PW Consulting Forecast: CO2 Incubators Market to Reach USD 1,139.7 Million by 2032

CO2 Incubators Market — Strategic Briefing for 2026 Capital Allocation

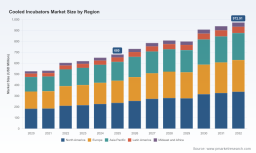

PW Consulting’s latest CO2 Incubators Market report (base year 2025) reframes how executives and procurement leaders should think about capital deployment in controlled-environment equipment for the life sciences. The market is now firmly in an expansion phase: global revenue grows from USD 617.1 Million in 2020 to USD 820.7 Million in 2025 and is projected to reach USD 1,139.7 Million by 2032, with a 2026–2032 compound annual growth rate (CAGR) of 4.9%. These headline numbers underscore a predictable, albeit selective, investment window in 2026 for product refresh, compliance-driven replacement, and targeted platform upgrades.

CO2 Incubators Market

Why this report matters to 2026 decision cycles

Capital committees, supply-chain chiefs, and R&D heads are asking three questions in 2026: where to prioritize limited CapEx, how to reduce lifecycle cost in the next procurement round, and how to reduce compliance risk in regulated workflows. This briefing explains the strategic value of our full report without disclosing the granular breakdowns that buyers and competitors prize — a deliberate “trailer” approach designed to demonstrate depth while protecting proprietary segmentation data.

-

Market momentum and durability: the market’s steady growth trajectory validates multi-year procurement programs rather than one-off tactical spend.

-

Consolidation and concentration: the market shows a moderate-to-high concentration profile (CR3: 62.0%; CR5: 78.0%), implying that procurement leverage and supplier selection will materially affect total cost of ownership (TCO) and validation timelines.

-

Regulatory and capex tailwinds: hospitals and regulated laboratories are increasing equipment spend to meet GLP/GMP and cleanroom standards, creating near-term replacement demand ahead of performance-driven upgrades.

Market snapshot (2026 context)

Our analysis treats 2025 as the operational baseline. Key macro takeaways for 2026 planning:

-

Growth runway: the market advances at a 4.9% CAGR in the forecast window, which supports staged procurement strategies rather than heavy front-loaded investment.

-

Demand drivers: compliance upgrades (GLP/GMP/FDA 21 CFR Part 11), institutional CapEx increases in aging healthcare estates, and the energy/ESG imperative for lower-power refrigeration technologies.

-

Technology mix: energy-efficient Peltier systems are gaining adoption as alternatives to compressor refrigeration in specific lab use cases, driven by lower lifecycle energy and refrigerant concerns.

Competitive dynamics — what separates winners from followers

Our competitive analysis synthesizes firm-level product architectures, service footprints, channel relationships, and certification practices. Rather than predicting each player’s 2026 moves, we map the competitive dimensions that determine design wins, margin resilience, and long-term defensibility.

-

Technology moat: suppliers with differentiated thermal control (e.g., advanced Peltier control, hybrid compressor/Peltier systems, UV/antimicrobial integrations) can command price premiums in regulated segments.

-

Compliance and validation support: suppliers that bundle validation documentation, site-qualification services, and software audit trails (aligned to ISO cleanroom classifications and FDA 21 CFR Part 11) are preferred in pharmaceutical and clinical buyers.

-

Service and distribution scale: after-sales service networks and spare-parts logistics determine uptime. For high-utilization environments, time-to-repair is as important as upfront price.

-

OEM partnerships and private-label channels: strategic OEM relationships expand access to hospital systems and national lab networks, creating repeatable revenue streams beyond one-off equipment sales.

Representative firms covered in the report include established manufacturers across Europe, North America, and Asia whose product portfolios span compressor and Peltier cooling, antimicrobial features, and varying automation levels. Our study evaluates their competitive positions against the dimensions above and identifies the non-price levers that most frequently drive procurement outcomes.

For immediate insight into supplier profiles and competitive positioning, access the full company benchmarking framework here: Access the full CO2 Incubators Market report .

