PW Consulting Report: PDCPD Market Poised to Grow at 6.3% CAGR Through 2032

PDCPD Market 2026: Strategic Preview for Capital Allocation and Operational Readiness

Polydicyclopentadiene (PDCPD) is shifting from a niche engineering polymer to a strategic industrial material in 2026. PW Consulting’s new market study reframes PDCPD not as a commodity but as a portfolio of engineering advantages, supply-chain sensitivities, and regulatory inflection points that will determine winners over the 2026–2032 planning horizon. This preview outlines why leading firms are treating PDCPD exposure as a board-level allocation decision and how our report equips executives to act decisively—without disclosing the granular tables reserved for subscribers.

Polydicyclopentadiene (PDCPD) Market

Executive snapshot: market trajectory and what it means for 2026 decisions

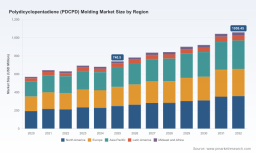

Now in 2026 the worldwide PDCPD molding market sits on a clear upward trajectory. Our base-year calibration (2025) places market value at USD 1.6 Billion, with the study projecting growth at a compound annual growth rate (CAGR) of 6.3% across the 2026–2032 forecast window. By the terminal year (2032) the market trajectory reaches approximately USD 2.5 Billion. These macro dynamics are driven by converging demand in durable transport components, industrial machinery, and select infrastructure use-cases where PDCPD’s impact resistance, low lifecycle maintenance and molding economics produce differentiated TCO outcomes.

Why 2026 is a decision point

Several converging forces make 2026 a pivotal year for capital allocation in PDCPD-related strategies:

- Supply-chain rebalancing following cracker margin volatility and monotonic changes in C5 feedstock availability, increasing the value of secured offtake and strategic backward-integration.

- Regulatory tightening on chemical registration and supply-chain communication, especially under REACH-equivalent regimes, raising the bar for compliance and supplier auditing.

- Manufacturing upgrades where AI-driven process control and improved RIM (reaction injection molding) automation materially improve yield and throughput, compressing payback timelines for capacity upgrades.

What senior executives must consider

For boards and C-suite teams, the implications are practical and immediate:

- Portfolio choices: PDCPD exposure should be reviewed against durability requirements, aftermarket economics and potential design-win pathways with OEMs.

- Risk mitigation: Securing feedstock channels and implementing regulatory-grade supply-chain documentation is now a precondition for commercial scale rather than a discretionary compliance activity.

- Operational leverage: Investments in yield models and digital process control tend to unlock margins faster than vertical integration in most scenarios—our scenario suite quantifies where that holds true.

Tools in the PW Consulting report and their 2026 utility

The full market study delivers not only market estimates but practical, executable tools that address 2026 pain points in procurement, product development, and compliance. Key inclusions are:

- Comprehensive supply‑chain map that traces DCPD origin to end-use molding nodes, highlighting single-point dependencies and logistics vectors relevant to 2026 contingency planning.

- BOM deconstruction logic that enables companies to model PDCPD substitution economics by product family (without publishing our confidential case matrices in this preview).

- Yield adjustment and NPI (new product introduction) ramp models that convert laboratory yield curves into plant-level throughput forecasts under realistic downtime and scrap assumptions.

- A technology roadmap that sequences polymerization, catalyst optimization, and RIM automation opportunities from tactical (12–24 months) to strategic (3–7 years).

Each tool is implemented as an interactive worksheet or model in the report so commercial teams can stress-test supplier quotes, capital plans and compliance investments against multiple scenarios applicable to 2026.

How these tools solve 2026 problems (practical framing)

Executives face three tangible 2026 problems: rising input volatility, compliance stringency, and the need to rapidly demonstrate product suitability to OEMs. Our tools are mapped to these problems as follows:

- Cost control: The BOM and yield models let CFOs simulate the marginal effect of feedstock price swings on product margin and optimize sourcing mixes and hedging thresholds.

- Compliance and audit readiness: The supply‑chain map and regulatory impact overlays create audit-ready documentation flows tied to REACH-style registrations and downstream communication obligations.

- Design Wins and market access: The technology roadmap and design-win checklist expose the non-price determinants—material certification, cycle-time guarantees, and supplier reliability metrics—required to win and sustain OEM partnerships.

Competitive landscape: what differentiates incumbents and challengers

The PDCPD market displays a concentrated supplier structure in 2026, with the top three suppliers representing roughly 65.0% of reported market share and the five largest about 80.0%. This concentration creates a playing field in which a small set of competitive dimensions determine access and pricing power.

