymers and components is now a scale industry. By our base year 2025 the market reaches USD 405.3 Billion, driven by accelerating electrification across passenger and commercial fleets. In 2026 the market expands to roughly USD 481.1 Billion, and our 2026–2032 forecast implies a compound annual growth rate (CAGR) of 15.9%, taking the addressable opportunity above USD 1,139.5 Billion by 2032. Historical momentum is strong: the market more than doubles from 2020 to 2025, underscoring both structural demand and rapid technology substitution.

- Primary macro tailwinds: regulatory-led weight reduction and emissions targets, accelerating OEM BEV programs, and substitution of metallic parts with high-performance polymers for thermal and electrical management.

- Supply-side constraints: energy intensity of polymerization and a narrow upstream feedstock base create episodic cost volatility that translates directly into component-level margin pressure.

- Market structure: the sector is moderately concentrated (CR3 ≈ 31.5%, CR5 ≈ 38.2%), leaving room for regional champions and specialized suppliers to capture disproportionate value via design wins and system integration.

What’s New in 2026 — Strategic Implications

Entering 2026, three dynamics redefine capital allocation and sourcing strategy:

- Regulatory acceleration: Stricter vehicular weight and emissions rules make material substitution not optional but mandatory for compliance-driven platforms.

- Feedstock and energy risk: Production of high-performance polymers remains energy-intensive and reliant on a compressed set of chemical intermediates; past episodes of upstream price spikes materially affect supplier cost-to-serve and delivery reliability.

- Product specification intensity: OEMs demand tailored material grades (thermal, flame retardance, laser-weldability, recycled content) — design wins increasingly hinge on demonstrable manufacturing compatibility, not just lab metrics.

Practical Deliverables — What the Full Report Gives You

Our full PW Consulting package equips leadership with operational tools that translate market intelligence into executable programs. Key assets include:

- Supply chain topology maps showing tiered supplier relationships, chokepoints, and geographic risk clusters—designed for rapid scenario planning and near-term sourcing migration.

- BOM decomposition frameworks that translate material substitution decisions into procurement KPIs, total-cost-of-ownership analytics, and part-level margin sensitivities.

- Yield-adjustment and manufacturability models that simulate the impact of grade changes, molding process switches, and recycling content on first-pass yield and warranty exposure.

- Technology roadmaps integrating material innovation, processing equipment evolution, and qualification timelines to align R&D, procurement, and program launch calendars.

- Compliance and ESG playbooks mapping regulatory regimes to production changes, enabling companies to prioritize CAPEX for low-risk, high-ROI retrofits.

Each tool is operationally oriented: they do not merely describe “what” is changing — they provide decision rules for “how” to reallocate capital, adjust sourcing, and structure supplier contracts in 2026. To preserve commercial confidentiality, parameterized datasets, the full BOM templates, and scenario outputs are available in the paid report and client workshops.

Competitive Landscape — Dimensions That Matter (Not Predictions)

Our competitive analysis focuses on the strategic vectors that determine who wins in EV polymer applications. Rather than publishing each firm’s playbook, we map competitive dimensions that buyers and investors should monitor when vetting partners or targets.

- Technology moat: Proprietary resin formulations and compounding know-how yield thermal, chemical, and mechanical performance advantages. Firms holding deep formulation IP are able to fast-track OEM qualifications and command premium design-in relevance.

- Manufacturing footprint and compounding scale: Localized compounding capability near major automotive hubs reduces logistics risk and shortens qualification cycles—critical for OEM Tier-1 design windows.

- Sustainability and circularity credentials: Grades incorporating mechanically recycled content or lower-carbon production processes are increasingly table stakes for large OEM platform awards and public-sector tenders.

- System-integration capability: Suppliers that combine polymer grades with engineering support for overmolding, busbar encapsulation, or laser welding secure more durable design wins because they reduce OEM integration risk.

- Supply security and raw-material access: Vertical relationships with feedstock suppliers or diversified sourcing reduce exposure to upstream shocks and enable differentiated commercial terms.

