PW Consulting: Semiconductor Inspection Equipment Market Poised to Hit USD 8,400.0 Million by 2032

Semiconductor Inspection Equipment Market — Strategic Imperatives for 2026

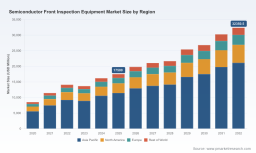

The semiconductor front-end inspection equipment market is at a strategic inflection point in 2026. PW Consulting’s latest study uses a 2025 base year and multi-year historical trend analysis (2020–2025) to show that the market reached USD 5,600.0 Million in 2025 and is growing at a compound annual growth rate (CAGR) of 7.5% through the 2026–2032 forecast horizon, reaching roughly USD 8,400.0 Million by 2032. This trajectory is driven by a confluence of node complexity, advanced packaging transitions, and regulatory-driven supply-chain realignment — factors that make near-term capital allocation and vendor strategy decisions materially consequential for OEMs, IDMs, and fabs.

Semiconductor Inspection Equipment Market

Market outlook: growth drivers and structural shifts

-

Technology push: Continued scaling to ≤5nm logic, 3D NAND growth, and GAA transistor adoption increase demand for higher-sensitivity front-side inspection and multi-surface capability. Inspection systems must evolve from single-point detection to system-level defect classification that informs upstream process control.

Semiconductor Inspection Equipment Market -

AI-enabled workflows: The industry is rapidly embedding AI/ML for defect classification and predictive maintenance. Vendors that can combine high signal-to-noise detection with low-latency data pipelines and model explainability gain disproportionate design-win advantages.

-

Packaging complexity: Panel-level and glass interposer inspection (including double-sided/internal defect detection) create new inspection modalities and product niches, expanding the addressable market beyond classical wafer-only inspection.

-

Supply-chain constraints: Specialty optics, lasers, and sensors are experiencing extended lead times, which lengthens procurement cycles and raises the premium on supply-chain transparency and alternative sourcing strategies.

-

Geopolitics and regulation: Export controls and licensing regimes — including controls on certain front-end tools — are reshaping where and how OEMs invest and where fabs secure equipment, accelerating localization and partnership strategies.

Why 2026 is a strategic decision year

Capital cycles that begin in 2026 will set production capacity and process architectures for the next three to five years. The combined effect of accelerated node complexity, regulatory friction (export licensing), and supply-chain lead-time risk means procurement timelines are longer and vendor selection costs are higher. Firms that delay strategic decisions risk either missing performance step-changes or incurring retrofit costs to meet compliance and yield targets.

What PW Consulting’s report delivers — pragmatic, operational tools

Our report is designed to be execution-focused: it does not stop at trend analysis but delivers actionable instruments that procurement, process integration, and corporate strategy teams can operationalize immediately.

-

Supply-chain topology and risk heatmaps — visualizing supplier-critical nodes, single-source dependencies, and lead-time sensitivity so procurement can prioritize mitigation and dual-sourcing initiatives.

-

BOM teardown logic and cost drivers — a repeatable framework for breaking down inspection-system BOMs (optics, lasers, sensors, motion systems, software stacks) to identify modular substitution opportunities and target components for total-cost-of-ownership reduction.

-

Yield-adjustment and ROI models — scenario-driven models that translate inspection sensitivity and throughput improvements into yield uplift, cycle-time reduction, and EBITDA impact under multiple CAPEX timelines.

-

Technology roadmaps and migration playbooks — comparative matrices that align inspection modalities to node and packaging roadmaps, helping R&D and fab teams prioritize investments between optical, e‑beam, and hybrid approaches.

-

Compliance and localization frameworks — playbooks to align procurement and deployment strategies with export controls, licensing risk, and on-shore service requirements, without prescribing specific legal remedies.

Each tool is accompanied by templates, decision-checklists, and an executive dashboard so teams can translate strategic intent into procurement specs and pilot programs in 2026.