- Protected production know-how and registered resin systems: Firms with proprietary resin formulations and validated RIM systems hold durable technical moats because these capabilities directly affect cycle time, part performance and secondary processing needs.

- Channel and service networks: Distributors and supporters that combine chemical supply with downstream engineering support (tooling, molding parameterization) convert raw material sales into stickier revenue streams.

- Design-win velocity: Winning OEM specifications is less about cheapest resin and more about predictable, auditable performance—first-pass yield, long-term thermal-mechanical behavior, and supply assurance are decisive.

Representative players exhibiting these dimensions include established resin producers and regional specialists. For example:

- Occidental Chemical Corporation—resin systems engineered for RIM and high-impact parts, exhibiting a classic product-technology moat tied to formulation and customer engineering support.

- Mitsui Chemicals—leveraging polymerization routes and global OEM relationships to offer validated material suites for automotive and construction segments.

- Riverhawk Company—positioned as a service-led provider offering rapid prototyping and customized molding, which is critical for industrial and machinery design cycles.

- Bodo Möller Chemie—acting as a regional integrator and technical distributor, addressing manufacturers who require localized supply and application support.

PW Consulting’s full analysis dissects these competitive dimensions and maps supplier capabilities to likely OEM selection criteria in 2026. For a detailed comparative matrix and our assessed likelihoods of near-term design wins, read the full study: Access the full PDCPD market report .

Supply‑side dynamics: feedstock, pricing and regulatory overlays

Raw-material dynamics remain the most immediate operational constraint in 2026. Dicyclopentadiene (DCPD), the primary monomer for PDCPD, is still tied to C5 streams from ethylene crackers. Global capacity and spot pricing volatility—evidenced by historical episodes of cracker margin swings—translate into procurement risk for PDCPD processors.

- Feedstock concentration: Where cracker outages or planned turnarounds occur, downstream PDCPD converters find lead times elongated; securing long-term offtake or diversifying feedstock sources is now a standard mitigation tactic.

- Regulatory compliance: DCPD’s registration bands under REACH and equivalent regimes require precise supply-chain communication and hazard management, pushing buyers to choose suppliers who can demonstrate compliant documentation flows.

These dynamics amplify the value of the report’s supply-map and procurement playbooks for 2026 contracting cycles.

Methodology: why our estimates are decision-grade

PW Consulting’s 2026 study deploys a layered triangulation methodology that combines three pillars: proprietary primary research (supplier and OEM interviews), patent and technical literature mining, and transactional-level reconstruction via BOM logic and plant-output inference models. We performed targeted patent citation tracing to locate material innovation vectors and paired those signals with confidential supplier interviews and anonymized commercial contracts where allowed under NDA.

In practice this means our market-size and scenario outputs are not simple extrapolations. They are reconstructed from observed purchase behaviors, validated plant throughput assumptions and closed-loop checks against public filings, customs datapoints and proprietary pricing feeds. This approach is why our models capture both the visible market and the latent demand that only emerges under certain price or regulatory pathways.

Operational recommendations for 2026 (actionable priorities)

Based on our 2026 assessment, executives should prioritize three operational moves to preserve optionality:

- Lock in conditional offtake: Short-term offtakes with staggered volume commitments reduce exposure while preserving upside participation if markets tighten.

- Invest selectively in yield-improvement projects: Prioritize automation and process analytics projects with sub-24-month payback, which our models consistently show outperform capacity build-outs in terms of ROI during this cycle.

- Centralize compliance documentation: Create an audit-ready dossier mapped to REACH-style reporting and OEM procurement checklists to remove administrative friction in design-wins.

Next steps

For commercial teams, procurement leaders and R&D heads evaluating PDCPD exposure in 2026, PW Consulting’s full report offers the granular scenario tables, supplier scorecards and executable models needed to convert insight into action. Our public preview is intentionally selective; the full study contains the segmented distribution maps, interactive BOM models and supplier-specific matrices that underpin strategic decisions.

To access the complete PDCPD market research package and licensing options, visit: Access the full PDCPD market report .

For detailed analysis of this topic, please visit the official page: Polydicyclopentadiene (PDCPD) Market

Lacy Lee

Senior Marketing Manager

sales@pmarketresearch.com

00852-95632430

PW Consulting: www.pmarketresearch.com

Tags

PW Consulting

The Best-reviewed Subdivided Market Risk Analysis Firm in the US and East Asia.