Representative players in this competitive set — spanning long-established chemical companies to regional polymer specialists — exhibit combinations of the above dimensions. Recent corporate moves (capacity expansions, targeted grade launches) confirm a market where execution of capacity and qualification programs matters as much as the base resin chemistry.

For a practical synthesis of competitor moves and the supplier scorecard we use to assess qualification probability, consult the full competitive matrix and supplier risk dashboards in our report: Access full competitive matrices and supplier dashboards here .

Industry Noise and Input-Risk Signals

Several technical and supply signals are noisy but predictive in 2026. Relevant facts we incorporate into scenario toolkits include the energy intensity of polymer production, restricted supplier bases for key intermediates, and regulatory-induced feedstock price volatility observed in recent years. These inputs feed our procurement stress tests and cost-of-goods simulations without relying on single-source assumptions.

- Production energy: Polymerization of certain high-performance resins remains energy-intensive; this is a direct driver of regional cost differentials and a lever for electrification and on-site renewables to lower variable costs.

- Feedstock concentration: Synthesis pathways for many high-performance polymers rely on a limited set of intermediates, creating supply tightness when regional environmental controls or feedstock price shocks occur.

- Regulatory pressure: Weight-reduction standards and emissions policies continue to push OEMs toward polymer replacement, accelerating demand for qualified high-temperature polymer grades.

Methodology — How PW Consulting Produces High-Confidence Intelligence

Our findings rest on a layered-triangulation methodology combining four pillars: primary intelligence, hard-data reconciliation, physical verification, and machine-enabled pattern discovery.

Primary intelligence includes structured interviews with OEMs and Tier-1 engineers, confidential procurement debriefs, and supplier management meetings. Hard-data reconciliation leverages customs and trade flows, capex filings, patent citation networks, and commercial transaction datasets to construct market balances. Physical verification comprises targeted BOM teardowns, laboratory qualification tests, and selective plant visits. Finally, machine-enabled methods — including natural-language processing of regulatory filings, satellite analysis of capex buildouts, and job-posting analytics — surface early signals of capacity shifts and skill migration.

We emphasize that several inputs derive from non-public sources cleared for research use under confidentiality agreements (e.g., aggregated supplier lead-time records, anonymized procurement tenders, and confidential OEM part specifications). These are triangulated against open-source signals and independent lab validation to produce the decision-grade outputs in our full report.

Actionable Strategic Guidance for 2026

Executives using our brief should prioritize three strategic moves this year to capture upside and shield downside risk.

- Hedge and localize: Reduce exposure to feedstock and energy constraints by prioritizing local compounding capacity investments or long-term offtake agreements with diversified suppliers.

- Design-for-supply: Make material selection decisions conditional on supplier risk scores and qualification timelines rather than on lab performance alone; build modular qualification paths into vehicle program timelines.

- Invest in manufacturing intelligence: Deploy AI-driven process control and yield-optimization tools to realize performance parity when switching to advanced polymer grades — these upgrades pay back faster in high-cost environments.

These are not theoretical suggestions: our scenario models quantify how each lever alters program margin and launch risk. The full report contains executable playbooks, supplier shortlists, and CAPEX prioritization matrices to convert strategy into procurement and engineering actions.

Next Steps — Where to Get the Full Intelligence

PW Consulting’s complete EV market research report packages the datasets, supplier scorecards, BOM templates, and scenario outputs required for investment committees and procurement teams to act immediately in 2026. For access to the full distribution maps, granular segmentation, and transaction-ready tools, please consult our report: Download the full PW Consulting EV Market Report .

Our 2026 workshops and bespoke advisory retainers are scheduled on a limited basis to ensure depth with select clients. Reach out to PW Consulting to reserve a briefing where we will walk your team through the full dataset and run prioritized scenarios tailored to your portfolio and program timelines.

For detailed analysis of this topic, please visit the official page: Electric Vehicles (EVs) Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.