Competitive landscape — dimensions that determine wins (not deterministic forecasts)

The market shows measurable concentration (CR3 ~55.0%, CR5 ~65.0%), indicating that a small set of vendors holds a meaningful share of high-end inspection spend while a broader cohort competes on throughput, price, and niche capabilities. Rather than publish granular commercial forecasts for each vendor, PW Consulting analyzes the competitive dimensions that shape outcomes in 2026:

-

Technology moat: Firms with proprietary optics, detector sensitivity, and algorithmic IP (for example, vendors with long histories in patterned-wafer sensitivity) defend high-end logic and memory design wins.

-

Installed base and service network: Scale in field service and spare-part logistics shortens time-to-yield for fabs — a decisive factor when uptime and rapid root-cause analysis matter.

-

Throughput vs. sensitivity trade-offs: Certain customers prioritize throughput for mature nodes and mass production, while others accept lower throughput for ultra-high sensitivity needed in advanced nodes — vendors are positioned differently across this axis.

-

System integration and metrology coupling: Companies that integrate inspection into a broader process-control stack (metrology + deposition/etch feedback) capture more value through closed-loop yield improvements.

-

Supply-chain and compliance alignment: Local manufacturing partnerships and alternative sourcing of critical optics/lasers provide competitive advantage in regions affected by export licensing nuances.

Representative vendors we profile in-depth include global leaders and regional specialists. Our competitive analysis dissects their moats, service footprints, product architecture choices, and the operational criteria customers use for design wins — without releasing confidential firm-level projections. For full company matrices and comparative scorecards, see the detailed company profiles in the report.

Recent market moves and tactical implications

Examples of product innovation and market entry are already reshaping procurement decision criteria. New inspection modalities targeting panel-level and double-sided substrate defects, and additions such as DIC (differential interference contrast) inspection on non-patterned wafers, are changing where inspection value is captured. At the same time, export-control regimes and raw-material constraints are prompting buyers to prioritize vendors that demonstrate transparent, resilient supply chains.

Operational recommendations for 2026

-

Re-base your vendor strategy to include supply-chain resilience metrics (lead-time exposure, single-sourced optics/lasers) in procurement scorecards.

-

Prioritize pilots that combine AI defect classifiers with physical metrology feedback to accelerate root-cause closure and reduce false-positive rates.

-

Allocate incremental CAPEX to inspection upgrades only when accompanied by measurable yield models that demonstrate payback within your cycle plan.

-

Negotiate service and spare-part SLAs that account for geopolitical risk and potential licensing delays, especially for equipment that may fall under restrictive ECCN classifications.

-

Invest in cross-functional “inspection + process” teams to ensure inspection output feeds actionable process control changes rather than only generating additional data.

Methodology and data rigor

PW Consulting’s analysis is built on a layered-triangulation methodology that combines patent-citation analysis, BOM reverse-engineering, proprietary supplier interviews under NDA, and on-site process audits with fab and OEM partners. We perform multi-source normalization across public filings, customer procurement data, independent lab measurements, and third-party shipment statistics to reconcile market sizing and validate growth assumptions.

Our firm also conducts targeted expert panels and cross-checks vendor claim sets against instrument-level tests and patent family timelines. This approach allows us to surface otherwise opaque dynamics — from component-level supply tension to the commercial levers that drive design wins — while protecting confidential commercial data and client anonymity.

Regulatory and geopolitical context — what to watch in 2026

Export-control regimes and collaborative restrictions among major supplier nations are continuing to influence equipment flows and localization strategies. Firms must align procurement and legal teams to anticipate licensing windows and assess whether on-shore contracting or qualified local partnerships are necessary to sustain roadmaps. The report includes a regulatory impact playbook to guide risk-weighted vendor selection.

For teams ready to convert these insights into a 2026 action plan, PW Consulting provides an extended deliverable set that includes granular regional and application breakdowns, supplier-level exposure matrices, and detailed company strategic scorecards. To access the full intelligence set, including the complete segmentation and interactive dashboards, please visit: https://pmarketresearch.com/worldwide-semiconductor-front-inspection-equipment-market-research .

PW Consulting’s Semiconductor Inspection Equipment Market report is structured to serve C-suite decision-makers, procurement officers, R&D leads, and process-integration teams — equipping them with the tools to prioritize investments, mitigate supplier risk, and capture the yield improvements that matter most in 2026.

For detailed analysis of this topic, please visit the official page: Semiconductor Inspection Equipment Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.