Operational playbooks and toolkits included in the report

This study is explicitly operational. Clients receive practical, implementable toolkits — not only strategic commentary — to support 2026 procurement and operational decisions. Key deliverables include:

-

Supply-chain topology and partner map: a layered supplier map that highlights critical single-source components, second-tier subassemblies, and geo-concentration risk to inform dual-sourcing and inventory policy.

-

BOM decomposition logic: a repeatable methodology for decomposing vendor quotes into labor, commodity, and proprietary modules — enabling apples-to-apples TCO comparisons without relying solely on list price.

-

Yield-adjustment and replacement-rate models: calibrated to typical laboratory utilization and mean-time-to-failure (MTTF) observations, these models quantify replacement cycles and spare-part budgets over a 5–7 year horizon.

-

Technology roadmaps and retrofit decision matrices: comparative scenarios for Peltier vs compressor vs hybrid implementations tied to lifecycle energy consumption, refrigerant compliance risk, and site-level footprint constraints.

-

Regulatory alignment templates: checklists and documentation bundles that accelerate validation for GLP/GMP and ISO-aligned cleanroom deployments.

Each toolkit is purpose-built to address practical 2026 pain points — accelerating procurement cycles, reducing hidden lifetime costs, and ensuring compliance during installations. The report demonstrates how to apply these tools without disclosing the proprietary numeric outputs that clients use to make supplier selections.

Industry signals shaping 2026 procurement urgency

Several converging signals make 2026 a decisive year for capital allocation:

-

Regulatory tightening: buyers in regulated segments increasingly require validated audit trails and antimicrobial design elements; equipment that does not meet these expectations faces longer qualification windows and higher total on-boarding cost.

-

Hospital CapEx dynamics: median capex ratios and aging estates are prompting accelerated replacement cycles in clinical diagnostics environments — buying now can avoid costly mid-cycle remediation.

-

Technology substitution: Peltier-cooled units are materially reducing operational energy use in select workflows, creating an ESG and OPEX case for replacement versus repair in many facilities.

Methodology: how PW Consulting builds confidence in hidden numbers

Our findings are produced through a disciplined, multi-layered approach we term Layered Triangulation. Core elements:

-

Patent and standards citation analysis to identify where technical innovation is concentrated and to infer feature roadmaps of leading vendors.

-

Proprietary supply-chain mapping and BOM decomposition combining vendor documentation, audited procurement line-items, and customs/shipment feeds to estimate component-level cost drivers.

-

Expert interviews across four stakeholder groups — OEM engineering, hospital procurement, lab directors, and third-party service providers — used to validate assumptions and adjust deployment curves.

-

On-site audits and laboratory performance tests to benchmark energy use and control precision between representative Peltier and compressor architectures.

By cross-validating these independent evidence streams, we can reliably model demand and TCO without exposing the granular segmentation charts in this briefing. The full report documents the triangulation mechanics and the sources used to produce each model.

Strategic implications and recommended board-level actions for 2026

Executives should treat the CO2 incubator market as a controlled, high-impact lever for risk reduction and operating-cost improvement. Recommended actions for 2026 include:

-

Prioritize purchases that deliver measurable validation support and software audit capabilities for regulated units to reduce qualification time and compliance risk.

-

Implement a two-tier procurement strategy: urgent replacements for aged, non-compliant assets; multi-year staged upgrades focused on energy-efficient platforms where a clear ROI exists.

-

Negotiate service-level agreements that include remote-diagnostics and performance guarantees to mitigate downtime risk and shift a portion of lifecycle risk back to suppliers.

-

Build a short-list of strategic OEM/channel partners based on service footprint and documentation completeness rather than headline price alone.

For teams preparing RFPs or CapEx proposals, our downloadable templates and comparative frameworks significantly shorten vendor evaluation time and improve outcome predictability. Learn more and obtain the full datasets and segmentation maps here: Access the full CO2 Incubators Market report .

Closing perspective

2026 is a year to convert foresight into structured action. The CO2 incubators market shows moderate, sustained growth and significant pockets of strategic differentiation rooted in thermal technology, compliance support, and service capability. PW Consulting’s report equips leaders with the operational tools and competitive context required to convert market momentum into durable value while preserving the detailed segmentation and supplier benchmarks that power superior procurement outcomes.

For detailed analysis of this topic, please visit the official page: CO2 Incubators Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.