From USD 11,000.0 Million in 2025 to USD 15,839.0 Million by 2032 — PW Consulting Forecasts 5.5% CAGR for Butterfly Valves Market

Butterfly Valves Market — Strategic Briefing for 2026

As PW Consulting’s senior industry analyst, I present a focused, action-oriented briefing designed to support executive decision-making in 2026. This release previews the strategic insights from our full Butterfly Valves Market study (base year 2025) and explains why calibrated capital allocation and supply‑chain restructuring are urgent for organizations active in fluid control today. We show the analytical structure and practical toolset of the report while deliberately withholding detailed segment-level distributions to encourage direct access to the full dataset and interactive maps.

Butterfly Valves Market

Executive snapshot

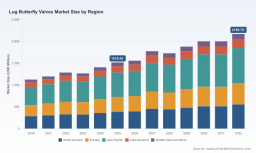

The global butterfly valves market is operating from an expanded base: the 2025 market size stands at USD 11,000.0 Million, and our forecast horizon (2026–2032) carries the industry forward at an annualized pace consistent with a 5.5% CAGR. Under this growth trajectory, the market is projected to reach approximately USD 15,839.0 Million by 2032, with 2026 acting as the first year of renewed investment cycles and regulatory recalibration.

Why 2026 is an inflection year

Several converging forces make 2026 a decisive moment for asset owners, OEMs and large distributors:

- Raw‑material volatility: late‑2025 to early‑2026 saw sharp moves in stainless steel and nickel pricing and broader metal input inflation, placing direct pressure on BOM costs and supplier margins.

- Regulatory and ESG uplift: tightening water‑quality and emissions compliance is reshaping procurement specifications and validation cycles across water/wastewater, power and industrial sectors.

- Automation and digitization push: buyers increasingly demand actuated, sensor‑ready valves that integrate with plant OT/IT stacks, creating new opportunity but also forcing legacy providers to retrofit product lines.

- Concentration dynamics: the market exhibits mid‑to‑high concentration with the top three suppliers accounting for roughly 55.0% of industry revenue and the top five near 60.0%, which sustains both pricing power and selective consolidation risk.

These dynamics drive the timing and scale of capital allocation decisions: whether to invest in local manufacturing, secure long‑lead critical materials via forward contracts, or accelerate product development for compliance-driven markets.

Practical tools inside the full report

PW Consulting’s study is structured as an operational playbook, not merely a desk survey. The deliverables are engineered for execution teams and include the following modules (examples):

- Supply‑chain topology and tiered supplier maps that link geographical nodes with critical subassembly risk scores.

- BOM decomposition logic with configurable levers for material substitution, finish specification and torque/actuation trade‑offs.

- Yield‑adjustment and scrap models that translate shopfloor process parameters into expected cost per unit under alternate scenarios.

- Technical roadmaps showing credible technology pathways from resilient seated designs to lined and high‑performance architectures, with maturation timelines and likely cost/benefit inflection points.

- Vendor scorecards and RFP templates designed to extract design‑win commitments and post‑sale service levels that are measurable in contracts.

Each tool is accompanied by implementation guidance: where to apply the lever, the typical stakeholder owners (procurement, engineering, operations), and the common pitfalls we have observed in field engagements. The report intentionally refrains from publishing fixed parameter values for proprietary models; instead, it supplies the analytic framework and calibrated inputs to run scenario analyses for your specific supply base.

Competitive landscape — dimensions that determine wins in 2026

Rather than predicting single‑firm outcomes, our report unpacks the structural dimensions that drive market success. These competitive vectors determine which players capture design wins and sustain aftermarket revenue:

- Certification and compliance moats — companies that secure sector‑specific approvals (e.g., potable‑water certifications) fast‑track procurement inclusion in municipal and OEM tenders.

- Material and metallurgy capabilities — control over alloy sourcing and casting/forging processes reduces vulnerability to raw‑material shocks and shortens time‑to‑scale for upgraded product lines.

- Actuation and systems integration — partners who offer plug‑and‑play actuators, smart positioners and digital diagnostics win specifications in modernized plants.

- Aftermarket and service networks — local presence for maintenance and spare parts is increasingly decisive for long‑term lifecycle revenues.

- Cost and delivery reliability — consistent lead times and predictable pricing during commodity cycles enable suppliers to be preferred partners for large projects.

Applying these dimensions to the competitive set yields clear implications:

- Companies with strong potable‑water certifications and established municipal relationships are advantaged in public sector tenders.

- Manufacturers with integrated actuation offerings or close OEM partnerships are better positioned to capture specification shifts toward digital valve assemblies.

- Regional low‑cost producers retain price leverage but must demonstrate compliance and aftermarket reach to unlock utility and power sector demand.

For practical, company‑level scoring by dimension — and how these scores translate into realistic design‑win probabilities for 2026 procurements — consult the detailed competitor matrices in the full report. Access the full dataset and distribution maps here: Download the full report .

Technology pathways and procurement levers

The technology section reframes product decisions as portfolio choices. We map three actionable pathways and the procurement levers that support each:

- Cost resilience pathway — prioritize material substitutions, standardized actuator interfaces and near‑term yield improvements on existing lines.

- Differentiation pathway — invest in high‑performance disc metallurgy, test‑certified sealing systems and extended warranties tied to remote diagnostics.

- Compliance and digitization pathway — couple certified materials with smart actuation and traceability systems to meet ESG and regulatory audits.

For each pathway the report supplies calibrated trade‑off matrices — indicating when incremental R&D or CapEx is likely to yield margin recovery versus when procurement contracts or hedging should be the preferred control.

Methodology — how PW Consulting builds actionable advantage

Our findings are the result of layered triangulation and primary validation executed during 2025–2026. Methodological pillars include:

- Patent and standards analysis to identify non‑obvious design protections and certification timelines.

- Hands‑on BOM reverse engineering and material assay work with sample components to benchmark supplier cost positions without disclosing proprietary line‑items.

- Customs and shipment flow analytics to map true supplier footprints and lead‑time variability across trade lanes.

- Targeted interviews with OEM procurement heads, plant engineering teams and distributor channel managers to validate adoption barriers for new valve types.

- Operational site visits and bench test data to calibrate yield and durability assumptions used in our cost models.

We emphasize the provenance of our inputs — many data points are synthesized from sources that are not publicly consolidated (customer contracts, factory yields, certified lab assays). The report documents the provenance and confidence intervals for every major assertion so that decision-makers can trace recommendations back to verifiable evidence.

Strategic priorities for capital allocation in 2026

Based on our integrated analysis, leadership teams should consider the following prioritized actions in 2026:

- Define a short list of supply‑chain continuity projects (dual‑sourcing or secured allotments for critical alloys) to insulate margins against metal price shocks.

- Mandate a 12–18 month program to convert the highest volume valve SKUs to modular actuator interfaces to accelerate digital retrofits.

- Deploy targeted CapEx to raise first‑pass yields in high‑variance casting operations rather than broad cost-cutting across all plants.

- Accelerate service and spare‑parts investments in priority regions where regulatory compliance is driving faster replacement cycles.

- Evaluate selective M&A to close capability gaps (automation, testing labs, regional service centers) rather than broad horizontal consolidation.

These priorities are calibrated to the current macro context — material inflation, ESG compliance costs and a market concentration profile that favors selective scale plays.

Next steps and how to obtain the full intelligence

PW Consulting’s full Butterfly Valves Market report contains the proprietary segmentation maps, interactive supplier dashboards and plug‑and‑play Excel models required to test all scenarios against your own portfolio. The public summary here is intentionally selective to preserve the strategic value of the underlying analytics while demonstrating the depth of our work.

To review the complete dataset, company scoring matrices and the operational toolkits described above, access the full report and interactive appendices: Download the full report .

For detailed analysis of this topic, please visit the official page: Butterfly Valves Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.